Nadaraya-Watson पर आधारित बहुआयामी एकीकृत ट्रेडिंग रणनीति

अवलोकन

यह रणनीति नादराया-वाटसन कर्नल रिग्रेशन पर आधारित एक बहु-आयामी ट्रेडिंग प्रणाली है, जो तकनीकी, भावना, अति-संवेदनशीलता और इच्छा इन चार आयामों की बाजार जानकारी को एकीकृत करके ट्रेडिंग निर्णयों के लिए समग्र संकेत तैयार करती है। रणनीति भार अनुकूलन विधि का उपयोग करती है, जिसमें विभिन्न आयामों के संकेतों को भारित किया जाता है, और संकेत गुणवत्ता में सुधार के लिए प्रवृत्ति और गति फिल्टर को जोड़ा जाता है। सिस्टम में एक पूर्ण जोखिम प्रबंधन मॉड्यूल भी शामिल है, जो स्टॉप-लॉस और टेक-प्रॉफिट के माध्यम से पूंजी की सुरक्षा करता है।

रणनीति सिद्धांत

रणनीति का मूल नादराया-वाटसन कर्नल रिग्रेशन विधि के माध्यम से बाजार डेटा के कई आयामों को स्मूथ करना है। विशेष रूप से:

- तकनीकी आयाम में क्लोज़िंग प्राइस का उपयोग किया जाता है।

- भावना आयाम में RSI संकेतक का उपयोग किया जाता है।

- अति-संवेदनशीलता आयाम में ATR अस्थिरता का उपयोग किया जाता है।

- इच्छा आयाम में मूल्य और मूविंग एवरेज के बीच विचलन का उपयोग किया जाता है।

इन आयामों को कर्नल रिग्रेशन द्वारा स्मूथ करने के बाद, पूर्वनिर्धारित भार (तकनीकी 0.4, भावना 0.2, अति-संवेदनशीलता 0.2, इच्छा 0.2) के माध्यम से भारित एकीकरण किया जाता है, जिससे अंतिम ट्रेडिंग संकेत बनता है। जब एकीकृत संकेत अपनी मूविंग एवरेज लाइन को पार करता है, तो प्रवृत्ति और गति फिल्टर के साथ पुष्टि होने पर ट्रेडिंग आदेश जारी किए जाते हैं।

रणनीति के लाभ

- बहु-आयामी विश्लेषण अधिक व्यापक बाजार दृष्टिकोण प्रदान करता है, एकल संकेतक की सीमाओं से बचाता है।

- नादराया-वाटसन कर्नल रिग्रेशन बाजार के शोर को प्रभावी ढंग से कम करता है और अधिक स्मूथ संकेत प्रदान करता है।

- भार अनुकूलन तंत्र बाजार विशेषताओं के अनुसार प्रत्येक आयाम के महत्व को समायोजित करने की अनुमति देता है।

- प्रवृत्ति और गति फिल्टर का जुड़ना संकेत गुणवत्ता में काफी सुधार करता है।

- पूर्ण जोखिम प्रबंधन प्रणाली पूंजी सुरक्षा सुनिश्चित करती है।

रणनीति जोखिम

- पैरामीटर ऑप्टिमाइज़ेशन की अति से ओवरफिटिंग हो सकती है।

- बहु-फिल्टर शर्तों के कारण कुछ प्रभावी संकेत छूट सकते हैं।

- कर्नल रिग्रेशन की गणना जटिलता अधिक है, जो रीयल-टाइम प्रदर्शन को प्रभावित कर सकती है।

- भार का अनुचित आवंटन कुछ महत्वपूर्ण बाजार संकेतों को कमजोर कर सकता है।

शमन उपायों में शामिल हैं: आउट-ऑफ-सैंपल परीक्षण के माध्यम से पैरामीटर सत्यापन, फिल्टर शर्तों का गतिशील समायोजन, गणना दक्षता का अनुकूलन, और भार आवंटन का नियमित मूल्यांकन और समायोजन।

रणनीति अनुकूलन दिशाएँ

- अनुकूली भार प्रणाली शुरू करना, जो बाजार की स्थिति के अनुसार प्रत्येक आयाम के भार को गतिशील रूप से समायोजित करे।

- अधिक बुद्धिमान फिल्टर तंत्र विकसित करना, जो संकेत गुणवत्ता और मात्रा को संतुलित करे।

- नादराया-वाटसन एल्गोरिदम के कार्यान्वयन को अनुकूलित करना, गणना दक्षता में सुधार करना।

- बाजार चक्र पहचान मॉड्यूल जोड़ना, विभिन्न बाजार चरणों में अलग-अलग पैरामीटर सेटिंग्स का उपयोग करना।

- जोखिम प्रबंधन प्रणाली का विस्तार करना, गतिशील स्टॉप-लॉस और पोजीशन प्रबंधन कार्य जोड़ना।

सारांश

यह एक नवीन रणनीति है जो गणितीय विधियों को ट्रेडिंग ज्ञान के साथ जोड़ती है। बहु-आयामी विश्लेषण और उन्नत गणितीय उपकरणों के माध्यम से, यह रणनीति बाजार के कई स्तरों को पकड़ सकती है और अपेक्षाकृत विश्वसनीय ट्रेडिंग संकेत प्रदान कर सकती है। हालांकि कुछ अनुकूलन स्थान हैं, लेकिन रणनीति का समग्र ढांचा मजबूत है और व्यावहारिक अनुप्रयोग मूल्य रखता है।

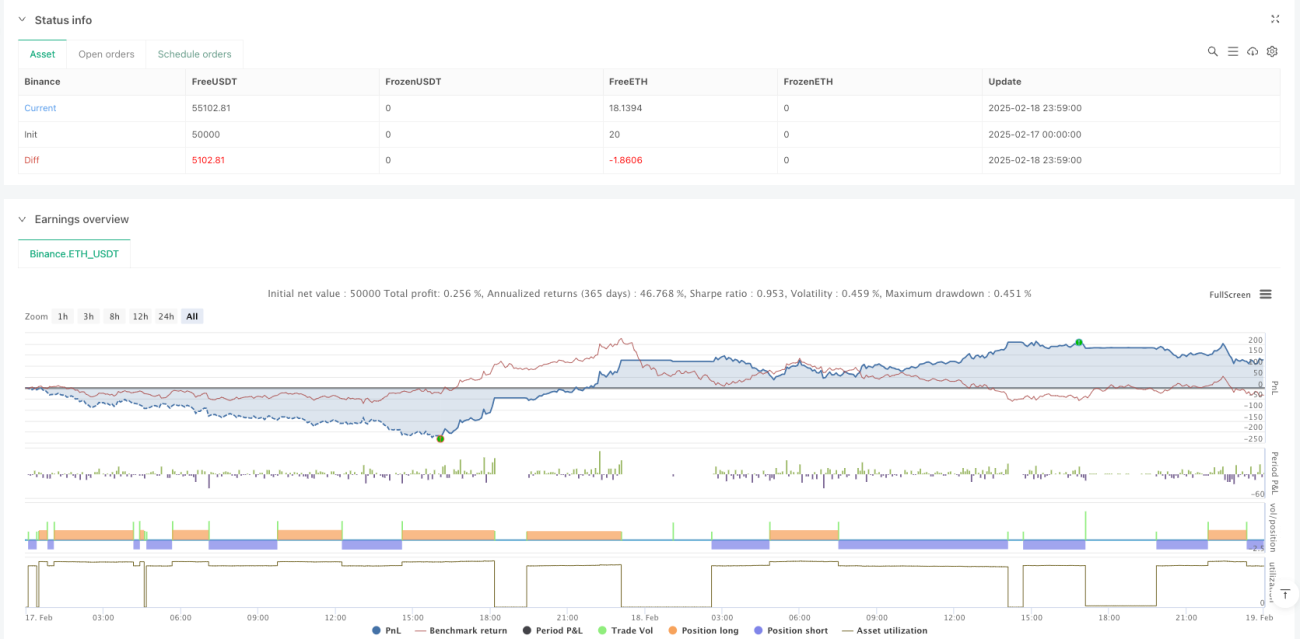

/*backtest

start: 2025-02-17 00:00:00

end: 2025-02-19 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("Enhanced Multidimensional Integration Strategy with Nadaraya", overlay=true, initial_capital=10000, currency=currency.USD, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

//────────────────────────────────────────────────────────────────────────────- 1