Strategi Arbitrase Dua Moving Average

Ikhtisar

Strategi ini adalah strategi yang memanfaatkan pola rata-rata bergerak ganda untuk melakukan operasi arbitrase. Strategi ini menggabungkan dua sub-strategi, yaitu pembalikan pola 123 dan Elemen Volume Terbatas (FVE). Ketika keduanya menghasilkan sinyal beli atau jual secara bersamaan, dilakukan operasi arbitrase.

Prinsip Strategi

Pembalikan Pola 123

Sub-strategi ini berasal dari buku Ulf Jensen "How I Tripled My Money in the Futures Market". Sinyal diberikan dalam kondisi berikut:

- Ketika harga penutupan naik selama 2 hari berturut-turut, dan stokastik lambat 9 hari berada di bawah 50, lakukan posisi beli (long).

- Ketika harga penutupan turun selama 2 hari berturut-turut, dan stokastik cepat 9 hari berada di atas 50, lakukan posisi jual (short).

Elemen Volume Terbatas (FVE)

FVE adalah indikator volume murni. Indikator ini menilai apakah dana masuk atau keluar berdasarkan besarnya kenaikan/penurunan harga dan volume perdagangan.

Sinyal diberikan ketika indikator FVE pada dua bar terakhir naik atau turun secara bersamaan.

Analisis Keunggulan

Strategi ini menggabungkan dua indikator untuk menilai tren pasar dan aliran dana, sehingga dapat menghindari sinyal palsu secara efektif. Kedua sub-strategi juga memiliki karakteristik pembalikan, sehingga dapat dimanfaatkan untuk arbitrase guna memperoleh keuntungan.

Selain itu, ketika pola rata-rata bergerak ganda muncul, ini menunjukkan keselarasan tren jangka pendek dan menengah, sehingga memiliki stabilitas yang kuat.

Analisis Risiko

Strategi ini bergantung pada pola rata-rata bergerak. Ketika pasar bergerak sideways (konsolidasi), sinyal palsu sering terjadi dan dapat menyebabkan kerugian. Selain itu, kegagalan pembalikan adalah risiko yang umum.

Risiko dapat dikendalikan dengan menyesuaikan parameter secara tepat agar strategi lebih kokoh, atau dengan menetapkan stop loss.

Arah Optimalisasi

Dapat diuji berbagai jenis indikator rata-rata bergerak untuk menemukan kombinasi terbaik. Juga dapat diperkenalkan indikator bantu lainnya seperti indikator kekuatan relatif atau indikator volatilitas untuk menghindari sinyal palsu.

Selain itu, dapat dipelajari cara menyesuaikan parameter secara dinamis sesuai kondisi pasar agar strategi lebih adaptif. Algoritma pembelajaran mesin dan jaringan saraf juga dapat dieksplorasi untuk mencapai adaptasi parameter otomatis.

Kesimpulan

Strategi arbitrase rata-rata bergerak ganda ini mengintegrasikan dua indikator berpola pembalikan untuk pengambilan keputusan, sehingga dapat menghindari risiko sampai batas tertentu. Namun, karena bergantung pada pola rata-rata bergerak, masih diperlukan optimalisasi lebih lanjut agar strategi lebih kokoh. Secara keseluruhan, strategi ini menyediakan kerangka dasar untuk perdagangan arbitrase jangka pendek dan layak untuk diteliti lebih lanjut.

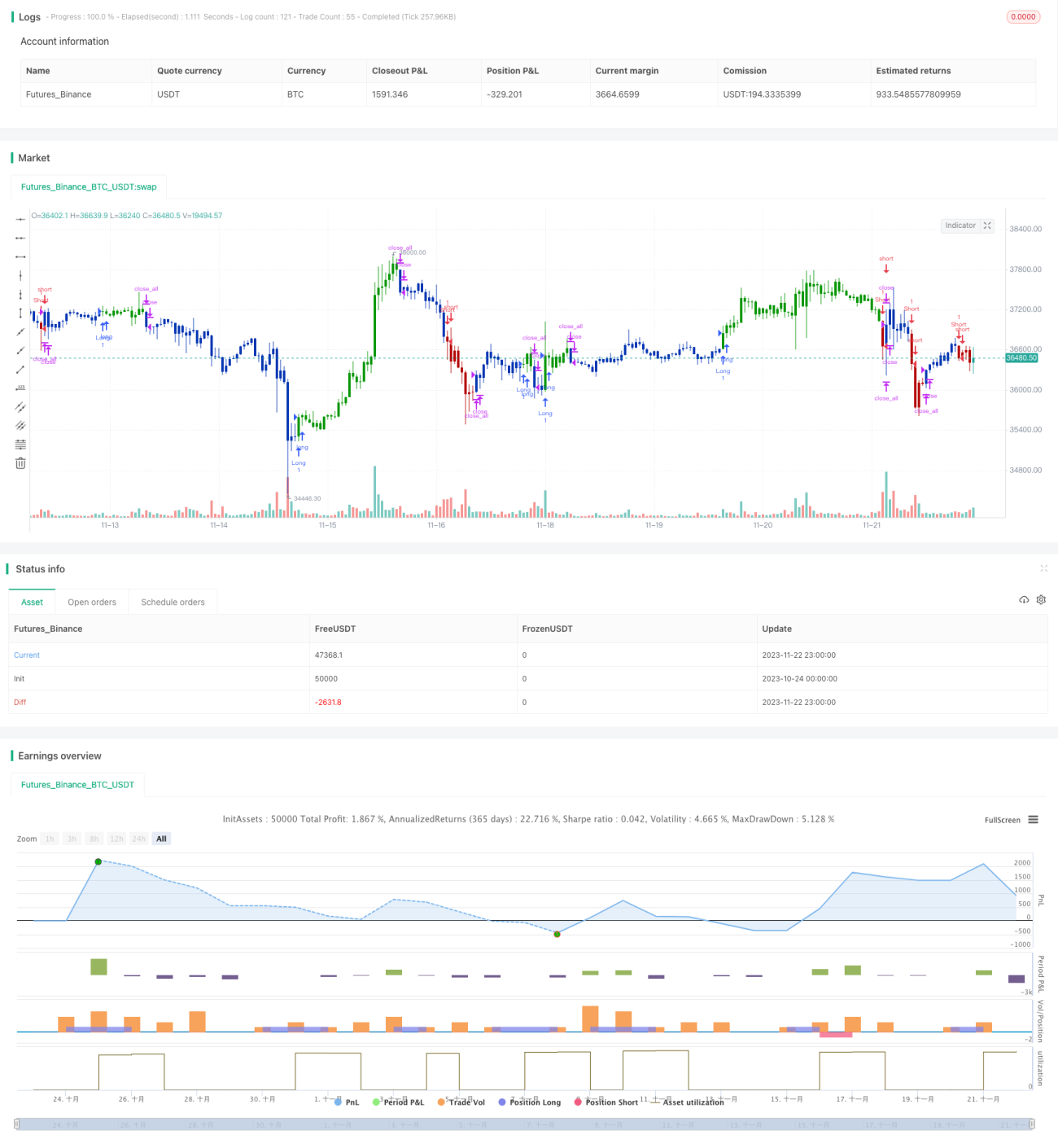

/*backtest

start: 2023-10-24 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 25/08/2020

// This is combo strategies for get a cumulative signal. - 1