Strategi Breakout Dua Pita Bollinger

Ringkasan

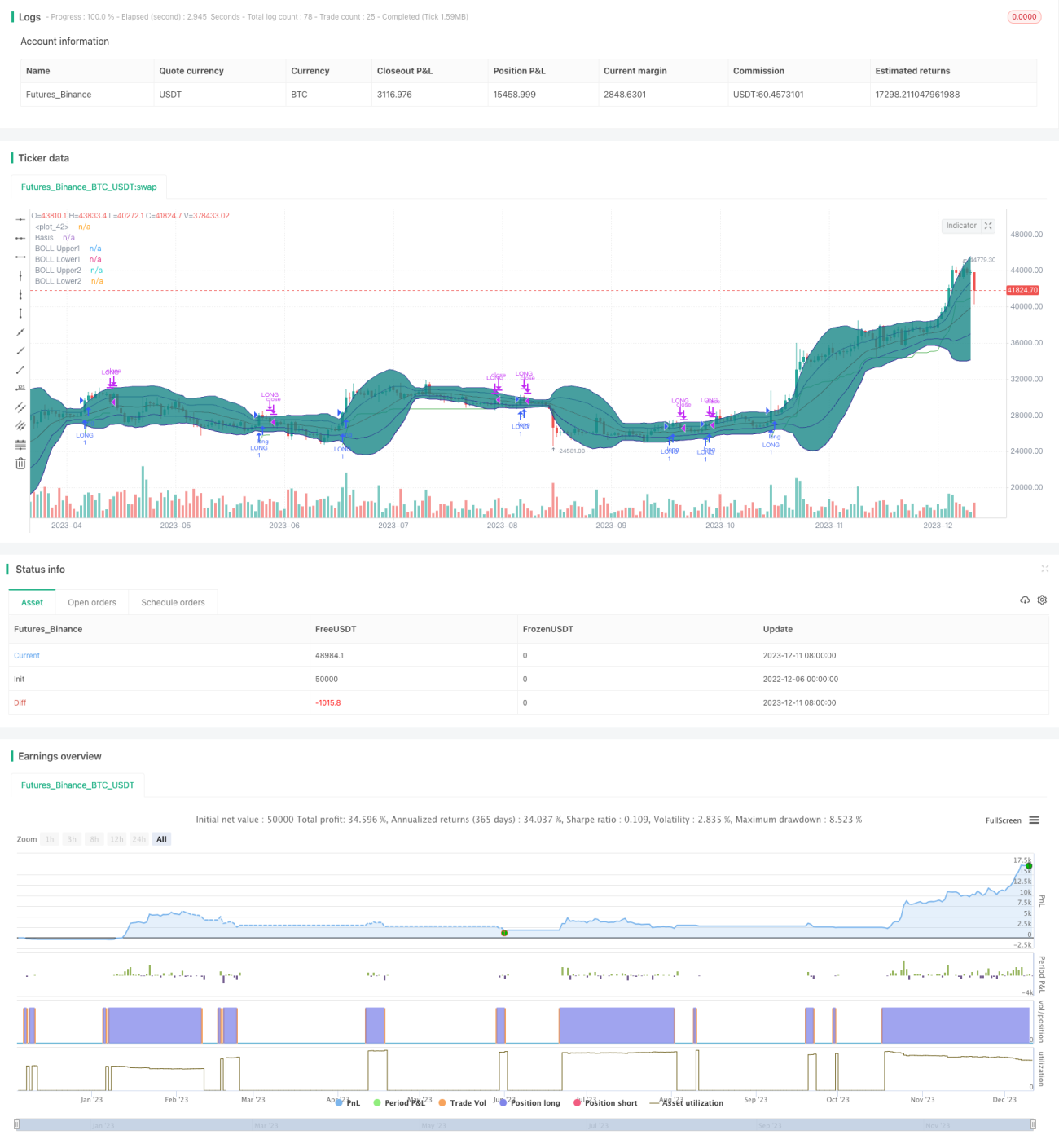

Strategi ini menggunakan indikator dual Bollinger Bands untuk mengidentifikasi area konsolidasi, dan menggabungkannya dengan strategi breakout guna menghasilkan strategi trading beli rendah jual tinggi. Ketika harga menembus zona netral, hal ini menandakan dimulainya tren baru, maka kita masuk posisi long. Ketika harga kembali turun menembus zona netral, hal ini menandakan berakhirnya tren, maka kita tutup posisi.

Prinsip Strategi

Strategi ini menggunakan dua Bollinger Bands. Pita dalam memiliki upper dan lower band berdasarkan SMA 20 hari ± 1 deviasi standar; pita luar memiliki upper dan lower band berdasarkan SMA 20 hari ± 2 deviasi standar. Ketika harga berada di antara pita dalam dan pita luar, area tersebut didefinisikan sebagai zona netral.

Ketika harga berada di zona netral selama dua candlestick berturut-turut, dianggap sedang dalam konsolidasi. Setelah dua candlestick konsolidasi, jika harga penutupan candlestick ketiga melampaui upper band pita dalam, maka dihasilkan sinyal long.

Setelah masuk posisi long, atur stop loss di harga terendah dikurangi 2 kali ATR, untuk mengunci keuntungan dan mengendalikan risiko. Ketika harga turun di bawah upper band pita dalam, tutup posisi.

Analisis Keunggulan

Strategi ini menggabungkan faktor indikator dan tren, mampu mengidentifikasi area konsolidasi dan menilai apakah harga memulai tren baru, sehingga memungkinkan beli rendah jual tinggi dengan potensi keuntungan besar. Strategi stop loss dapat mengunci keuntungan dan mengendalikan risiko, membuat strategi ini relatif stabil.

Analisis Risiko

Strategi ini bergantung pada sinyal long yang dihasilkan dari penembusan harga di atas upper band Bollinger Bands. Jika terjadi false breakout, maka akan menghasilkan order yang salah dan kerugian. Selain itu, jika titik stop loss terlalu dekat, dapat terkena stop loss secara instan.

Probabilitas false breakout dapat dikurangi dengan mengoptimalkan parameter Bollinger Bands, menambahkan filter kondisi seperti volume, dan lain-lain. Selain itu, titik stop loss dapat dilonggarkan secara wajar untuk memastikan ada ruang yang cukup.

Arah Optimasi

- Optimalkan parameter Bollinger Bands, sesuaikan lebar pita untuk mengurangi probabilitas false breakout.

- Tambahkan filter indikator lain, seperti volume perdagangan, untuk menghindari false breakout dengan volume rendah.

- Sesuaikan strategi stop loss untuk mencegah terjebak dan terkena stop loss instan.

- Tambahkan strategi masuk posisi secara bertahap untuk mengurangi risiko per transaksi.

Kesimpulan

Strategi ini mengintegrasikan indikator dual Bollinger Bands dan strategi tren, menghasilkan beli rendah jual tinggi dengan potensi keuntungan besar. Pada saat yang sama, strategi stop loss juga membuat strategi ini relatif stabil. Dengan optimasi lebih lanjut, efektivitas strategi dapat ditingkatkan, dan layak untuk diuji coba langsung di pasar nyata.

- 1