बुद्धिमान बहुआयामी अनुकूली प्रवृत्ति व्यापार प्रणाली

अवलोकन

यह रणनीति एक बहु-तकनीकी संकेतकों से युक्त बुद्धिमान ट्रेडिंग सिस्टम है, जो फेयर वैल्यू गैप (FVG), ट्रेंड सिग्नल और मूल्य कार्रवाई के समग्र विश्लेषण के माध्यम से बाजार के अवसरों की पहचान करता है। सिस्टम दोहरी रणनीति तंत्र का उपयोग करता है, जो ट्रेंड फॉलोइंग और स्विंग ट्रेडिंग की विशेषताओं को जोड़ता है, और गतिशील पोजीशन प्रबंधन और बहुआयामी निकास तंत्र के माध्यम से ट्रेडिंग प्रदर्शन को अनुकूलित करता है। यह रणनीति विशेष रूप से जोखिम नियंत्रण पर ध्यान केंद्रित करती है, और अस्थिरता फिल्टर और ट्रेडिंग वॉल्यूम पुष्टिकरण के माध्यम से सिग्नल की गुणवत्ता में सुधार करती है।

रणनीति सिद्धांत

रणनीति का मुख्य तर्क निम्नलिखित आयामों पर आधारित है:

- FVG गैप पहचान - मूल्य अंतराल के आकार की गणना करके संभावित ट्रेडिंग अवसरों की खोज

- ट्रेंड पुष्टिकरण प्रणाली - 200-दिवसीय मूविंग एवरेज, SuperTrend संकेतक और MACD का उपयोग करके बाजार की प्रवृत्ति की पुष्टि

- स्मार्ट मनी पुष्टिकरण - RSI ओवरबॉट/ओवरसोल्ड, वॉल्यूम असामान्यता और मूल्य कार्रवाई पैटर्न को ट्रेडिंग ट्रिगर के रूप में उपयोग करना

- गतिशील पोजीशन प्रबंधन - ATR आधारित अस्थिरता का उपयोग करके पोजीशन के आकार को समायोजित करना, जोखिम एक्सपोजर की स्थिरता सुनिश्चित करना

- बहुस्तरीय निकास तंत्र - ट्रेलिंग स्टॉप लॉस और लक्ष्य लाभ के संयोजन के माध्यम से ट्रेड से बाहर निकलने का प्रबंधन

रणनीति के लाभ

- उच्च अनुकूलनशीलता - रणनीति बाजार की अस्थिरता के अनुसार स्वचालित रूप से पैरामीटर और पोजीशन को समायोजित कर सकती है

- पूर्ण जोखिम नियंत्रण - कई फिल्टर और सख्त पोजीशन प्रबंधन के माध्यम से जोखिम को नियंत्रित करना

- विश्वसनीय सिग्नल गुणवत्ता - बहुआयामी संकेतक पुष्टिकरण के माध्यम से ट्रेडिंग सिग्नल की सटीकता में सुधार

- लचीला ट्रेडिंग तरीका - एक साथ ट्रेंड और रेंज बाजारों के अवसरों को पकड़ने में सक्षम

- वैज्ञानिक धन प्रबंधन - प्रतिशत जोखिम प्रबंधन का उपयोग, धन के उपयोग की तर्कसंगतता सुनिश्चित करना

रणनीति के जोखिम

- पैरामीटर संवेदनशीलता - कई पैरामीटर सेटिंग्स रणनीति के प्रदर्शन को प्रभावित कर सकती हैं, निरंतर अनुकूलन की आवश्यकता

- बाजार पर्यावरण पर निर्भरता - कुछ बाजार स्थितियों में झूठे ब्रेकआउट संकेत हो सकते हैं

- स्लिपेज प्रभाव - कम तरलता वाले बाजारों में बड़े स्लिपेज का सामना करना पड़ सकता है

- गणना जटिलता - कई संकेतकों की गणना से सिग्नल में देरी हो सकती है

- उच्च पूंजी आवश्यकता - रणनीति को पूर्ण रूप से लागू करने के लिए बड़ी प्रारंभिक पूंजी की आवश्यकता

रणनीति अनुकूलन दिशाएँ

- संकेतक भार अनुकूलन - मशीन लर्निंग विधियों का उपयोग करके प्रत्येक संकेतक के भार को गतिशील रूप से समायोजित किया जा सकता है

- बाजार अनुकूलन क्षमता में वृद्धि - बाजार अस्थिरता अनुकूलन तंत्र जोड़ना

- सिग्नल फिल्टर में सुधार - अधिक बाजार सूक्ष्म संरचना संकेतक शामिल करना

- निष्पादन तंत्र अनुकूलन - बुद्धिमान ऑर्डर विभाजन तंत्र जोड़कर प्रभाव लागत कम करना

- जोखिम नियंत्रण उन्नयन - गतिशील जोखिम बजट प्रबंधन प्रणाली जोड़ना

सारांश

यह रणनीति कई तकनीकी संकेतकों और ट्रेडिंग तकनीकों के एकीकृत उपयोग के माध्यम से एक पूर्ण ट्रेडिंग सिस्टम का निर्माण करती है। इसका लाभ बाजार परिवर्तनों के अनुकूल होने और साथ ही सख्त जोखिम नियंत्रण बनाए रखने की क्षमता में है। हालांकि अनुकूलन के लिए कुछ गुंजाइश है, कुल मिलाकर यह एक उचित डिज़ाइन किया गया मात्रात्मक ट्रेडिंग रणनीति है।

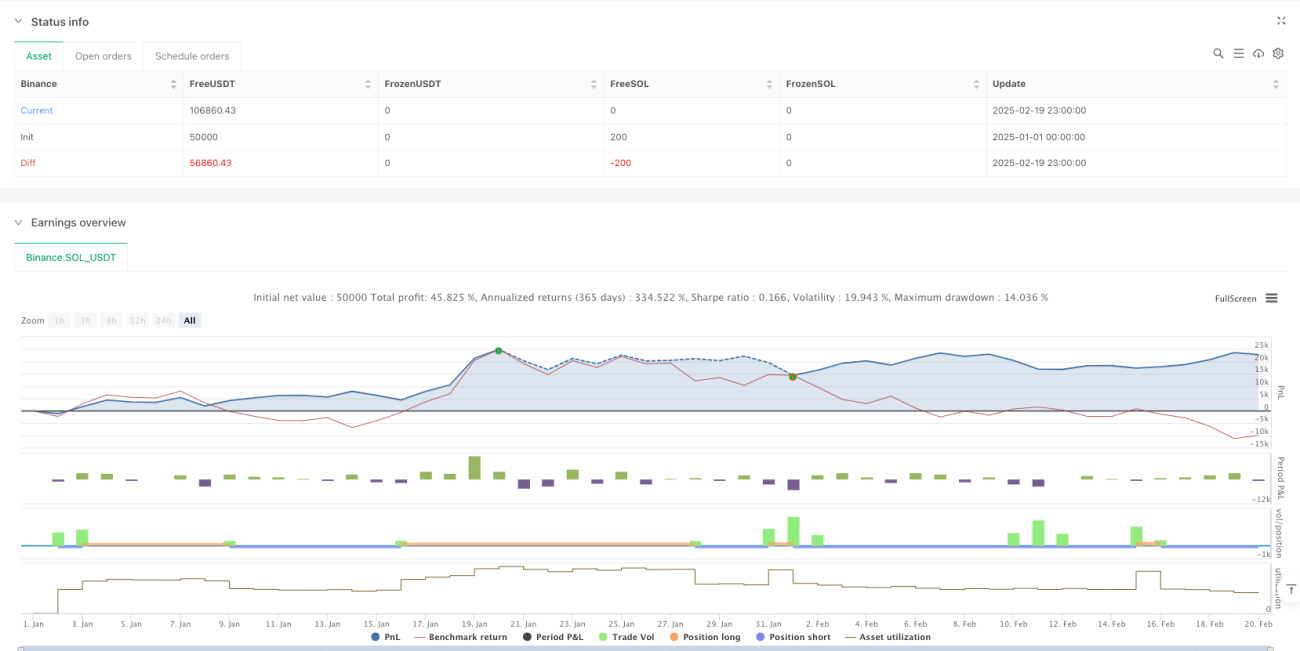

/*backtest

start: 2025-01-01 00:00:00

end: 2025-02-20 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=6

strategy("Adaptive Trend Signals", overlay=true, margin_long=100, margin_short=100, pyramiding=1, initial_capital=50000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.075)

// 1. Enhanced Inputs with Debugging Options- 1