अवलोकन

यह एक अभिनव ट्रेडिंग रणनीति है जो तरलता क्षेत्र विश्लेषण और आंतरिक बाजार संरचना गतिशीलता को जोड़ती है, जिसका उद्देश्य उच्च संभावना वाले प्रवेश बिंदुओं की पहचान करना है। यह रणनीति मूल्य और प्रमुख बाजार स्तरों के बीच की बातचीत को ट्रैक करती है और आंतरिक बाजार परिवर्तन का उपयोग करके ट्रेडों को ट्रिगर करती है, जिससे व्यापारियों को एक लचीली और सटीक बाजार प्रवेश विधि प्रदान होती है।

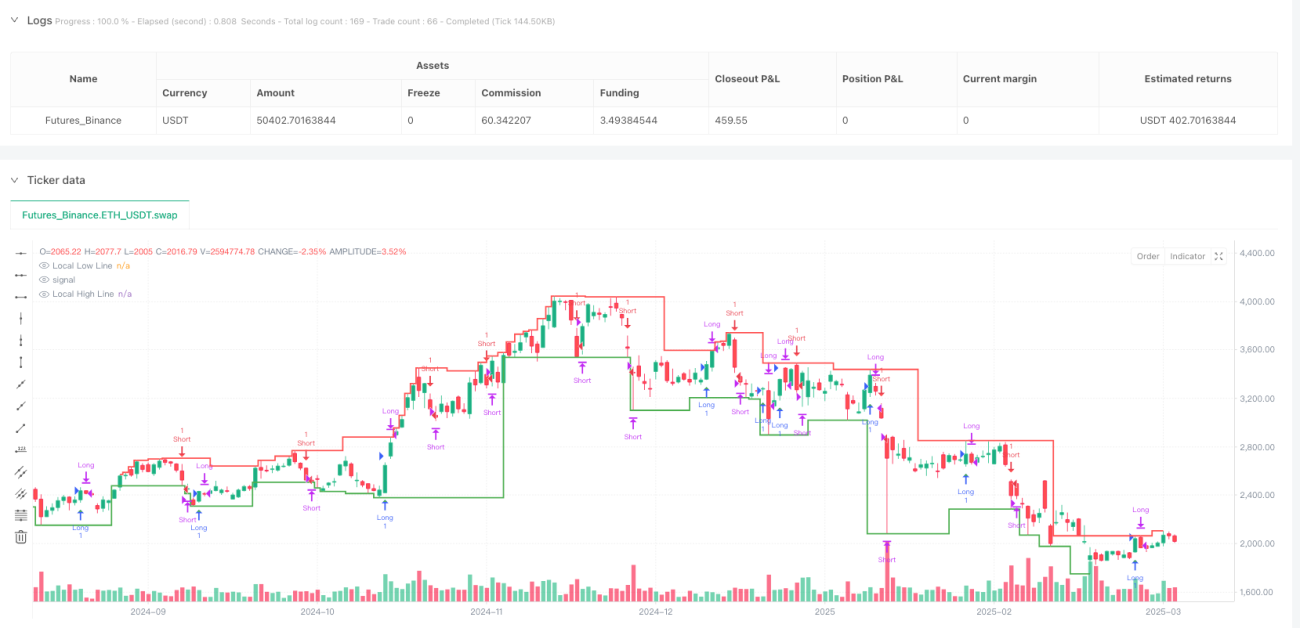

रणनीति सिद्धांत

रणनीति का मुख्य तर्क दो प्रमुख घटकों पर आधारित है: तरलता क्षेत्रों की पहचान और आंतरिक बाजार परिवर्तन। तरलता क्षेत्र स्थानीय उच्च और निम्न बिंदुओं के विश्लेषण के माध्यम से गतिशील रूप से निर्धारित किए जाते हैं, जबकि आंतरिक बाजार परिवर्तन पिछले तेजी या मंदी के स्तरों के माध्यम से मूल्य के टूटने पर आधारित होता है जो बाजार की दिशा में बदलाव का निर्धारण करता है।

रणनीति में निम्नलिखित मुख्य विशेषताएं हैं:

- आंतरिक बाजार परिवर्तन तर्क: पारंपरिक कैंडलस्टिक पैटर्न पर निर्भर नहीं करता, बल्कि प्रमुख स्तरों के मूल्य टूटने पर आधारित है

- तरलता क्षेत्र ट्रैकिंग: प्रमुख तरलता क्षेत्रों की गतिशील पहचान, कमजोर बाजार स्थितियों में ट्रेडिंग को रोकता है

- पैटर्न लचीलापन: तीन ट्रेडिंग मोड प्रदान करता है - "Both", "Bullish Only" और "Bearish Only"

- जोखिम प्रबंधन: अनुकूलन योग्य स्टॉप-लॉस और टेक-प्रॉफिट स्तर

- समय सीमा नियंत्रण: ट्रेडिंग समय अवधि का सटीक नियंत्रण

रणनीति के लाभ

- गतिशील अनुकूलनशीलता: रणनीति बाजार संरचना में परिवर्तनों पर तेजी से प्रतिक्रिया कर सकती है

- सटीक प्रवेश: तरलता क्षेत्रों और आंतरिक बाजार परिवर्तन को जोड़कर प्रवेश सटीकता में सुधार

- जोखिम नियंत्रणीय: अंतर्निहित स्टॉप-लॉस और टेक-प्रॉफिट तंत्र

- उच्च लचीलापन: विभिन्न बाजार स्थितियों के अनुसार ट्रेडिंग मोड चुनने की क्षमता

- बहुआयामी विश्लेषण: मूल्य क्रिया, तरलता और बाजार संरचना पर एक साथ विचार

रणनीति जोखिम

- बाजार में अत्यधिक उतार-चढ़ाव से स्टॉप-लॉस ट्रिगर हो सकता है

- साइडवेज बाजार में, बार-बार आने वाले सिग्नल ट्रेडिंग लागत बढ़ा सकते हैं

- पैरामीटर सेटिंग्स का अनुचित होना रणनीति के प्रदर्शन को प्रभावित कर सकता है

- बैकटेस्ट परिणाम वास्तविक व्यापार से भिन्न हो सकते हैं

रणनीति अनुकूलन दिशा

- पैरामीटर स्व-अनुकूलन के लिए मशीन लर्निंग एल्गोरिदम शामिल करना

- अधिक फिल्टर शर्तें जोड़ना, जैसे ट्रेडिंग वॉल्यूम, अस्थिरता संकेतक

- मल्टी-टाइमफ्रेम सत्यापन तंत्र विकसित करना

- स्टॉप-लॉस और टेक-प्रॉफिट एल्गोरिदम को अनुकूलित करना, बाजार अस्थिरता के अनुसार गतिशील समायोजन पर विचार

निष्कर्ष

यह एक अभिनव ट्रेडिंग रणनीति है जो तरलता विश्लेषण और बाजार संरचना गतिशीलता को एकीकृत करती है। लचीले आंतरिक बाजार परिवर्तन तर्क और सटीक तरलता क्षेत्र ट्रैकिंग के माध्यम से, यह व्यापारियों को एक शक्तिशाली ट्रेडिंग उपकरण प्रदान करती है। रणनीति की कुंजी इसकी अनुकूलनशीलता और बहुआयामी विश्लेषण क्षमता में निहित है, जो विभिन्न बाजार स्थितियों में उच्च निष्पादन दक्षता बनाए रख सकती है।

- 1