Strategi Pengikut Tren Berbasis kNN

Ikhtisar

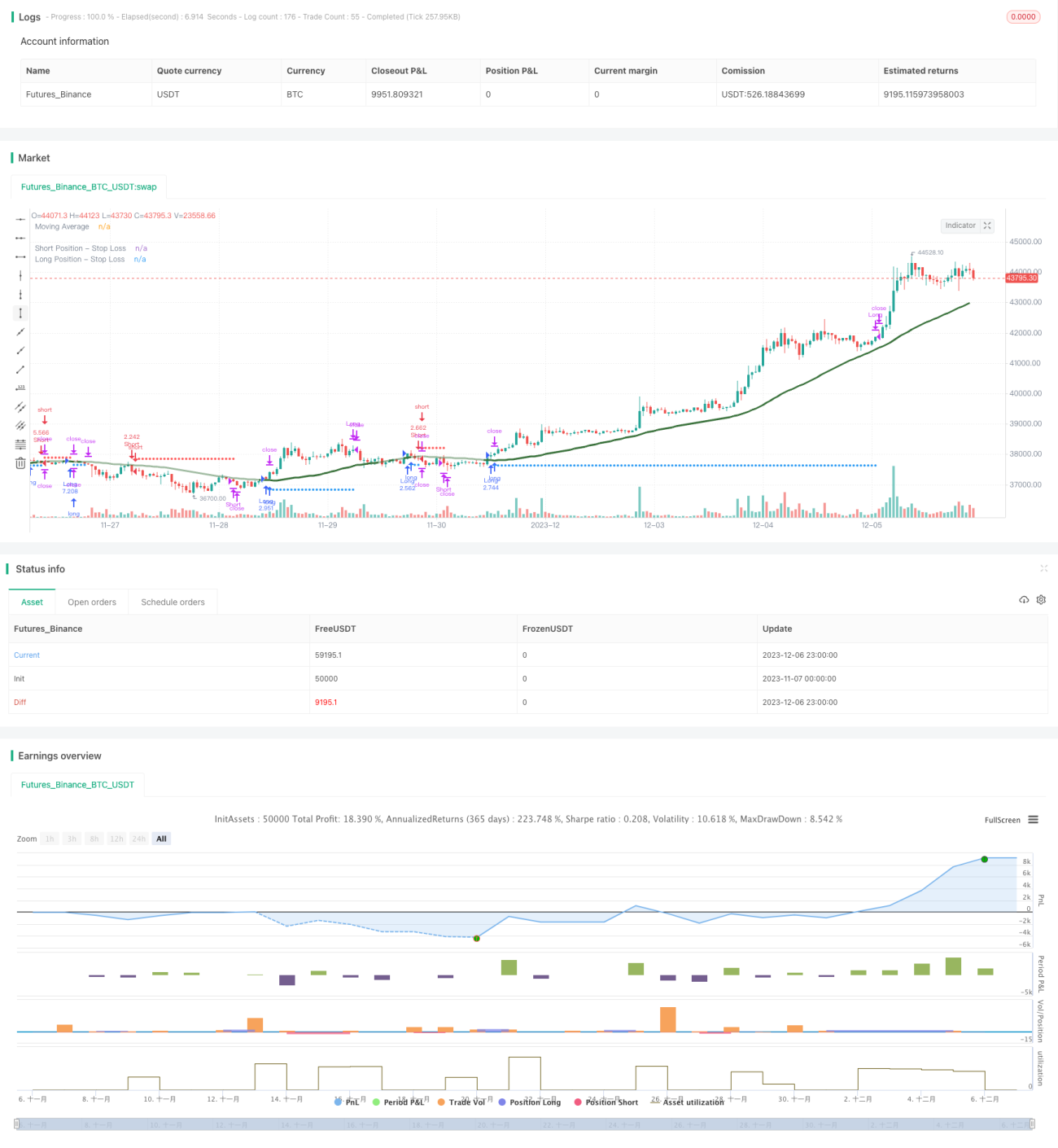

Strategi ini menggunakan algoritma pembelajaran mesin k-nearest neighbors (kNN) untuk memprediksi tren pasar, dan menghasilkan sinyal long dan short berdasarkan hasil prediksi. Strategi ini mempertimbangkan berbagai faktor seperti data historis, indikator teknis, dan lain-lain, dengan melatih model kNN untuk secara dinamis menangkap karakteristik pasar, sehingga mewujudkan perdagangan pengikut tren secara otomatis.

Prinsip Strategi

-

Mengumpulkan data pelatihan: mengumpulkan data deret waktu seperti harga penutupan historis, volume perdagangan, serta indikator teknis seperti RSI, CCI, dll.

-

Pra-pemrosesan data: menormalkan nilai indikator ke rentang 0-100.

-

Melatih model kNN: memasukkan dua fitur dalam model kNN saat ini, menghitung jarak Euclidean antara vektor fitur ini dengan vektor fitur historis, memilih k sampel historis terdekat, dan menghitung distribusi label (long atau short) dari k sampel tersebut.

-

Mendapatkan prediksi: memprediksi pergerakan pasar saat ini berdasarkan label dari k sampel tetangga terdekat. Jika prediksi adalah long, maka menghasilkan sinyal long; jika prediksi adalah short, maka menghasilkan sinyal short.

-

Melakukan perdagangan dengan menggabungkan filter seperti stop loss, kontrol posisi, moving average, dll.

Keunggulan Strategi

-

Menggunakan algoritma pembelajaran mesin untuk secara otomatis mengidentifikasi pola teknis, tanpa intervensi manual.

-

Dapat secara fleksibel memilih indikator teknis yang berbeda sebagai fitur model, mengoptimalkan strategi secara real-time.

-

Mengintegrasikan mekanisme kontrol risiko yang ketat seperti stop loss dan manajemen posisi.

-

Menampilkan garis stop loss secara visual, jelas dan intuitif.

Risiko dan Solusi

-

Prediksi pembelajaran mesin dapat menghasilkan false positive. Dapat memilih nilai k, vektor fitur, rentang waktu sampel, dll. yang sesuai untuk mengoptimalkan model.

-

Perdagangan satu arah memiliki potensi risiko. Dapat menambahkan izin perdagangan dua arah dalam kode untuk menghilangkan bug.

-

Pengaturan parameter yang tidak tepat dapat menyebabkan overtrading. Ukuran posisi, frekuensi perdagangan, dan parameter lainnya harus disesuaikan dengan tepat.

Arah Optimasi

-

Menguji berbagai jenis indikator teknis sebagai fitur masukan kNN.

-

Mencoba metode pengukuran jarak lainnya, seperti jarak Manhattan.

-

Menggunakan jarak sampel atau kualitas klasifikasi untuk menyesuaikan ukuran posisi.

-

Menambahkan pembagian set pelatihan dan set pengujian model, untuk mewujudkan optimasi bergulir.

Kesimpulan

Strategi ini menggunakan algoritma kNN klasik untuk memprediksi tren pasar, dan melakukan perdagangan mengikuti tren berdasarkan sinyal prediksi. Strategi ini memiliki karakteristik parameter yang dapat disesuaikan dan risiko yang terkendali, sehingga dapat menyediakan solusi perdagangan otomatis yang efektif bagi pengguna. Pengguna dapat terus meningkatkan kinerja strategi dengan menyesuaikan kombinasi indikator teknis, mengoptimalkan hyperparameter model, dan lain sebagainya.

- 1