रणनीति अवलोकन

ओपनिंग रेंज ब्रेकआउट ATR ट्रेलिंग स्टॉप लॉस रणनीति एक मात्रात्मक ट्रेडिंग सिस्टम है जो ओपनिंग रेंज ब्रेकआउट और स्मार्ट मार्केट कॉन्सेप्ट्स को जोड़ती है। यह रणनीति अमेरिकी शेयर बाजार में खुलने के बाद पहले 5 मिनट (09:30-09:35 EST) में बनने वाली मूल्य सीमा (ओपनिंग रेंज) के ब्रेकआउट के अवसरों को पकड़ने पर केंद्रित है, और ट्रेडिंग सिग्नल की गुणवत्ता सुनिश्चित करने के लिए बहु-स्तरीय फिल्टर का उपयोग करती है। सिस्टम तत्काल या पुलबैक एंट्री का समर्थन करता है, जोखिम-लाभ अनुपात के आधार पर गतिशील समायोजन करता है, और लाभ प्रबंधन को अनुकूलित करने के लिए ATR (औसत ट्रू रेंज) ट्रेलिंग स्टॉप लॉस का विकल्प प्रदान करता है। इस रणनीति में "दूसरा मौका" ट्रेडिंग फीचर भी है, जो प्रारंभिक ट्रेड विफल होने पर विपरीत दिशा में ब्रेकआउट के अवसरों को पकड़ने में सक्षम बनाता है, साथ ही व्यापक विज़ुअलाइज़ेशन फीचर्स प्रदान करता है ताकि ट्रेडर बाजार की गतिशीलता को बेहतर समझ सकें।

रणनीति सिद्धांत

ओपनिंग रेंज ब्रेकआउट ATR ट्रेलिंग स्टॉप लॉस रणनीति का मूल तर्क बाजार खुलने के बाद प्रारंभिक मूल्य सीमा के महत्व पर आधारित है। यह रणनीति पहले एक निर्दिष्ट समय विंडो (09:30-09:35 EST) में कीमत के उच्चतम और निम्नतम बिंदुओं को रिकॉर्ड करती है, जिससे "ओपनिंग रेंज" बनती है। इसके बाद, सिस्टम उस सीमा से मूल्य के ब्रेकआउट की निगरानी करता है, और निम्नलिखित प्रमुख तंत्रों के साथ ट्रेड गुणवत्ता सुनिश्चित करता है:

-

ओपनिंग रेंज पहचान और ब्रेकआउट सत्यापन : सिस्टम निर्दिष्ट समय विंडो में मूल्य के उच्चतम और निम्नतम बिंदुओं को रिकॉर्ड करता है, फिर ब्रेकआउट की निगरानी करता है। ब्रेकआउट को दो-स्तरीय फिल्टर तंत्र के माध्यम से सत्यापित किया जाना चाहिए:

- कैंडलस्टिक शैडो प्रतिशत फिल्टर: यह सुनिश्चित करता है कि ब्रेकआउट कैंडल की ऊपरी/निचली छाया कैंडल बॉडी के निर्दिष्ट प्रतिशत से अधिक न हो, जिससे झूठे ब्रेकआउट से बचा जा सके।

- ब्रेकआउट दूरी फिल्टर: यह सुनिश्चित करता है कि मूल्य ब्रेकआउट का आकार उचित हो, न तो बहुत छोटा (मामूली ब्रेकआउट से बचने के लिए) और न ही बहुत बड़ा (अत्यधिक विस्तार से बचने के लिए)।

-

एंट्री तंत्र : रणनीति दो प्रकार की एंट्री का समर्थन करती है:

- तत्काल एंट्री: पुष्टि किए गए वैध ब्रेकआउट के उसी कैंडल के समापन मूल्य पर सीधे प्रवेश।

- पुलबैक एंट्री: कीमत के ब्रेकआउट कैंडल बॉडी के निर्दिष्ट प्रतिशत तक वापस आने की प्रतीक्षा करना, आमतौर पर 50% पुलबैक स्तर पर सेट किया जा सकता है।

-

स्टॉप लॉस सेटिंग : सिस्टम दो प्रकार के स्टॉप लॉस प्रदान करता है:

- ब्रेकआउट कैंडल स्टॉप: स्टॉप लॉस को ब्रेकआउट कैंडल के चरम बिंदु के बाहर सेट करना।

- विपरीत रेंज स्टॉप: स्टॉप लॉस को ओपनिंग रेंज की विपरीत सीमा के बाहर सेट करना, जिससे कीमत को अधिक उतार-चढ़ाव की जगह मिलती है।

-

जोखिम प्रबंधन : सिस्टम जोखिम-लाभ अनुपात गुणक (Risk:Reward Multiplier) का उपयोग करके स्वचालित रूप से टेक-प्रॉफिट स्तर की गणना करता है, जिससे गतिशील जोखिम प्रबंधन होता है। उदाहरण के लिए, 2:1 का जोखिम-लाभ अनुपात सेट करने का मतलब है कि संभावित लाभ संभावित हानि का दोगुना है।

-

ATR ट्रेलिंग स्टॉप : एक बार लाभ पूर्व निर्धारित जोखिम-लाभ अनुपात तक पहुँच जाता है, तो सिस्टम ATR-आधारित ट्रेलिंग स्टॉप को सक्रिय कर सकता है, जिससे कुछ लाभ लॉक हो जाता है जबकि ट्रेंड को जारी रहने दिया जाता है।

-

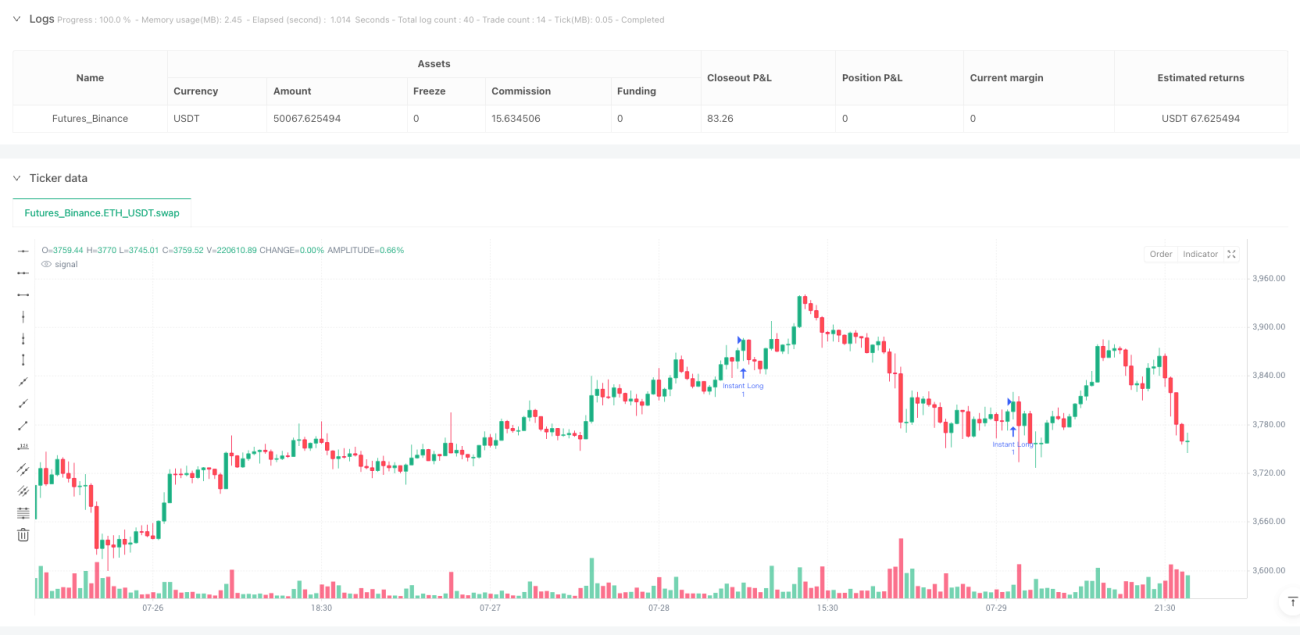

दूसरा मौका ट्रेड : जब प्रारंभिक ट्रेड स्टॉप लॉस ट्रिगर होता है या विफल होता है, तो सिस्टम स्वचालित रूप से ओपनिंग रेंज की विपरीत दिशा में ब्रेकआउट के अवसर की तलाश कर सकता है, जिससे उसी दिन द्विदिश ट्रेडिंग संभव होती है।

रणनीति के लाभ

-

गुणवत्तापूर्ण ट्रेडिंग अवसरों पर ध्यान केंद्रित करना : बहु-स्तरीय सत्यापन तंत्र (शैडो फिल्टर, दूरी फिल्टर) के माध्यम से, रणनीति झूठे ब्रेकआउट ट्रेडों को काफी कम करती है और जीत दर में सुधार करती है।

-

लचीला एंट्री तंत्र : विभिन्न ट्रेडिंग शैलियों और बाजार स्थितियों के अनुकूल तत्काल या पुलबैक एंट्री का समर्थन करता है। तत्काल एंट्री मजबूत ट्रेंड के लिए उपयुक्त है, जबकि पुलबैक एंट्री बेहतर एंट्री मूल्य प्राप्त कर सकती है।

-

अनुकूली जोखिम प्रबंधन : जोखिम-लाभ अनुपात गुणक पर आधारित गतिशील टेक-प्रॉफिट सेटिंग यह सुनिश्चित करती है कि प्रत्येक ट्रेड में एकसमान जोखिम विशेषताएँ हों, जिससे मानकीकृत धन प्रबंधन संभव होता है।

-

लाभ अधिकतमीकरण : ATR ट्रेलिंग स्टॉप फीचर प्राप्त लाभ की रक्षा करने के साथ-साथ मजबूत चाल को जारी रखने की अनुमति देता है, जिससे समय से पहले बाहर निकलने से बचा जा सकता है।

-

उच्च विज़ुअलाइज़ेशन : सिस्टम व्यापक दृश्य सहायता प्रदान करता है, जिसमें रेंज मार्कर, ब्रेकआउट सत्यापन लेबल, ट्रेड स्थिति संकेतक, एंट्री/स्टॉप/टारगेट मार्कर आदि शामिल हैं, जो ट्रेडिंग निर्णयों को अधिक सहज बनाते हैं।

-

पूर्वाग्रह-मुक्त पोस्ट-हॉक डिज़ाइन : रणनीति पूरी तरह से

barstate.isconfirmedका उपयोग करती है ताकि यह सुनिश्चित किया जा सके कि सभी निर्णय पुष्टि किए गए मूल्य डेटा पर आधारित हों, जिससे आगामी पूर्वाग्रह से बचा जा सके और वास्तविक ट्रेडिंग वातावरण के अनुरूप हो। -

दूसरा मौका तंत्र : दूसरा मौका ट्रेडिंग फीचर को सक्षम करके, रणनीति प्रारंभिक दिशा की गलती होने पर तेजी से बाजार परिवर्तनों के अनुकूल हो सकती है, विपरीत अवसरों को पकड़ सकती है और धन उपयोग दक्षता में सुधार कर सकती है।

-

सत्र प्रबंधन अनुकूलन : बिल्ट-इन सत्र समाप्ति पर ऑटो-क्लोज फीचर यह सुनिश्चित करता है कि रात भर पोजीशन न रखी जाए, जिससे रात्रि जोखिम कम होता है।

रणनीति जोखिम

-

रेंज निर्माण अवधि के दौरान उतार-चढ़ाव का जोखिम : ओपनिंग रेंज निर्माण अवधि (09:30-09:35) के दौरान, बाजार में असामान्य उतार-चढ़ाव हो सकता है, जिससे रेंज बहुत चौड़ी या बहुत संकरी हो सकती है। बहुत चौड़ी रेंज से स्टॉप लॉस बहुत बड़ा हो सकता है, जबकि बहुत संकरी रेंज से झूठे ब्रेकआउट बार-बार ट्रिगर हो सकते हैं।

समाधान : ओपनिंग रेंज आकार के लिए फिल्टर स्थिति जोड़ने पर विचार करें, असामान्य रेंज को हटाने के लिए; या ट्रेडिंग दिन फिल्टर को समायोजित करें, उच्च अस्थिरता वाले विशिष्ट दिनों (जैसे महत्वपूर्ण आर्थिक डेटा रिलीज़ दिन) से बचें। -

ब्रेकआउट के बाद तीव्र वापसी का जोखिम : वैध ब्रेकआउट के बाद बाजार में तीव्र वापसी हो सकती है, जिससे स्टॉप लॉस ट्रिगर होने के बाद बाजार फिर से मूल दिशा में चला जाता है।

समाधान : अधिक ढीली स्टॉप लॉस सेटिंग का उपयोग करने पर विचार करें, जैसे कि विपरीत रेंज स्टॉप; या एंट्री मैकेनिज्म को पुलबैक एंट्री में बदलें, ताकि बेहतर एंट्री मूल्य और कम जोखिम एक्सपोजर प्राप्त किया जा सके। -

सिग्नल गुणवत्ता फिल्टर सेटिंग्स पर निर्भर करती है : ब्रेकआउट सत्यापन के शैडो फिल्टर और दूरी फिल्टर पैरामीटर सेटिंग्स सिग्नल गुणवत्ता को महत्वपूर्ण रूप से प्रभावित करती हैं। अनुचित पैरामीटर अच्छे ट्रेड अवसरों को फिल्टर कर सकते हैं या बहुत अधिक निम्न-गुणवत्ता वाले सिग्नल स्वीकार कर सकते हैं।

समाधान : ऐतिहासिक बैकटेस्टिंग के माध्यम से फिल्टर पैरामीटर को अनुकूलित करें, विशिष्ट बाजार और इंस्ट्रूमेंट के लिए सबसे अच्छी सेटिंग खोजें; अनुकूली पैरामीटर का उपयोग करने पर विचार करें, बाजार की अस्थिरता के अनुसार फिल्टर मानकों को गतिशील रूप से समायोजित करें। -

ट्रेलिंग स्टॉप पैरामीटर संवेदनशीलता : ATR ट्रेलिंग स्टॉप की पैरामीटर सेटिंग बहुत टाइट होने पर छोटी वापसी में समय से पहले बाहर निकल सकती है, जबकि बहुत ढीली होने पर अत्यधिक लाभ वापसी हो सकती है।

समाधान : लक्ष्य इंस्ट्रूमेंट के ऐतिहासिक अस्थिरता गुणों के आधार पर ATR अवधि और गुणक को समायोजित करें; आंशिक रूप से पोजीशन बंद करने की रणनीति लागू करने पर विचार करें, कुछ पोजीशन फिक्स्ड टेक-प्रॉफिट पर और कुछ ट्रेलिंग स्टॉप पर। -

ट्रेड आवृत्ति सीमा : रणनीति प्रतिदिन अधिकतम दो ट्रेड (प्रारंभिक ट्रेड और दूसरा मौका ट्रेड) निष्पादित करती है, जो दिन के सभी अवसरों का पूरा उपयोग नहीं कर सकती।

समाधान : रणनीति का विस्तार करने पर विचार करें, दिन के अन्य महत्वपूर्ण मूल्य रेंज की निगरानी करें; या अन्य तकनीकी संकेतकों के साथ मिलकर एक मिश्रित रणनीति बनाएं, जिससे ट्रेड सिग्नल के स्रोत बढ़ें।

रणनीति अनुकूलन दिशाएँ

-

अनुकूली ओपनिंग रेंज अवधि : वर्तमान में रणनीति निश्चित 5-मिनट ओपनिंग रेंज का उपयोग करती है, बाजार की अस्थिरता के अनुसार रेंज की अवधि को गतिशील रूप से समायोजित करने पर विचार करें। कम अस्थिरता वाले बाजार में रेंज समय को 3 मिनट तक छोटा किया जा सकता है, जबकि उच्च अस्थिरता वाले बाजार में 10 मिनट तक बढ़ाया जा सकता है, जिससे विभिन्न बाजार स्थितियों के लिए बेहतर अनुकूलन होता है।

-

वॉल्यूम पुष्टि का उपयोग : ब्रेकआउट सत्यापन तंत्र में वॉल्यूम फिल्टर शर्त जोड़ें, जिसमें ब्रेकआउट के समय वॉल्यूम पिछले कई अवधियों के औसत वॉल्यूम से काफी अधिक हो, जिससे ब्रेकआउट की वैधता में सुधार होता है। यह ब्रेकआउट कैंडल के वॉल्यूम और पिछले N अवधियों के औसत वॉल्यूम के अनुपात की गणना करके किया जा सकता है।

-

बहु-समय फ्रेम विश्लेषण : उच्च समय फ्रेम के ट्रेंड दिशा फिल्टर को शामिल करें, केवल तभी एंट्री करें जब दैनिक या घंटे के ट्रेंड की दिशा ब्रेकआउट की दिशा से मेल खाती हो, जिससे जीत दर में सुधार होता है। उच्च समय फ्रेम ट्रेंड को निर्धारित करने के लिए सरल मूविंग एवरेज ढलान या अधिक उन्नत ट्रेंड संकेतक का उपयोग किया जा सकता है।

-

धन प्रबंधन अनुकूलन : गतिशील पोजीशन साइज़िंग तंत्र लागू करें, जो ऐतिहासिक अस्थिरता, वर्तमान खाता आकार और हाल के प्रदर्शन के आधार पर अनुबंधों की संख्या को स्वचालित रूप से समायोजित करता है, जिससे अधिक सटीक जोखिम नियंत्रण संभव होता है। उदाहरण के लिए, लगातार लाभ के बाद धीरे-धीरे पोजीशन बढ़ाएँ, लगातार हानि के बाद पोजीशन कम करें।

-

मशीन लर्निंग मॉडल एकीकरण : ब्रेकआउट गुणवत्ता का मूल्यांकन करने के लिए मशीन लर्निंग मॉडल शामिल करें, ऐतिहासिक डेटा पर मॉडल को प्रशिक्षित करके सबसे सफल होने वाले ब्रेकआउट पैटर्न की पहचान करें। विशेषताओं में ओपनिंग रेंज का आकार, बाजार अस्थिरता, पिछले ट्रेडिंग दिन का मूल्य व्यवहार, विशिष्ट समय पैटर्न आदि शामिल हो सकते हैं।

-

दूसरा मौका ट्रेडिंग लॉजिक को बढ़ाना : दूसरे मौका ट्रेड के ट्रिगर शर्तों को अनुकूलित करें, न केवल प्रारंभिक ट्रेड विफलता पर आधारित, बल्कि बाजार संरचना में बदलाव और नए मोमेंटम इंडिकेटर पर भी विचार करें, जिससे दूसरे ट्रेड की सफलता दर में सुधार होता है।

-

व्यक्तिगत इंस्ट्रूमेंट पैरामीटर : विभिन्न ट्रेडिंग इंस्ट्रूमेंट्स के लिए अनुकूलित पैरामीटर सेट विकसित करें, प्रत्येक इंस्ट्रूमेंट की अद्वितीय अस्थिरता विशेषताओं और मूल्य व्यवहार को ध्यान में रखते हुए। उदाहरण के लिए, अधिक अस्थिर इंस्ट्रूमेंट को अधिक ढीली फिल्टर सेटिंग और अधिक रूढ़िवादी जोखिम-लाभ अनुपात की आवश्यकता हो सकती है।

-

बाजार भावना संकेतकों का एकीकरण : VIX सूचकांक या अन्य बाजार भावना संकेतकों को शामिल करें, अत्यधिक बाजार भावना अवधि के दौरान रणनीति पैरामीटर समायोजित करें या अस्थायी रूप से ट्रेडिंग बंद करें, उच्च अनिश्चितता वाले वातावरण से बचें।

सारांश

ओपनिंग रेंज ब्रेकआउट ATR ट्रेलिंग स्टॉप लॉस रणनीति एक सुसंरचित मात्रात्मक ट्रेडिंग सिस्टम है, जो ओपनिंग रेंज ब्रेकआउट, स्मार्ट फिल्टर तंत्र, लचीले एंट्री विकल्प और उन्नत जोखिम प्रबंधन सुविधाओं को कुशलता से जोड़ती है। यह रणनीति विशेष रूप से अमेरिकी शेयर और वायदा बाजारों में इंट्राडे ट्रेडिंग के लिए उपयुक्त है, जो खुलने के बाद दिशात्मक ब्रेकआउट को पकड़कर लाभ कमाती है।

रणनीति का मूल्य इसके बहु-स्तरीय सत्यापन तंत्र और जोखिम प्रबंधन प्रणाली में निहित है, जो शैडो और दूरी फिल्टर के माध्यम से झूठे ब्रेकआउट ट्रेडों को काफी कम करती है, साथ ही जोखिम-लाभ अनुपात गुणक और ATR ट्रेलिंग स्टॉप का उपयोग करके एकसमान जोखिम एक्सपोजर और लाभ सुरक्षा सुनिश्चित करती है। दूसरा मौका ट्रेडिंग फीचर रणनीति में अनुकूलन क्षमता और अतिरिक्त लाभ के अवसर जोड़ता है।

हालाँकि इस रणनीति के कई लाभ हैं, उपयोगकर्ताओं को पैरामीटर अनुकूलन के महत्व पर ध्यान देना चाहिए, विभिन्न बाजारों और इंस्ट्रूमेंट्स के लिए लक्षित समायोजन की आवश्यकता हो सकती है ताकि सर्वोत्तम परिणाम प्राप्त हो सकें। साथ ही, ट्रेडरों को इस रणनीति को एक पूर्ण ट्रेडिंग सिस्टम के हिस्से के रूप में उपयोग करने की सलाह दी जाती है, व्यापक बाजार विश्लेषण और जोखिम प्रबंधन सिद्धांतों के साथ संयोजन में।

अनुशंसित अनुकूलन दिशाओं, विशेष रूप से अनुकूली पैरामीटर, बहु-समय फ्रेम विश्लेषण और बढ़ी हुई धन प्रबंधन प्रणाली को लागू करके, इस रणनीति में अपनी स्थिरता और लाभप्रदता में और सुधार करने की क्षमता है, और यह पेशेवर ट्रेडरों के टूलबॉक्स में एक शक्तिशाली उपकरण बन सकती है।

/*backtest

start: 2025-07-18 00:00:00

end: 2025-07-30 00:00:00

period: 30m

basePeriod: 30m

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("Casper SMC 5min ORB - Roboquant AI", overlay=true, default_qty_type=strategy.fixed, default_qty_value=1, max_bars_back=500, calc_on_order_fills=true, calc_on_every_tick=false, initial_capital=50000, currency=currency.USD)

// === STRATEGY SETTINGS ===- 1