Strategi Kombinasi Momentum dan Reversal

Gambaran Umum

Strategi ini menggabungkan dua indikator momentum untuk menemukan lebih banyak peluang trading. Indikator pertama adalah strategi pembalikan stochastic cepat-lambat yang diperkenalkan oleh Ulf Jensen dalam bukunya. Indikator kedua adalah Harga Sintetis Detrend (Detrended Synthetic Price) yang dikemukakan oleh John Ehlers. Strategi ini memanfaatkan sinyal dari kedua indikator secara bersamaan, hanya melakukan order ketika kedua indikator memberikan sinyal beli atau jual secara bersamaan.

Prinsip Strategi

Prinsip dari bagian pertama strategi pembalikan stochastic cepat-lambat adalah: lakukan posisi long ketika harga penutupan dua hari berturut-turut lebih rendah dari harga penutupan hari sebelumnya, dan garis cepat berada di atas garis lambat; lakukan posisi short ketika harga penutupan dua hari berturut-turut lebih tinggi dari harga penutupan hari sebelumnya, dan garis cepat berada di bawah garis lambat.

Rumus perhitungan Harga Sintetis Detrend pada bagian kedua adalah:

DSP = EMA(HL/2, periode 0,25) - EMA(HL/2, periode 0,5)

Di mana HL/2 adalah titik tengah harga tinggi dan rendah, EMA periode 0,25 mewakili tren jangka pendek harga, EMA periode 0,5 mewakili tren jangka panjang harga. Harga Sintetis Detrend mewakili besarnya kenaikan atau penurunan harga relatif terhadap siklus dominannya. Ketika DSP menembus ke atas dari ambang batas, itu menunjukkan bullish; ketika menembus ke bawah dari ambang batas, itu menunjukkan bearish.

Strategi ini mempertimbangkan sinyal dari kedua indikator secara komprehensif. Posisi hanya dibuka ketika kedua indikator memberikan sinyal beli atau jual secara bersamaan.

Analisis Keunggulan

- Menggunakan dua indikator untuk menyaring sinyal yang tidak pasti, dapat mengurangi kesalahan trading

- Kedua indikator saling memverifikasi, dapat meningkatkan keandalan sinyal

- Strategi pembalikan stochastic cepat-lambat dapat menangkap peluang pembalikan jangka pendek

- Harga Sintetis Detrend dapat mengidentifikasi tren jangka menengah dan panjang

- Menggabungkan dua indikator, dapat menangkap pembalikan dan mengikuti tren, fleksibilitas tinggi

Analisis Risiko

- Indikator stochastic cepat-lambat berkinerja buruk di pasar yang bergerak sideways

- Harga Sintetis Detrend dapat memberikan sinyal palsu sebelum titik balik tren

- Hanya bertransaksi ketika kedua indikator memberikan sinyal secara bersamaan, mungkin melewatkan beberapa peluang

- Perlu mengatur parameter dengan benar agar efek kombinasi optimal

Arah Optimasi

- Dapat menguji parameter yang berbeda untuk mengoptimalkan efektivitas indikator

- Dapat mencoba bobot indikator yang berbeda, seperti menunda sinyal Harga Sintetis Detrend

- Dapat menambahkan stop loss untuk mengendalikan risiko

- Dapat menggabungkan lebih banyak jenis indikator yang berbeda untuk membangun model multi-faktor

Kesimpulan

Strategi ini menggabungkan dua indikator momentum yang berbeda, meningkatkan kualitas sinyal melalui penyaringan ganda, mengendalikan risiko sambil menjaga frekuensi trading. Namun, perlu diperhatikan keterbatasan indikator itu sendiri dan mengoptimalkan parameter dengan tepat. Jika dapat dioptimalkan secara berkelanjutan, strategi ini berpotensi memperoleh keuntungan berlebih dibandingkan pasar.

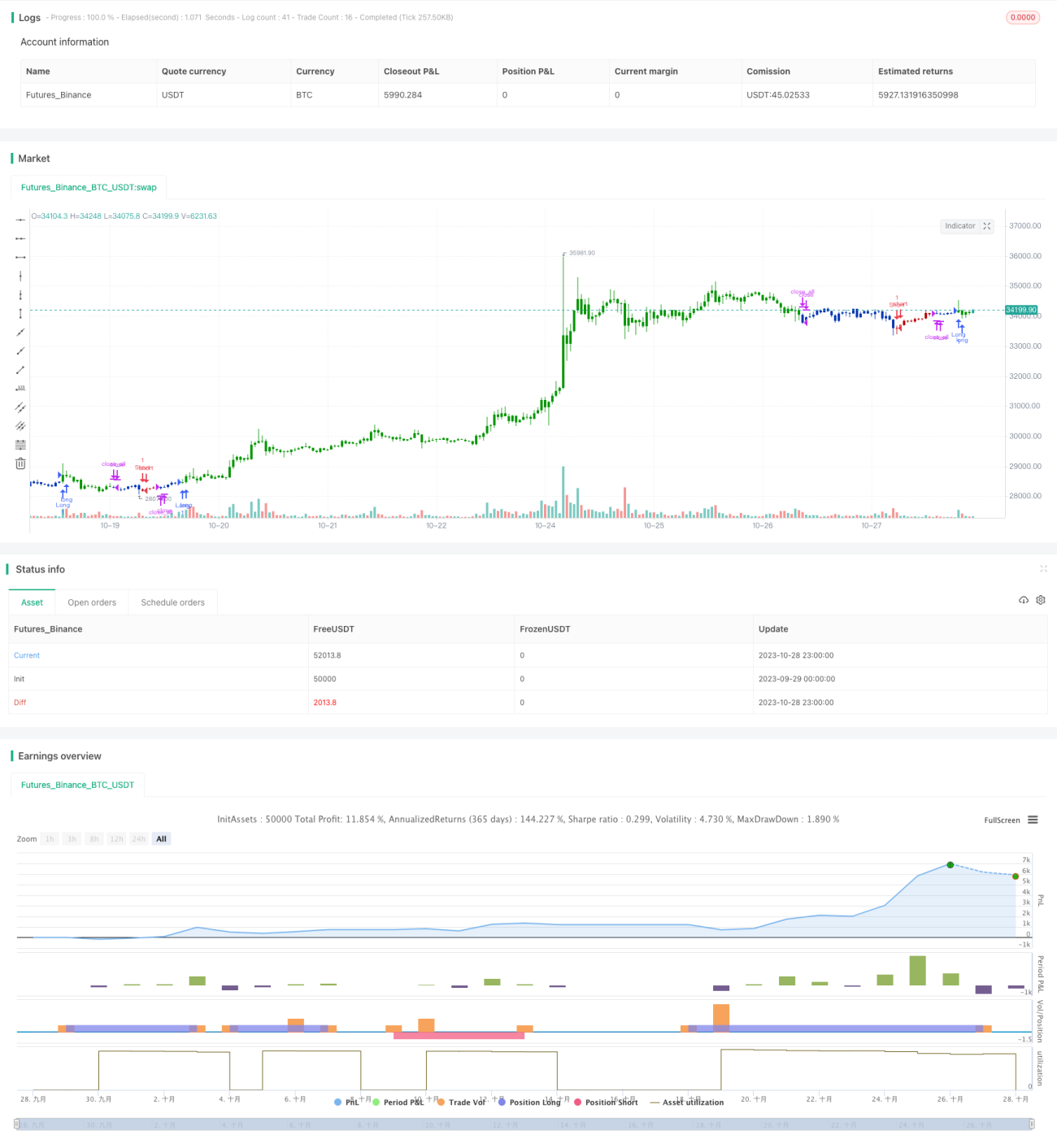

/*backtest

start: 2023-09-29 00:00:00

end: 2023-10-29 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 18/11/2019

// This is combo strategies for get a cumulative signal. - 1