Strategi Penyaringan Analisis Koreksi Indeks

Ikhtisar

Strategi ini menggunakan kombinasi operasi modulo dan moving average eksponensial untuk menghasilkan filter tren acak yang kuat, guna menentukan arah posisi. Strategi pertama-tama menghitung sisa bagi harga dibagi dengan angka yang ditentukan; jika hasilnya 0, maka sinyal transaksi muncul. Jika sinyal ini berada di bawah exponential moving average (EMA), maka posisi short diambil; jika di atas EMA, maka posisi long diambil. Strategi ini menggabungkan keacakan operasi matematika dengan penilaian tren indikator teknis, menggunakan validasi silang antara indikator periode yang berbeda untuk secara efektif menyaring sebagian pergerakan harga yang acak.

Prinsip Strategi

- Menetapkan nilai input harga a sebagai harga penutupan close (dapat diubah); menetapkan nilai pembagi b sebagai 4 (dapat diubah).

- Menghitung sisa bagi modulo = a % b, dan memeriksa apakah sisa bagi sama dengan 0.

- Menetapkan panjang EMA sebagai MALen, default 70 periode, sebagai indikator tren jangka menengah-panjang harga.

- Ketika sisa bagi modulo = 0, dihasilkan sinyal transaksi evennumber, dan hubungannya dengan EMA menentukan arah. Ketika harga menembus EMA ke atas, sinyal beli BUY dihasilkan; ketika harga menembus EMA ke bawah, sinyal jual SELL dihasilkan.

- Entry transaksi masuk ke posisi long atau short sesuai arah sinyal. Strategi dapat membatasi pembukaan posisi terbalik untuk mengontrol jumlah transaksi.

- Kondisi stop loss diatur berdasarkan tiga jenis: stop loss tetap, stop loss ATR, dan stop loss berdasarkan rentang fluktuasi harga. Kondisi take profit adalah kebalikan dari stop loss.

- Dapat memilih apakah akan menggunakan trailing stop untuk mengunci lebih banyak keuntungan, default tidak digunakan.

Analisis Keunggulan

- Keacakan operasi modulo menghindari pengaruh fluktuasi harga, dan dikombinasikan dengan penilaian tren moving average, secara efektif dapat menyaring sinyal yang tidak valid.

- Exponential Moving Average sebagai indikator tren jangka menengah-panjang, digabungkan dengan sinyal jangka pendek dari operasi modulo, menghasilkan validasi multi-lapis untuk menghindari sinyal palsu.

- Parameter yang dapat disesuaikan sangat fleksibel, memungkinkan penyesuaian parameter sesuai pasar yang berbeda untuk menemukan kombinasi parameter terbaik.

- Mengintegrasikan berbagai metode stop loss untuk mengelola risiko. Juga menetapkan kondisi take profit untuk mengunci keuntungan.

- Mendukung pembukaan posisi terbalik secara langsung, memungkinkan peralihan arah posisi yang mulus. Fitur ini juga dapat dinonaktifkan untuk mengurangi jumlah transaksi.

Analisis Risiko

- Pengaturan parameter yang tidak tepat dapat menghasilkan terlalu banyak sinyal transaksi, meningkatkan frekuensi transaksi dan biaya slippage.

- Exponential Moving Average sebagai satu-satunya indikator tren dapat menyebabkan lag, sehingga melewatkan momen pembalikan harga.

- Metode stop loss tetap mungkin terlalu mekanis dan tidak dapat menyesuaikan dengan volatilitas pasar.

- Pembukaan posisi terbalik secara langsung meningkatkan frekuensi penyesuaian posisi, sehingga meningkatkan biaya transaksi dan risiko.

Arah Optimasi

- Dapat menguji indikator moving average lain sebagai pengganti EMA, atau menggabungkan EMA dengan moving average lainnya, untuk melihat apakah dapat meningkatkan profitabilitas.

- Dapat mencoba menggabungkan filter modulo dengan strategi lain, seperti Bollinger Bands, pola candlestick, dll., untuk membentuk filter yang lebih stabil.

- Dapat meneliti metode stop loss adaptif yang menyesuaikan jarak stop loss sesuai dengan tingkat volatilitas pasar.

- Dapat menetapkan jumlah transaksi atau ambang laba/rugi untuk membatasi frekuensi pembukaan posisi terbalik secara langsung.

Kesimpulan

Strategi ini menggabungkan filter acak dari operasi modulo dengan penilaian tren moving average secara efektif. Parameter yang fleksibel memungkinkan penyesuaian dan optimasi sesuai lingkungan pasar yang berbeda, sehingga menghasilkan sinyal transaksi yang lebih andal. Selain itu, strategi ini mengintegrasikan berbagai mekanisme stop loss untuk mengelola risiko, serta take profit dan trailing stop untuk mengunci keuntungan. Secara keseluruhan, strategi ini memiliki logika yang jelas, mudah dipahami dan dimodifikasi, layak untuk diuji dan dioptimalkan lebih lanjut, serta memiliki potensi aplikasi perdagangan nyata yang besar.

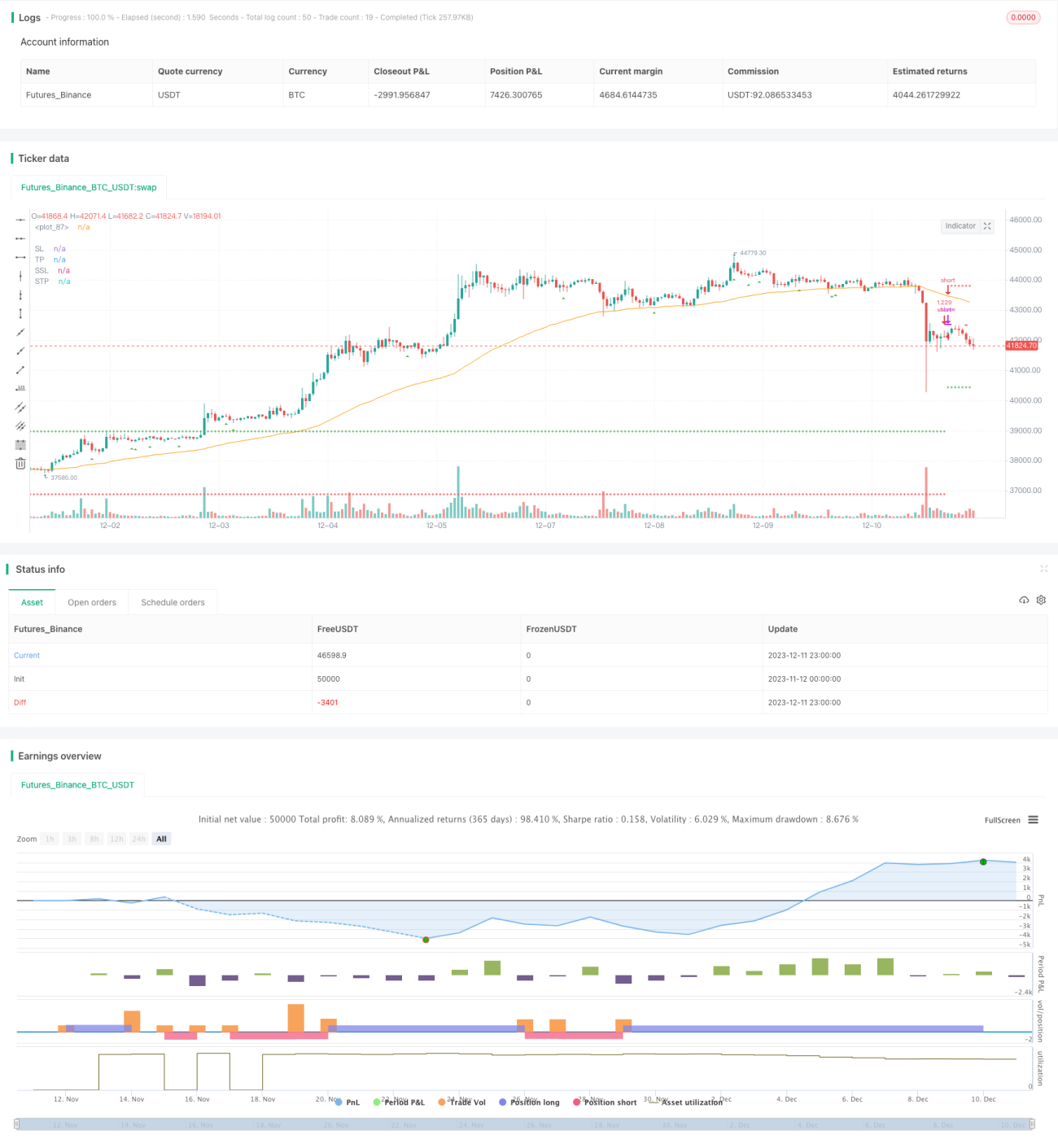

/*backtest

start: 2023-11-12 00:00:00

end: 2023-12-12 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © tweakerID

// To understand this strategy first we need to look into the Modulo (%) operator. The modulo returns the remainder numerator - 1