🎯 ये कैसी जादुई रणनीति है? 20 संकेतक एक साथ आए!

क्या आप जानते हैं? यह रणनीति आपके ट्रेडिंग के लिए एक सुपर इंटेलिजेंट AI सहायक की तरह काम करती है! यह एक साथ 20 अलग-अलग बाजार संकेतों की निगरानी करती है, और केवल तब ट्रेडिंग सुझाव देती है जब अधिकांश संकेतक कहें "हाँ"। ठीक वैसे ही जैसे घर खरीदते समय लोकेशन, कीमत, डिज़ाइन, ट्रांसपोर्ट... सब कुछ देखकर ही निर्णय लेते हैं!

याद रखें! यह कोई सामान्य एक-संकेतक रणनीति नहीं है, बल्कि एक "बहु-आयामी सामंजस्य प्रणाली" है। सोचिए, अगर सिर्फ एक दोस्त कहे कि कोई शेयर अच्छा है, तो आप संदेह कर सकते हैं; लेकिन अगर 20 विशेषज्ञ दोस्त सब कहें कि यह अच्छा है, तो क्या आपको अधिक भरोसा नहीं होगा?

📊 मुख्य हथियारों का भंडार: एक बड़ा खुलासा

प्रवृत्ति पहचान के तीन तलवारबाज 🗡️

- तेज़ EMA(5) बनाम धीमी EMA(13): अल्पकालिक प्रवृत्ति परिवर्तन को पकड़ें

- प्रवृत्ति फ़िल्टर EMA(34): मध्यम अवधि की दिशा की पुष्टि करें

- मुख्य प्रवृत्ति EMA(89): बड़ी दिशा को समझें, छोटे उतार-चढ़ाव से भ्रमित न हों

बहु-समय सीमा विश्लेषण ⏰

यह फीचर बहुत शानदार है! रणनीति एक साथ 1 घंटे और 4 घंटे की प्रवृत्ति देखती है, जैसे आप गाड़ी चलाते समय सामने की सड़क और नेविगेशन का समग्र रास्ता दोनों देखते हैं। इससे "छोटी समय सीमा में तेज़ी, बड़ी समय सीमा में मंदी" जैसी अजीब स्थिति से बचा जा सकता है!

स्मार्ट जोखिम प्रबंधन 🛡️

- गतिशील पोजीशन आकार: बाजार की अस्थिरता के अनुसार स्वचालित रूप से दांव का आकार समायोजित करें

- चरणबद्ध लाभ लेना: लालच न करें, थोड़ा-थोड़ा लाभ लेते रहें

- मूविंग स्टॉप-लॉस: लाभ सुरक्षा का जादुई उपकरण

🔥 20 सुरक्षा वाली ट्रेडिंग तर्क

लॉन्ग सिग्नल के लिए आवश्यक:

- प्रवृत्ति ऊपर: सभी EMA बुलिश क्रम में हों

- गति पर्याप्त: RSI, MACD, स्टोकास्टिक RSI सब हरी झंडी दें

- वॉल्यूम का साथ: बढ़े हुए वॉल्यूम के साथ ऊपर जाना ही सच्चा उछाल है

- बाजार संरचना स्वस्थ: ऊंचाई लगातार बढ़ रही हो

- तरलता समर्थन: महत्वपूर्ण समर्थन स्तर बरकरार हों

शॉर्ट सिग्नल इसके विपरीत!

गलतियों से बचने की मार्गदर्शिका ⚠️: रणनीति में "बोलिंजर बैंड स्क्वीज़ डिटेक्शन" भी है, जो बाजार के अत्यधिक शांत होने पर ट्रेडिंग रोक देता है, ताकि साइडवेज़ बाजार में बार-बार चूना न लगे!

💰 अधिकतम लाभ का गुप्त हथियार

चरणबद्ध लाभ लेने की रणनीति 📈

- पहला लाभ लेना: 2 गुना रिस्क-रिवॉर्ड पर 30% पोजीशन बेचें

- दूसरा लाभ लेना: 3.5 गुना पर 40% और बेचें

- बची हुई पोजीशन: मूविंग स्टॉप-लॉस से सुरक्षित, लाभ को दौड़ने दें

स्मार्ट स्टॉप-लॉस अपग्रेड 🎯

2.5 गुना लाभ पर पहुंचने के बाद, स्टॉप-लॉस स्वचालित रूप से लागत मूल्य पर आ जाता है, यह सुनिश्चित करता है कि यह ट्रेड कम से कम घाटे में न जाए। यह आपके लाभ के लिए बीमा की तरह है!

डायनामिक ट्रेलिंग स्टॉप-लॉस 🏃♂️

जब लाभ एक निश्चित स्तर पर पहुंच जाता है, तो स्टॉप-लॉस एक छाया की तरह कीमत का पीछा करता है, जो लाभ को सुरक्षित रखता है और ऊपर जाने की गुंजाइश भी देता है।

🚀 यह रणनीति इतनी शानदार क्यों है?

- पूर्ण कवरेज: तकनीकी विश्लेषण, धन प्रबंधन, जोखिम नियंत्रण - कोई कमी नहीं

- स्मार्ट फ़िल्टरिंग: 20 शर्तों की परत-दर-परत जांच, सफलता दर काफी बढ़ जाती है

- अनुकूलनशीलता: बहु-समय सीमा विश्लेषण, विभिन्न बाजार स्थितियों के लिए उपयुक्त

- मानवीय डिज़ाइन: स्वचालित निष्पादन, भावनात्मक ट्रेडिंग से बचाव

यह रणनीति एक अनुभवी ट्रेडिंग टीम को कोड में बदलने जैसी है, जो 24 घंटे बिना रुके आपके लिए सर्वश्रेष्ठ ट्रेडिंग अवसर खोजती रहती है!

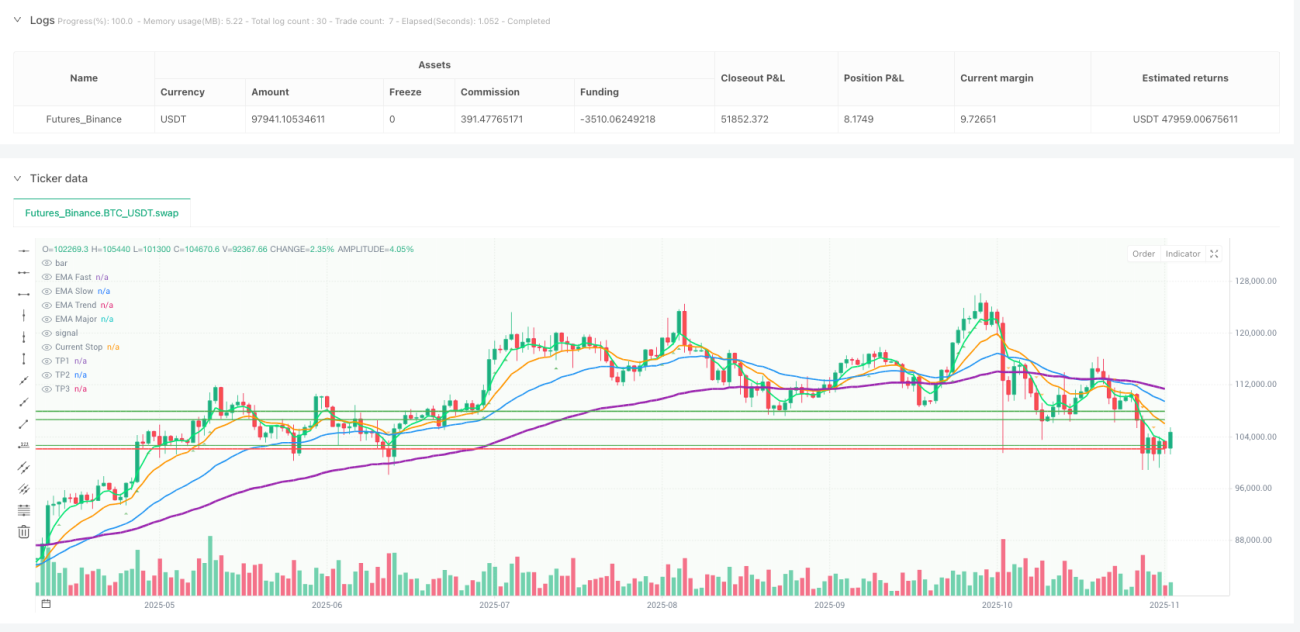

/*backtest

start: 2024-11-12 00:00:00

end: 2025-11-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy('Amir Mohammad Lor ', shorttitle='MPF', overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=15, pyramiding=0, max_bars_back=1000)

// === INPUTS ===- 1