गतिशील अनुकूली बहु-समय अवधि प्रवृत्ति अनुसरण और दोलन उत्क्रमण संयुक्त रणनीति

अवलोकन

यह रणनीति एक मिश्रित ट्रेडिंग सिस्टम है जो ट्रेंड फॉलोअरिंग और रेंज ट्रेडिंग को जोड़ती है। यह इचिमोकू क्लाउड का उपयोग करके बाजार की स्थिति की पहचान करती है, MACD मोमेंटम पुष्टि और RSI ओवरबॉट/ओवरसोल्ड संकेतकों के साथ, साथ ही ATR का उपयोग करके गतिशील स्टॉप-लॉस प्रबंधन करती है। यह रणनीति ट्रेंडिंग बाजारों में ट्रेंड के अवसरों को पकड़ने और साइडवे बाजारों में रिवर्सल के अवसर खोजने में सक्षम है, जिससे यह अत्यधिक अनुकूलनीय और लचीली बनती है।

रणनीति सिद्धांत

रणनीति बहु-स्तरीय संकेत पुष्टि तंत्र का उपयोग करती है:

- बाजार की स्थिति का मुख्य निर्धारण इचिमोकू क्लाउड के माध्यम से किया जाता है, कीमत और क्लाउड के बीच स्थिति के आधार पर यह पता चलता है कि बाजार ट्रेंड में है या साइडवे।

- ट्रेंडिंग बाजारों में, जब कीमत क्लाउड के ऊपर होती है और RSI>55, MACD हिस्टोग्राम सकारात्मक होता है, तो लॉन्ग पोजीशन ली जाती है। जब कीमत क्लाउड के नीचे होती है और RSI<45, MACD हिस्टोग्राम नकारात्मक होता है, तो शॉर्ट पोजीशन ली जाती है।

- साइडवे बाजारों में, जब RSI<30 और स्टोकास्टिक RSI<20 होता है, तो लॉन्ग के अवसर तलाशे जाते हैं। जब RSI>70 और स्टोकास्टिक RSI>80 होता है, तो शॉर्ट के अवसर तलाशे जाते हैं।

- जोखिम प्रबंधन के लिए ATR पर आधारित गतिशील स्टॉप-लॉस का उपयोग किया जाता है, स्टॉप-लॉस की दूरी ATR मान का 2 गुना होती है।

रणनीति के लाभ

- उच्च बाजार अनुकूलनशीलता: विभिन्न बाजार स्थितियों के अनुसार स्वचालित रूप से ट्रेडिंग रणनीति को समायोजित करने में सक्षम, जिससे रणनीति की स्थिरता बढ़ती है।

- उच्च संकेत विश्वसनीयता: एकाधिक संकेतक सत्यापन तंत्र का उपयोग करके झूठे संकेतों के प्रभाव को कम करता है।

- उत्कृष्ट जोखिम नियंत्रण: ATR गतिशील स्टॉप-लॉस के माध्यम से लाभ को बढ़ने देता है और साथ ही जोखिम को प्रभावी ढंग से नियंत्रित करता है।

- अच्छा विज़ुअलाइज़ेशन: बैकग्राउंड रंग के माध्यम से बाजार की स्थिति को चिह्नित करता है, जिससे व्यापारी बाजार के माहौल को आसानी से समझ सकते हैं।

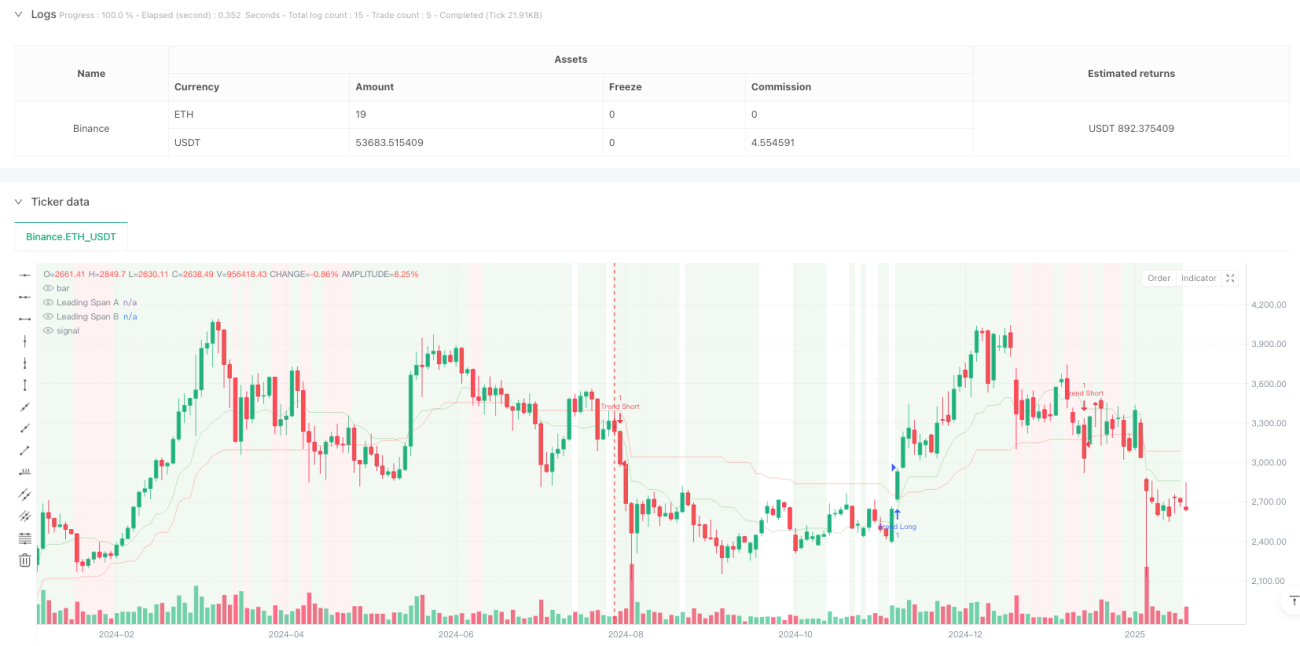

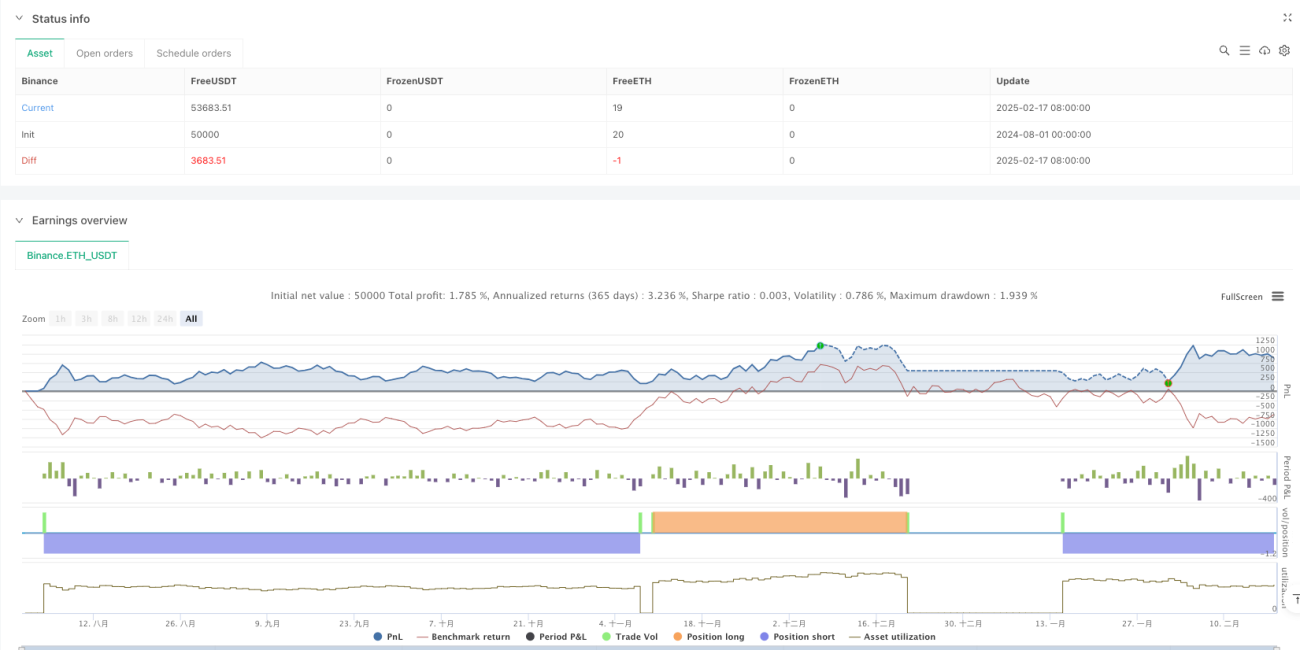

- उच्च समय-सीमा पर उत्कृष्ट प्रदर्शन: दैनिक समय-सीमा पर लाभ कारक 2.159 है, शुद्ध लाभ 10.71% है।

रणनीति जोखिम

- कम जीत दर: सभी समय-सीमाओं पर जीत दर 40% से कम है, जिसके लिए मजबूत मानसिक सहनशक्ति की आवश्यकता है।

- कम समय-सीमा पर अत्यधिक ट्रेडिंग: 4-घंटे की समय-सीमा पर 430 ट्रेड निष्पादित किए गए, जो दक्षता को कम करता है।

- संकेत में देरी: कई संकेतक सत्यापन के कारण, कुछ बाजार अवसर छूट सकते हैं।

- पैरामीटर ऑप्टिमाइज़ेशन में कठिनाई: कई संकेतकों का संयोजन रणनीति ऑप्टिमाइज़ेशन की जटिलता को बढ़ाता है।

रणनीति अनुकूलन दिशाएँ

- संकेत फ़िल्टरिंग अनुकूलन: जीत दर बढ़ाने के लिए प्रत्येक संकेतक की सीमाओं को समायोजित किया जा सकता है।

- समय-सीमा अनुकूलन: मुख्य रूप से दैनिक या उससे ऊपर की समय-सीमाओं पर उपयोग करने की सिफारिश की जाती है, और विभिन्न बाजार विशेषताओं के अनुसार पैरामीटर समायोजित किए जा सकते हैं।

- स्टॉप-लॉस अनुकूलन: विभिन्न बाजार स्थितियों के अनुसार ATR गुणक को गतिशील रूप से समायोजित करने पर विचार किया जा सकता है।

- प्रवेश समय अनुकूलन: प्रवेश सटीकता बढ़ाने के लिए वॉल्यूम पुष्टि या मूल्य पैटर्न पुष्टि जोड़ी जा सकती है।

- पोजीशन प्रबंधन अनुकूलन: संकेत शक्ति के आधार पर गतिशील पोजीशन प्रबंधन प्रणाली डिज़ाइन की जा सकती है।

सारांश

यह रणनीति एक अच्छी तरह से डिज़ाइन किया गया, तार्किक रूप से स्पष्ट, व्यापक ट्रेडिंग सिस्टम है। कई संकेतकों के सहयोग से, यह बाजार की स्थिति की बुद्धिमानी से पहचान करती है और ट्रेडिंग अवसरों को सटीक रूप से पकड़ती है। हालांकि कम समय-सीमाओं पर कुछ समस्याएं हैं, दैनिक जैसी उच्च समय-सीमाओं पर इसका प्रदर्शन उत्कृष्ट है। व्यापारियों को लाइव ट्रेडिंग में मुख्य रूप से दैनिक स्तर के संकेतों पर ध्यान केंद्रित करने और अपनी जोखिम सहनशीलता के अनुसार पैरामीटर को उचित रूप से समायोजित करने की सलाह दी जाती है। निरंतर अनुकूलन और समायोजन के माध्यम से, यह रणनीति व्यापारियों को स्थिर लाभ के अवसर प्रदान करने की उम्मीद है।

- 1