Strategi Kuantitatif Pelacakan Tren Berbasis SAR

Gambaran Umum

Strategi Spekulasi Gap adalah strategi trading kuantitatif yang mengikuti tren. Ia menggunakan kurva halus SAR sebagai sinyal trading utama, dilengkapi dengan berbagai filter seperti EMA, Squeeze Momentum, dan Volatility Oscillator. Dengan mengonfigurasi parameter SAR, strategi ini mengidentifikasi titik pembalikan tren untuk melacak tren dengan risiko rendah. Ini adalah strategi yang sangat cocok untuk investasi jangka menengah hingga panjang.

Prinsip Strategi

Strategi ini menggunakan Parabolic SAR sebagai indikator sinyal trading utama. SAR mampu menentukan titik pembalikan tren harga secara efektif. Ketika tanda SAR berubah, itu berarti tren telah berbalik. Strategi ini biasanya menghasilkan sinyal beli atau jual saat SAR berbalik.

Selain itu, strategi juga menyediakan opsi breakout SAR. Artinya, sebelum SAR sepenuhnya berbalik, jika harga telah menembus nilai SAR terakhir, sinyal akan dihasilkan. Hal ini dapat meningkatkan sensitivitas strategi.

Untuk menyaring sinyal palsu, strategi ini juga menyertakan tiga filter tambahan: EMA, Squeeze Momentum, dan Volatility Oscillator. Filter-filter ini dapat digunakan secara terpisah atau dikombinasikan untuk mengonfirmasi reliabilitas tren harga dan sinyal trading.

Terakhir, strategi menyediakan tiga metode stop loss dan take profit: stop loss tetap, take profit tetap, dan stop loss berdasarkan rasio risk-reward. Hal ini memungkinkan strategi beradaptasi secara fleksibel dengan karakteristik berbagai jenis instrumen trading.

Analisis Keunggulan

-

SAR mampu menentukan pembalikan tren harga secara akurat dan menangkap tren harga baru tepat waktu, cocok untuk pelacakan tren jangka menengah hingga panjang.

-

Pengaturan filter berganda mengurangi probabilitas breakout palsu, meningkatkan keandalan sinyal.

-

Konfigurasi sederhana dan fleksibel, parameter dapat disesuaikan untuk berbagai instrumen trading.

-

Menyediakan berbagai cara stop loss dan take profit, memungkinkan keseimbangan antara risiko dan imbal hasil.

-

Dapat langsung terhubung dengan robot trading untuk mewujudkan trading otomatis.

Analisis Risiko

-

Di pasar yang tidak bertren, mungkin muncul lebih banyak sinyal palsu dan trading yang tidak efektif.

-

Pengaturan parameter SAR yang tidak tepat juga akan mempengaruhi akurasi sinyal.

-

Sebagai strategi pelacakan tren, dalam pasar yang sangat bergejolak mudah mencapai level stop loss.

Untuk mengatasi risiko di atas, parameter SAR atau parameter filter dapat disesuaikan untuk mengurangi probabilitas trading yang tidak efektif. Batasan stop loss juga dapat dilonggarkan untuk menahan fluktuasi pasar yang lebih besar.

Arah Optimasi

-

Optimasi Parameter SAR. Parameter step dan increment SAR dapat dioptimalkan melalui data backtest historis untuk mendapatkan strategi trading yang lebih stabil dan efisien.

-

Memasukkan Indikator Penentu Tren. Tambahkan indikator tambahan seperti MACD, DMI untuk meningkatkan kemampuan dalam menentukan tren.

-

Mengoptimalkan Rasio Risk-Reward. Sesuaikan persentase stop loss dan take profit tetap serta parameter rasio risk-reward untuk mengambil risiko lebih tinggi demi imbal hasil yang lebih besar.

-

Menambahkan Instrumen Forex. Saat ini strategi hanya mendukung trading aset kripto, dapat diperluas untuk mendukung instrumen forex, komoditas, dan sekuritas.

Kesimpulan

Spekulasi Gap adalah strategi kuantitatif pelacakan tren yang sangat praktis. Ia responsif, sinyalnya andal, dan melalui manajemen stop loss dan take profit dapat menghasilkan keuntungan stabil jangka panjang. Optimasi parameter dan aturan yang tepat dapat lebih meningkatkan efisiensi strategi. Ini adalah strategi kuantitatif efisien yang layak digunakan dalam jangka panjang.

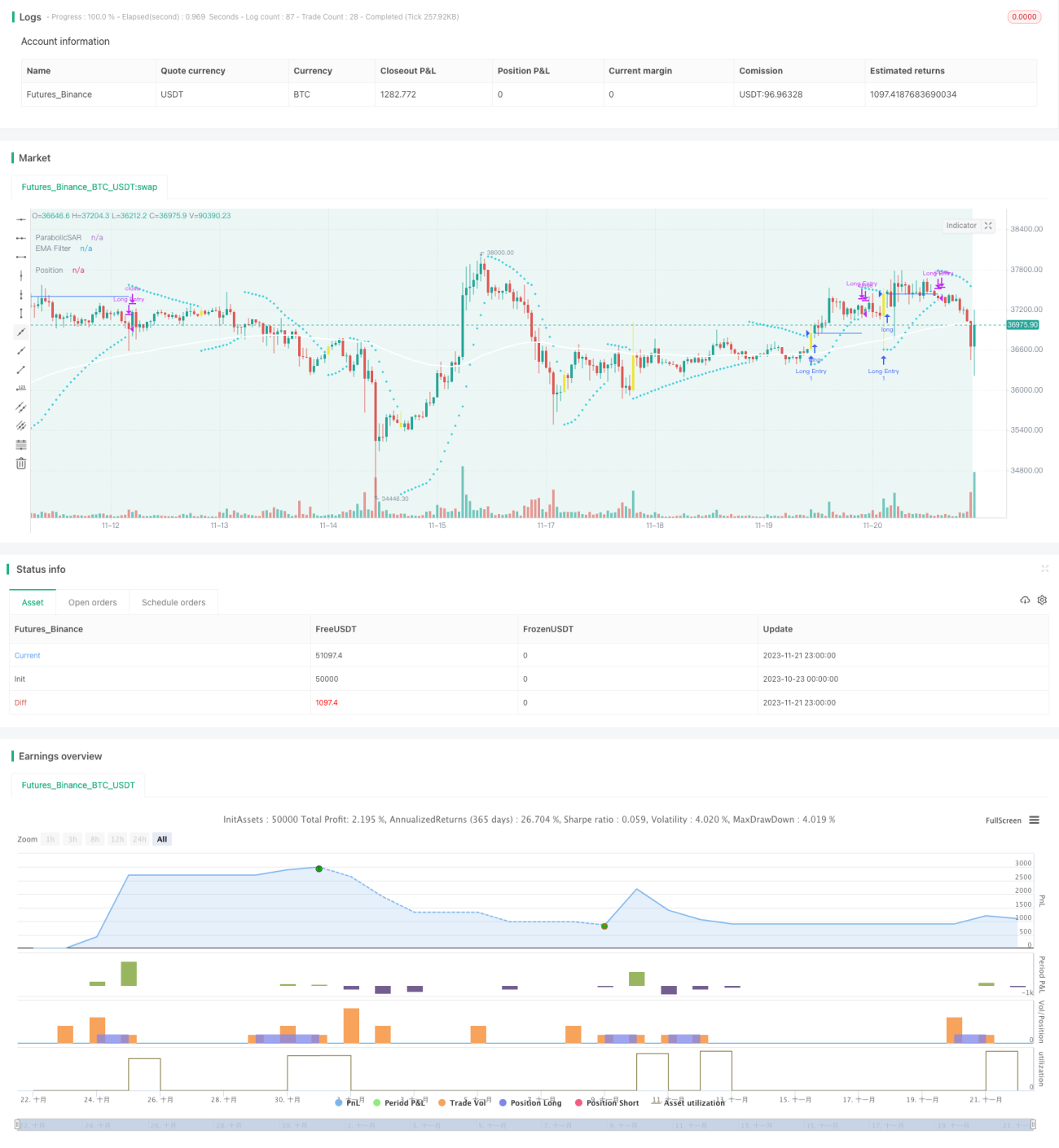

/*backtest

start: 2023-10-23 00:00:00

end: 2023-11-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//VERSION =================================================================================================================

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// This strategy is intended to study.- 1