Strategi Akumulasi Saat Koreksi Pola

Ikhtisar

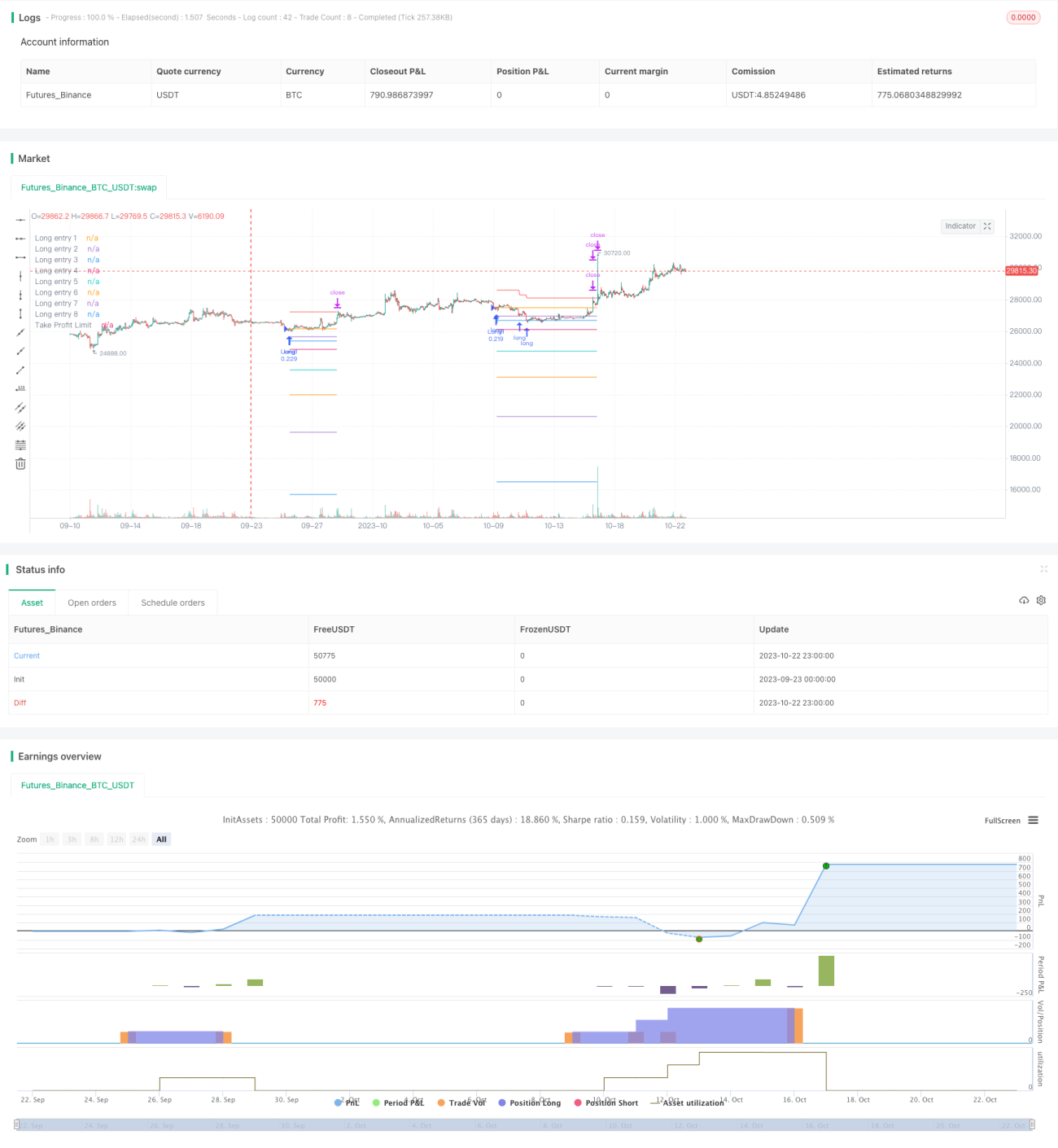

Strategi ini menggabungkan indikator RSI dan rata-rata pergerakan harga untuk mencari peluang oversold saat harga saham jatuh di bawah rata-rata pergerakan, kemudian membuka posisi beli. Seiring harga semakin turun, strategi akan menambah posisi secara bertahap sesuai persentase yang telah ditentukan untuk mencapai biaya rata-rata kepemilikan. Ketika laba posisi mencapai persentase take profit yang dikonfigurasi, strategi akan memilih untuk menutup posisi. Pada saat yang sama, strategi memperkenalkan mekanisme take profit progresif, yang secara dinamis menyesuaikan harga take profit keseluruhan posisi berdasarkan laba dari setiap posisi yang telah direalisasikan. Ini dapat secara efektif mengurangi risiko kerugian dan mencapai keluar secara bertahap.

Prinsip Strategi

-

Ketika indikator RSI di bawah garis oversold 29, dan harga penutupan di bawah rata-rata pergerakan, lakukan pembelian posisi pertama.

-

Ketika harga turun 2% dari posisi pertama, tambah posisi beli; ketika penurunan mencapai 3%, tambah posisi ketiga, dan seterusnya hingga maksimal 8 kali penambahan posisi. Ini mencapai efek pembukaan posisi secara bertahap.

-

Setiap kali posisi dibuka, harga pembukaan pada saat itu dicatat. Titik-titik harga ini adalah harga referensi masuk. Gambarkan garis harga ini pada grafik.

-

Setelah posisi dibuka, hitung harga rata-rata kepemilikan. Gunakan 3% dari harga rata-rata sebagai take profit untuk setiap posisi, dan 4% sebagai take profit keseluruhan posisi.

-

Ketika harga naik melebihi harga take profit suatu posisi, pilih untuk menutup posisi tersebut.

-

Metode perhitungan take profit progresif: setiap kali satu posisi ditutup, kurangi laba yang direalisasikan dari posisi tersebut dari harga take profit keseluruhan. Ini membuat garis take profit perlahan turun, dan hanya ketika laba semua posisi cukup untuk menutupi kerugian maksimum, semua posisi akan ditutup.

-

Ketika harga menyentuh garis take profit progresif, pilih untuk menutup semua posisi.

Analisis Keunggulan

-

Indikator RSI dapat menilai zona oversold dengan cukup akurat, membantu menangkap peluang pembalikan.

-

Penambahan posisi secara bertahap beberapa kali memungkinkan rata-rata biaya kepemilikan di titik rendah.

-

Take profit progresif dapat mengurangi risiko kerugian dan mencapai keluar secara bertahap. Bahkan jika terjadi kerugian, dapat dikendalikan dalam kisaran tertentu.

-

Rasio take profit dan rasio penambahan posisi yang dapat dikonfigurasi memungkinkan penyesuaian risiko strategi sesuai pasar.

-

Menggambarkan garis referensi pembukaan dan garis take profit pada grafik memudahkan visualisasi distribusi posisi.

Analisis Risiko

-

Dalam pasar yang berfluktuasi, dapat memicu pembukaan dan take profit berulang kali, menyebabkan kerugian slippage akibat frekuensi transaksi yang tinggi. Parameter RSI dapat dilonggarkan untuk mengurangi jumlah transaksi.

-

Penentuan jumlah dan rasio penambahan posisi yang tidak tepat dapat menyebabkan overtrading. Harus dikonfigurasi secara hati-hati sesuai kondisi dana.

-

Jika pasar terus turun dan posisi ditambah, mungkin menghadapi risiko tanpa batas. Batas maksimal penambahan posisi harus ditentukan, dan rasio penambahan posisi terakhir harus konservatif.

-

Jika rasio take profit terlalu kecil, dapat menyebabkan take profit terlalu dini. Rasio take profit yang sesuai harus ditetapkan berdasarkan data backtest historis.

Arah Optimasi

-

Dapat memperkenalkan indikator seperti MACD untuk memfilter sinyal RSI, mengurangi transaksi tidak efektif.

-

Dapat mengatur stop loss berdasarkan ATR untuk menghindari kerugian besar akibat pergerakan ekstrem.

-

Dapat mengoptimalkan parameter seperti jumlah penambahan posisi, rasio, dan rasio take profit agar strategi lebih sesuai dengan instrumen yang berbeda.

-

Dapat menyesuaikan rasio take profit secara cerdas berdasarkan volatilitas, melonggarkan saat volatilitas tinggi.

Kesimpulan

Strategi ini memanfaatkan indikator RSI untuk menilai zona oversold dan menggabungkannya dengan rata-rata pergerakan harga untuk melakukan perdagangan pembalikan. Pada saat yang sama, menggunakan mekanisme penambahan posisi cerdas dan take profit progresif untuk mencapai strategi beli yang efisien dengan tetap mengendalikan risiko. Dengan mengoptimalkan parameter indikator, mekanisme take profit, dan lainnya, strategi dapat menjadi lebih stabil dan efisien. Strategi ini dapat diterapkan secara luas pada instrumen keuangan yang memiliki karakteristik pembalikan tren, seperti indeks berjangka, mata uang kripto, dan memiliki nilai investasi praktis.

- 1