Strategi trading berbasis EMA (Rata-rata Bergerak Eksponensial)

Ikhtisar

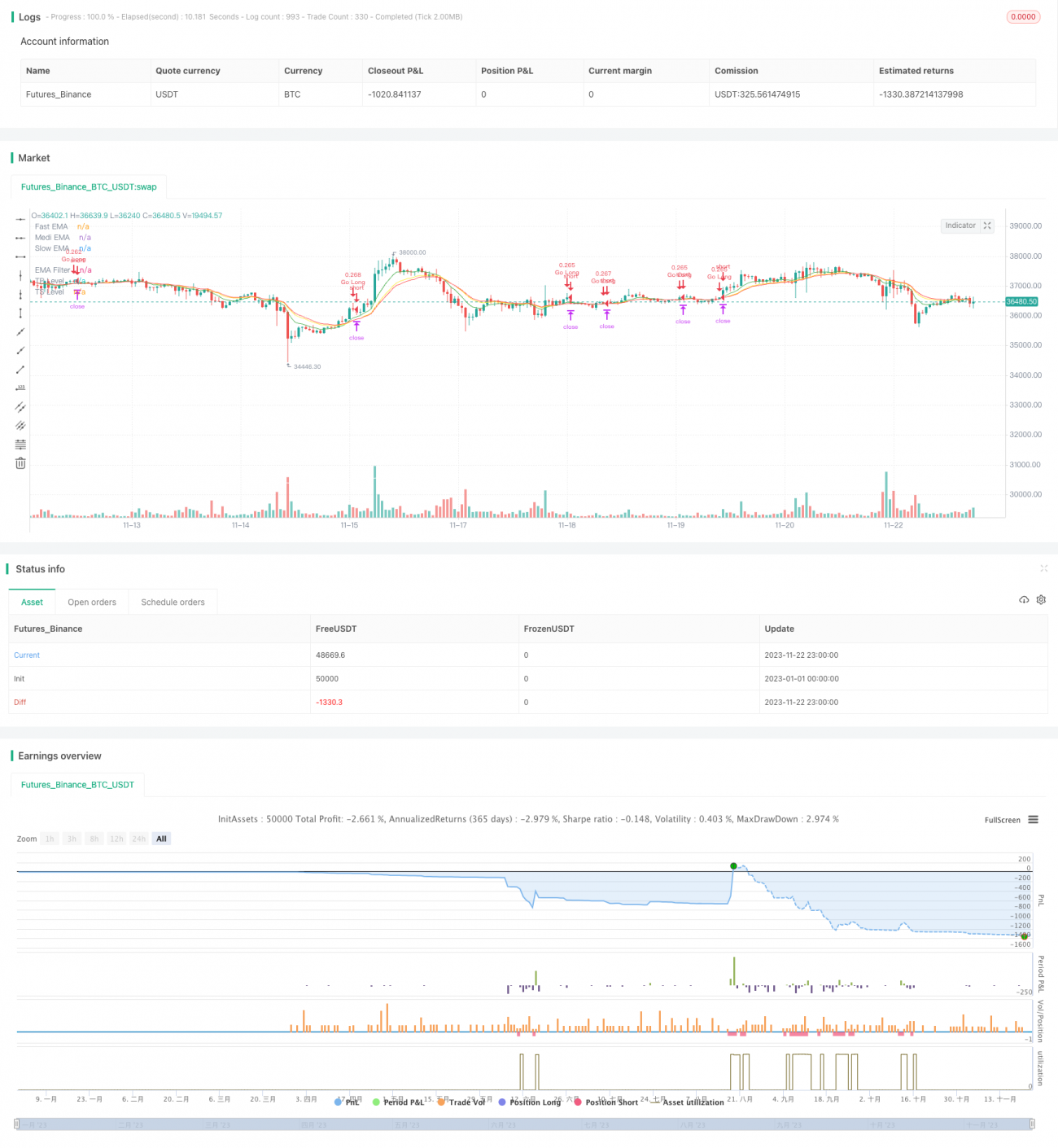

Strategi ini menggunakan 4 garis EMA dengan periode berbeda, dan menghasilkan sinyal trading berdasarkan urutannya, mirip dengan lampu lalu lintas merah, kuning, dan hijau. Oleh karena itu dinamai "Strategi Trading Lampu Lalu Lintas". Strategi ini menilai pasar secara komprehensif dari dua sudut pandang, yaitu tren dan pembalikan, untuk meningkatkan akurasi keputusan trading.

Prinsip Strategi

-

Menetapkan 3 garis EMA: garis cepat (periode 8), garis tengah (periode 14), garis lambat (periode 16), dan menambahkan 1 garis EMA berperiode panjang (periode 100) sebagai filter.

-

Menentukan urutan dari 3 garis EMA (cepat, tengah, lambat) dan persilangannya dengan filter untuk menentukan momen entry long dan short:

-

Ketika garis cepat menembus ke atas garis tengah, atau garis tengah menembus ke atas garis lambat, maka dianggap sebagai sinyal beli (long).

-

Ketika garis tengah menembus ke bawah garis cepat, maka dianggap sebagai sinyal tutup posisi beli.

-

Ketika garis cepat menembus ke bawah garis tengah, atau garis tengah menembus ke bawah garis lambat, maka dianggap sebagai sinyal jual (short).

-

Ketika garis tengah menembus ke atas garis cepat, maka dianggap sebagai sinyal tutup posisi jual.

-

-

Dengan mengamati urutan 3 garis EMA (cepat, tengah, lambat) untuk menentukan arah dan kekuatan tren, serta menggabungkannya dengan persilangan garis EMA dengan filter untuk menentukan titik pembalikan, strategi ini mencapai kombinasi organik antara mengikuti tren dan menangkap pembalikan.

Analisis Keunggulan

Strategi ini mengintegrasikan kelebihan dari pengikut tren dan trading pembalikan, sehingga dapat menangkap peluang pasar dengan lebih baik. Keunggulan utamanya meliputi:

- Menggunakan beberapa grup garis EMA, sehingga kemampuan analisis lebih kuat dan mengurangi sinyal palsu.

- Kondisi entry long dan short yang fleksibel, menghindari kehilangan peluang trading.

- Penggunaan garis EMA jangka pendek dan panjang secara tiga dimensi, memberikan penilaian yang komprehensif.

- Kondisi take profit dan stop loss yang dapat disesuaikan, memberikan kontrol risiko yang memadai.

Melalui optimasi parameter, strategi ini dapat beradaptasi dengan lebih banyak instrumen, dan menunjukkan profitabilitas serta stabilitas yang kuat dalam backtest.

Analisis Risiko

Risiko utama dari strategi ini meliputi:

- Ketika urutan beberapa grup garis EMA kacau, akan meningkatkan kesulitan analisis dan menyebabkan keraguan dalam trading.

- Tidak dapat menyaring sinyal palsu akibat fluktuasi pasar yang tidak normal secara efektif, misalnya kerugian saat terjadi osilasi besar.

- Jika parameter tidak diatur dengan tepat, kondisi take profit dan stop loss mungkin terlalu longgar atau terlalu ketat, sehingga mengakibatkan hilangnya profit atau kerugian berlebihan.

Disarankan untuk lebih meningkatkan stabilitas strategi dan mengendalikan risiko dengan cara mengoptimalkan parameter, menetapkan level stop loss, dan beroperasi dengan hati-hati.

Arah Optimasi

Arah optimasi utama untuk strategi ini:

- Menyesuaikan parameter periode garis EMA agar lebih cocok dengan berbagai instrumen.

- Menambahkan filter indikator lain, seperti MACD, Bollinger Bands, dll., untuk meningkatkan akurasi penilaian.

- Mengoptimalkan rasio take profit dan stop loss untuk mencapai keseimbangan terbaik antara risiko dan imbal hasil.

- Menambahkan mekanisme stop loss adaptif, seperti stop loss ATR, untuk lebih mengendalikan risiko penurunan.

Melalui penyesuaian parameter di berbagai aspek dan pengenalan metode kontrol risiko, stabilitas dan profitabilitas strategi dapat terus ditingkatkan.

Kesimpulan

Strategi Trading Lampu Lalu Lintas ini mengintegrasikan penilaian tren dan pembalikan, menggunakan 4 grup garis EMA untuk menghasilkan sinyal trading. Melalui optimasi parameter, strategi ini dapat beradaptasi dengan lebih banyak instrumen dan menunjukkan profitabilitas yang kuat dalam backtest. Ke depannya, dengan kontrol risiko yang lebih lanjut dan pengenalan indikator yang beragam, strategi ini berpotensi menjadi strategi trading kuantitatif yang stabil dan efisien.

/*backtest

start: 2023-01-01 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © maxits

// 4HS Crypto Market Strategy- 1