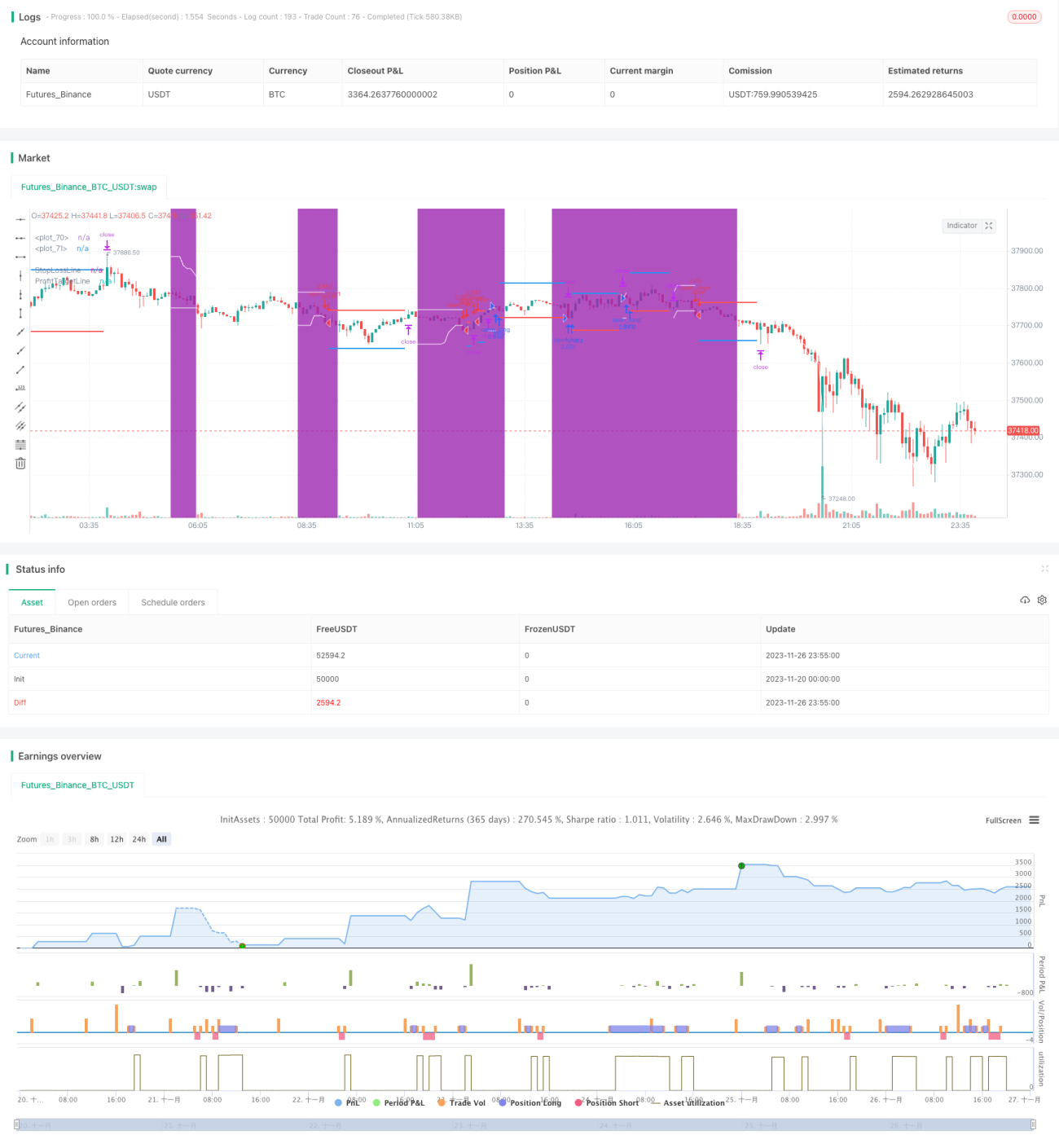

Strategi Trend Following Cerdas ADX

Gambaran Umum

Strategi ADX Smart Trend Following memanfaatkan Indeks Pergerakan Rata-rata (ADX) untuk menilai kekuatan tren, menangkap tren saat tren lemah, dan mengikuti tren untuk meraih keuntungan saat tren kuat. Strategi ini menggabungkan penilaian kekuatan tren dengan penembusan harga untuk menghasilkan sinyal perdagangan, termasuk dalam kategori strategi trend following.

Prinsip Strategi

Strategi ini terutama didasarkan pada Indeks Pergerakan Rata-rata (ADX) untuk menilai kekuatan tren saat ini. ADX menunjukkan kekuatan tren dengan menghitung rata-rata indikator pergerakan terarah dalam periode tertentu. Ketika nilai ADX di bawah ambang batas yang ditetapkan, dianggap pasar sedang dalam fase konsolidasi, dan pada saat itu dilakukan penentuan rentang kotak. Jika harga menembus batas atas atau bawah kotak, sinyal perdagangan dihasilkan.

Secara spesifik, strategi pertama-tama menghitung nilai ADX periode 14, dan jika di bawah 18 dianggap tren lemah. Kemudian, dihitung rentang kotak yang terbentuk dari harga tertinggi dan terendah 20 lilin terakhir. Ketika harga menembus kotak tersebut, dihasilkan sinyal beli dan jual. Jarak stop loss adalah 50% dari ukuran kotak, sedangkan jarak take profit adalah 100% dari ukuran kotak.

Strategi ini menggabungkan penilaian kekuatan tren dan sinyal penembusan, sehingga dapat menangkap pergerakan saat tren lemah dan memasuki fase konsolidasi, menghindari seringnya transaksi di pasar yang tidak beraturan. Saat tren kuat muncul, rentang take profit yang lebih besar memungkinkan perolehan keuntungan yang lebih banyak.

Keunggulan Strategi

- Menggabungkan penilaian kekuatan tren, sehingga dapat menghindari seringnya transaksi di pasar yang tidak beraturan.

- Penembusan kotak menambahkan penyaringan, sehingga menghindari jebakan di pasar yang bergerak sideways.

- Dalam tren yang kuat, memberikan ruang take profit yang lebih besar.

- Parameter ADX, parameter kotak, koefisien stop loss/take profit dapat disesuaikan, sehingga cocok untuk berbagai instrumen.

Risiko Strategi

- Pengaturan parameter ADX yang tidak tepat dapat menyebabkan kehilangan tren atau kesalahan penilaian.

- Ukuran kotak yang terlalu besar atau terlalu kecil dapat mempengaruhi hasil.

- Koefisien stop loss/take profit yang tidak tepat dapat menyebabkan stop loss terlalu kecil atau take profit terlalu dini.

Dapat dioptimalkan dengan menyesuaikan parameter ADX, parameter kotak, koefisien stop loss/take profit, agar lebih cocok untuk berbagai instrumen dan kondisi pasar. Manajemen modal yang ketat juga penting, dengan mengontrol persentase kerugian per transaksi untuk menghindari kerugian besar tunggal.

Arah Optimasi Strategi

- Parameter ADX dapat diuji dengan berbagai periode.

- Parameter kotak dapat diuji dengan berbagai panjang untuk menentukan ukuran rentang terbaik.

- Koefisien stop loss/take profit dapat disesuaikan untuk mengoptimalkan rasio risiko-keuntungan.

- Dapat diuji efek perdagangan satu arah, hanya long atau hanya short.

- Dapat ditambahkan indikator lain seperti indikator volume untuk kombinasi.

Kesimpulan

Secara keseluruhan, strategi ADX Smart Trend Following adalah strategi tren yang cukup stabil. Strategi ini menggabungkan penilaian kekuatan tren dan sinyal penembusan harga, sehingga sampai batas tertentu menghindari masalah membeli di puncak dan menjual di dasar yang sering terjadi pada strategi trend following biasa. Dengan optimasi parameter dan manajemen modal yang ketat, strategi ini dapat menghasilkan keuntungan secara stabil.

- 1