Sistem Terobosan Pembalikan Oversold Ganda

Ringkasan

Sistem Pembalikan Ganda Overextended adalah strategi kuantitatif yang menggabungkan pelacakan tren dan perdagangan pembalikan. Strategi ini menghasilkan sinyal beli dengan menghitung apakah harga saham mengalami sinyal overextended berurutan dibandingkan dengan harga penutupan N hari sebelumnya; pada saat yang sama, menggabungkan perhitungan rata-rata bergerak T3 dengan parameter tertentu untuk menghasilkan sinyal jual, sehingga melindungi keuntungan.

Prinsip Strategi

Strategi ini terdiri dari dua bagian:

-

Sistem Pembalikan 123

Menurut deskripsi dalam buku, sistem pembalikan ini mengamati perubahan harga penutupan selama N hari terakhir. Jika harga penutupan hari ini lebih tinggi dari hari sebelumnya, dan harga penutupan hari sebelumnya lebih rendah dari dua hari sebelumnya, maka ini dianggap sebagai sinyal overextended selama dua hari berturut-turut, dan sistem menghasilkan sinyal beli. Selain itu, sistem ini juga menggabungkan indikator STOCH. Jika garis cepat STOCH hari ini lebih rendah dari garis lambat, maka validitas sinyal beli semakin dikonfirmasi.

-

Rata-rata Bergerak T3

Rata-rata bergerak T3 dihitung berdasarkan rumus tertentu yang menggabungkan rata-rata bergerak eksponensial dari harga. Dengan parameter tertentu, ia menyesuaikan sensitivitas rata-rata bergerak terhadap perubahan harga. Ketika harga menembus di atas rata-rata bergerak T3, sinyal jual dihasilkan.

Strategi ini menggabungkan kedua sinyal di atas: ketika sinyal beli dari sistem pembalikan 123 dan sinyal jual dari rata-rata bergerak T3 terpenuhi secara bersamaan, maka sinyal perdagangan yang sebenarnya dihasilkan.

Analisis Keunggulan

- Strategi perdagangan pembalikan, cocok untuk membeli di titik terendah, mengikuti pergerakan pemulihan dari overextended.

- Strategi rata-rata bergerak membantu mengunci keuntungan dan menghindari risiko.

- Kombinasi sinyal ganda dapat meningkatkan validitas sinyal dan mengurangi sinyal palsu.

- Menggabungkan keunggulan pelacakan tren dan perdagangan pembalikan.

- Parameter dapat disesuaikan secara fleksibel untuk beradaptasi dengan kondisi pasar yang berbeda.

Analisis Risiko

- Sinyal pembalikan dapat salah interpretasi, menghasilkan perdagangan yang merugi.

- Pengaturan parameter yang tidak tepat dapat menyebabkan perdagangan yang terlalu sering, meningkatkan biaya transaksi dan slippage.

- Sinyal jual dari rata-rata bergerak mungkin mengunci keuntungan terlalu dini.

- Risiko stop loss tetap ada saat pergerakan pasar yang ekstrem.

- Diperlukan optimalisasi parameter untuk memilih parameter terbaik bagi instrumen yang berbeda.

Untuk mengatasi risiko, langkah-langkah berikut dapat diambil:

- Menyesuaikan parameter perdagangan pembalikan secara tepat untuk memastikan validitas sinyal.

- Menyesuaikan parameter rata-rata bergerak untuk memperpanjang durasi kepemilikan.

- Menambahkan strategi stop loss untuk mengurangi kerugian per transaksi.

- Mengoptimalkan pemilihan parameter, memilih parameter berbeda untuk instrumen yang berbeda.

Arah Optimasi

Strategi ini dapat dioptimalkan dari beberapa aspek berikut:

-

Menambahkan kondisi filter untuk memastikan validitas sinyal perdagangan

Dapat menambahkan indikator teknis lain sebagai filter berdasarkan strategi asli, misalnya menambahkan kondisi breakout volume, sehingga menghindari perdagangan yang salah akibat noise.

-

Menyesuaikan pengaturan parameter untuk beradaptasi dengan lingkungan pasar

Dapat melakukan backtest dengan berbagai kombinasi parameter, memilih kombinasi parameter dengan return tertinggi untuk mengoptimalkan efek strategi. Juga dapat menetapkan parameter dinamis yang menyesuaikan secara real-time berdasarkan kondisi pasar.

-

Menggabungkan teknik pembelajaran mesin untuk optimasi adaptif strategi

Misalnya, dapat mengumpulkan data historis dalam jumlah besar, menggunakan pembelajaran mesin untuk melatih model guna memprediksi waktu beli/jual terbaik. Serta mengoptimalkan parameter strategi secara real-time.

-

Menetapkan parameter independen berdasarkan karakteristik instrumen yang berbeda

Karakteristik instrumen yang berbeda memerlukan parameter yang berbeda pula. Dapat melakukan backtest terpisah berdasarkan data masing-masing instrumen untuk menetapkan parameter independen.

Kesimpulan

Sistem Pembalikan Ganda Overextended menggabungkan keunggulan pelacakan tren dan perdagangan pembalikan. Ia dapat membeli pada harga rendah di fase overextended, dan mengambil keuntungan tepat waktu setelah tren menguntungkan. Kombinasi efektif antara sinyal pembalikan dan sinyal tren dari strategi ini dapat secara efektif menangkap peluang pembalikan sambil mengunci keuntungan. Meskipun masih ada risiko tertentu, hal ini dapat diperbaiki melalui optimalisasi parameter, penambahan filter, dan cara lain untuk beradaptasi dengan lingkungan pasar yang berbeda. Strategi ini memberikan ide yang efektif untuk perdagangan kuantitatif dan layak untuk dioptimalkan lebih lanjut serta diterapkan.

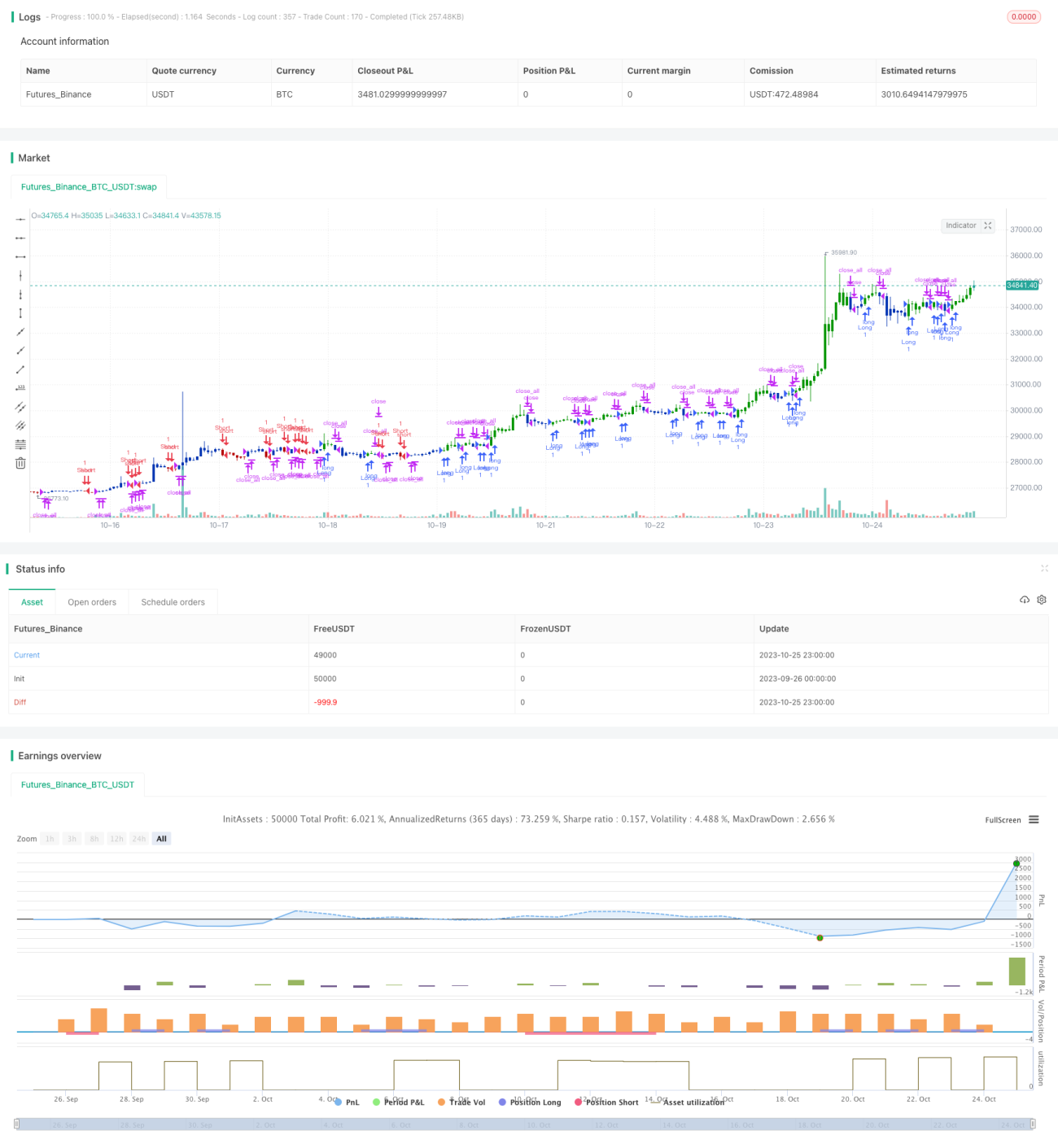

/*backtest

start: 2023-09-26 00:00:00

end: 2023-10-26 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 16/09/2021

// This is combo strategies for get a cumulative signal. - 1