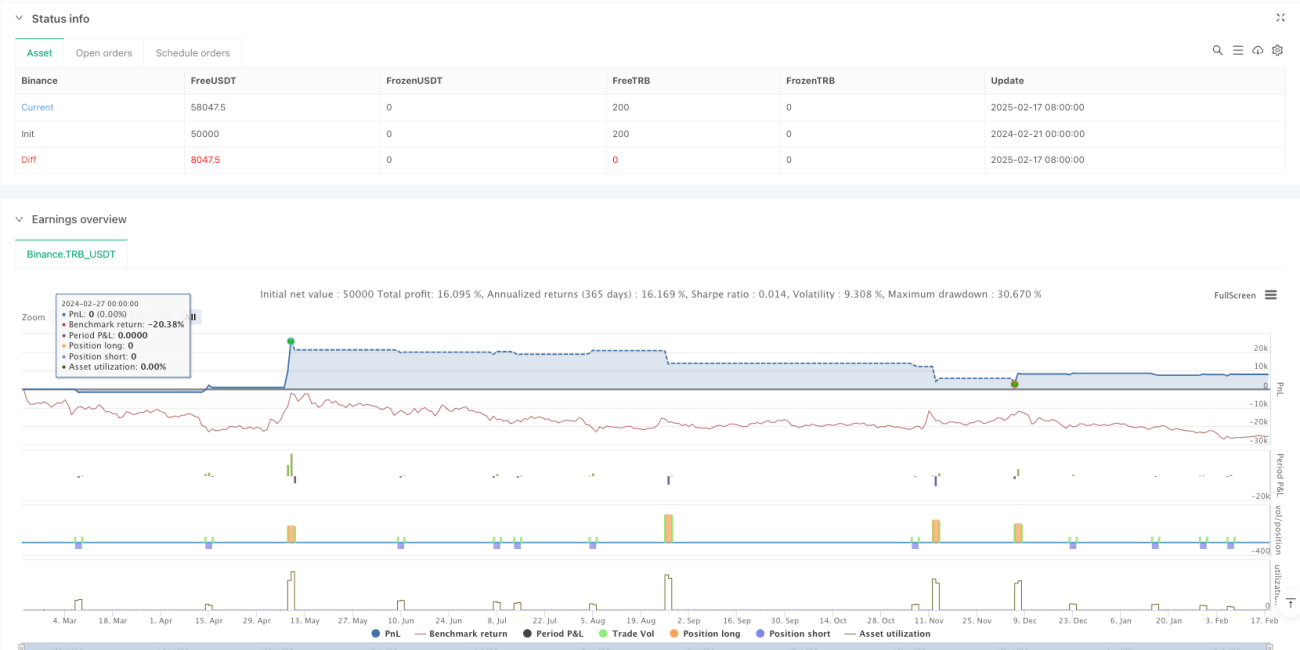

अवलोकन

यह रणनीति एक मूल्य ब्रेकआउट और गतिशील ट्रेलिंग स्टॉप-लॉस पर आधारित ट्रेडिंग सिस्टम है। यह पिछले N अवधियों के उच्चतम और न्यूनतम मूल्यों की निगरानी करता है, और जब मूल्य इन महत्वपूर्ण स्तरों को तोड़ता है तो ट्रेड करता है। यह रणनीति एक बुद्धिमान स्टॉप-लॉस तंत्र का उपयोग करती है, जो केवल 1% लाभ प्राप्त करने के बाद सक्रिय होता है, जिससे लाभ को पूरी तरह से विकसित होने दिया जा सके। साथ ही, 1 घंटे की कूल-डाउन अवधि निर्धारित करके ओवर-ट्रेडिंग से बचा जाता है, जिससे प्रत्येक ट्रेड की गुणवत्ता में सुधार होता है।

रणनीति का सिद्धांत

रणनीति के मूल तर्क में निम्नलिखित प्रमुख भाग शामिल हैं:

- प्रवेश संकेत: पिछले N अवधियों के उच्चतम और न्यूनतम मूल्यों की गणना करके, जब वर्तमान मूल्य इन स्तरों को तोड़ता है तो ट्रेडिंग सिग्नल ट्रिगर होता है। लॉन्ग एंट्री के लिए मूल्य को पिछले उच्च स्तर को एक निश्चित प्रतिशत तोड़ना आवश्यक है, जबकि शॉर्ट एंट्री के लिए पिछले निम्न स्तर को तोड़ना आवश्यक है।

- ट्रेड प्रबंधन: अत्यधिक अस्थिरता के दौरान बार-बार ट्रेडिंग से बचने के लिए 1 घंटे की ट्रेडिंग कूल-डाउन अवधि लागू की जाती है।

- जोखिम नियंत्रण: एक गतिशील ट्रेलिंग स्टॉप-लॉस का उपयोग किया जाता है, जो केवल 1% लाभ प्राप्त करने के बाद सक्रिय होता है, जिससे लाभ की बेहतर सुरक्षा होती है।

- पैरामीटर अनुकूलन: मुख्य पैरामीटर जैसे कि लुकबैक अवधि, ब्रेकआउट थ्रेशोल्ड, स्टॉप-लॉस प्रतिशत आदि को विभिन्न बाजार स्थितियों के अनुसार समायोजित किया जा सकता है।

रणनीति के लाभ

- गतिशील जोखिम प्रबंधन: ट्रेलिंग स्टॉप-लॉस तंत्र के माध्यम से, रणनीति लाभ की रक्षा करते हुए लाभ को बढ़ने दे सकती है।

- लचीला अनुकूलन: यह रणनीति पैरामीटर समायोजित करके विभिन्न बाजार स्थितियों के अनुकूल हो सकती है, जिससे प्रदर्शन का अनुकूलन होता है।

- फ़िल्टरिंग तंत्र: ओवर-ट्रेडिंग से बचने और ट्रेड की गुणवत्ता में सुधार करने के लिए ट्रेडिंग कूल-डाउन अवधि का उपयोग किया जाता है।

- सरल और प्रभावी: रणनीति का तर्क स्पष्ट, समझने और लागू करने में आसान है, साथ ही इसमें अच्छी स्केलेबिलिटी बनी रहती है।

रणनीति के जोखिम

- फाल्स ब्रेकआउट जोखिम: बाजार में फाल्स ब्रेकआउट हो सकता है, जिससे गलत सिग्नल उत्पन्न हो सकते हैं। वॉल्यूम की पुष्टि जोड़ने की सलाह दी जाती है।

- स्लिपेज का प्रभाव: उच्च अस्थिरता की अवधि के दौरान, बड़े स्लिपेज का सामना करना पड़ सकता है, जो रणनीति के प्रदर्शन को प्रभावित कर सकता है।

- पैरामीटर संवेदनशीलता: रणनीति का प्रदर्शन पैरामीटर सेटिंग्स के प्रति संवेदनशील है, और इसके लिए सावधानीपूर्वक अनुकूलन की आवश्यकता है।

- बाजार पर्यावरण पर निर्भरता: कम अस्थिरता वाले वातावरण में प्रदर्शन खराब हो सकता है।

रणनीति सुधार के क्षेत्र

- वॉल्यूम संकेतक शामिल करना: वॉल्यूम पुष्टि के माध्यम से ब्रेकआउट सिग्नल की विश्वसनीयता में सुधार किया जा सकता है।

- ट्रेंड फ़िल्टर जोड़ना: दीर्घकालिक ट्रेंड संकेतकों के साथ मिलाकर, केवल ट्रेंड की दिशा में ट्रेड किया जा सकता है।

- गतिशील पैरामीटर समायोजन: बाजार की अस्थिरता के अनुसार स्वचालित रूप से ब्रेकआउट थ्रेशोल्ड और स्टॉप-लॉस पैरामीटर को समायोजित किया जा सकता है।

- एकाधिक समय-सीमा: सटीकता बढ़ाने के लिए कई समय-सीमाओं के संकेतों को एकीकृत किया जा सकता है।

निष्कर्ष

यह एक अच्छी तरह से डिज़ाइन की गई ट्रेंड फ़ॉलोइंग रणनीति है, जो मूल्य ब्रेकआउट और गतिशील स्टॉप-लॉस को जोड़ती है, जिससे बड़े ट्रेंड को कैप्चर किया जा सकता है और जोखिम को प्रभावी ढंग से नियंत्रित किया जा सकता है। रणनीति में उच्च अनुकूलन क्षमता है, और पैरामीटर अनुकूलन के माध्यम से इसे विभिन्न बाजार स्थितियों के अनुकूल बनाया जा सकता है। सुझाव है कि लाइव ट्रेडिंग में छोटे लॉट साइज़ से शुरुआत करें और धीरे-धीरे विभिन्न बाजार स्थितियों में रणनीति के प्रदर्शन का परीक्षण करें।

- 1