Strategi Trading Pembalikan Momentum TD

Gambaran Umum

Strategi Perdagangan Pembalikan Momentum TD adalah strategi perdagangan kuantitatif yang menggunakan indikator TD Sequential untuk mengidentifikasi sinyal pembalikan harga. Strategi ini didasarkan pada analisis momentum harga, dan mengambil posisi beli atau jual setelah mengonfirmasi sinyal pembalikan harga.

Prinsip Strategi

Strategi ini menggunakan indikator TD Sequential untuk menganalisis fluktuasi harga dan mengidentifikasi pola pembalikan harga dari 9 lilin (candlestick) berurutan. Secara spesifik, ketika pola kenaikan harga selama 9 lilin berurutan diikuti oleh lilin penurunan, strategi menilai sebagai peluang jual. Sebaliknya, ketika pola penurunan harga selama 9 lilin berurutan diikuti oleh lilin kenaikan, strategi menilai sebagai peluang beli.

Keunggulan memanfaatkan indikator TD Sequential adalah dapat menangkap sinyal pembalikan harga lebih awal. Dengan mekanisme pengejaran kenaikan dan penjualan (追涨杀跌) dalam jumlah tertentu yang digabungkan dalam strategi ini, posisi beli atau jual dapat dibuka tepat waktu setelah sinyal pembalikan dikonfirmasi, sehingga memperoleh peluang masuk yang lebih baik pada tahap awal pembalikan harga.

Analisis Keunggulan

- Menggunakan indikator TD Sequential dapat mengidentifikasi peluang pembalikan harga lebih awal.

- Mekanisme pengejaran kenaikan dan penjualan memungkinkan konfirmasi pembalikan harga yang lebih tepat waktu.

- Membuka posisi pada tahap pembentukan pembalikan memberikan titik masuk yang lebih optimal.

Analisis Risiko

- Indikator TD Sequential dapat menghasilkan sinyal palsu (false breakout), sehingga perlu dikonfirmasi dengan faktor lain.

- Perlu mengontrol ukuran posisi dan durasi posisi secara tepat untuk mengurangi risiko.

Arah Optimasi

- Menggabungkan indikator lain untuk mengonfirmasi sinyal pembalikan guna menghindari risiko sinyal palsu.

- Menerapkan mekanisme stop-loss untuk mengendalikan kerugian per transaksi.

- Mengoptimalkan ukuran posisi dan waktu penahanan posisi untuk menyeimbangkan keuntungan dan pengendalian risiko.

Kesimpulan

Strategi Perdagangan Pembalikan Momentum TD mengidentifikasi pembalikan harga lebih awal melalui indikator TD Sequential dan membuka posisi dengan cepat setelah konfirmasi pembalikan. Ini adalah strategi yang sangat cocok untuk pedagang momentum. Strategi ini memiliki keunggulan dalam mengidentifikasi peluang pembalikan, namun perlu diperhatikan pengendalian risiko untuk menghindari kerugian besar akibat sinyal palsu. Dengan optimasi lebih lanjut, strategi ini merupakan strategi perdagangan dengan rasio risiko-imbal hasil yang seimbang.

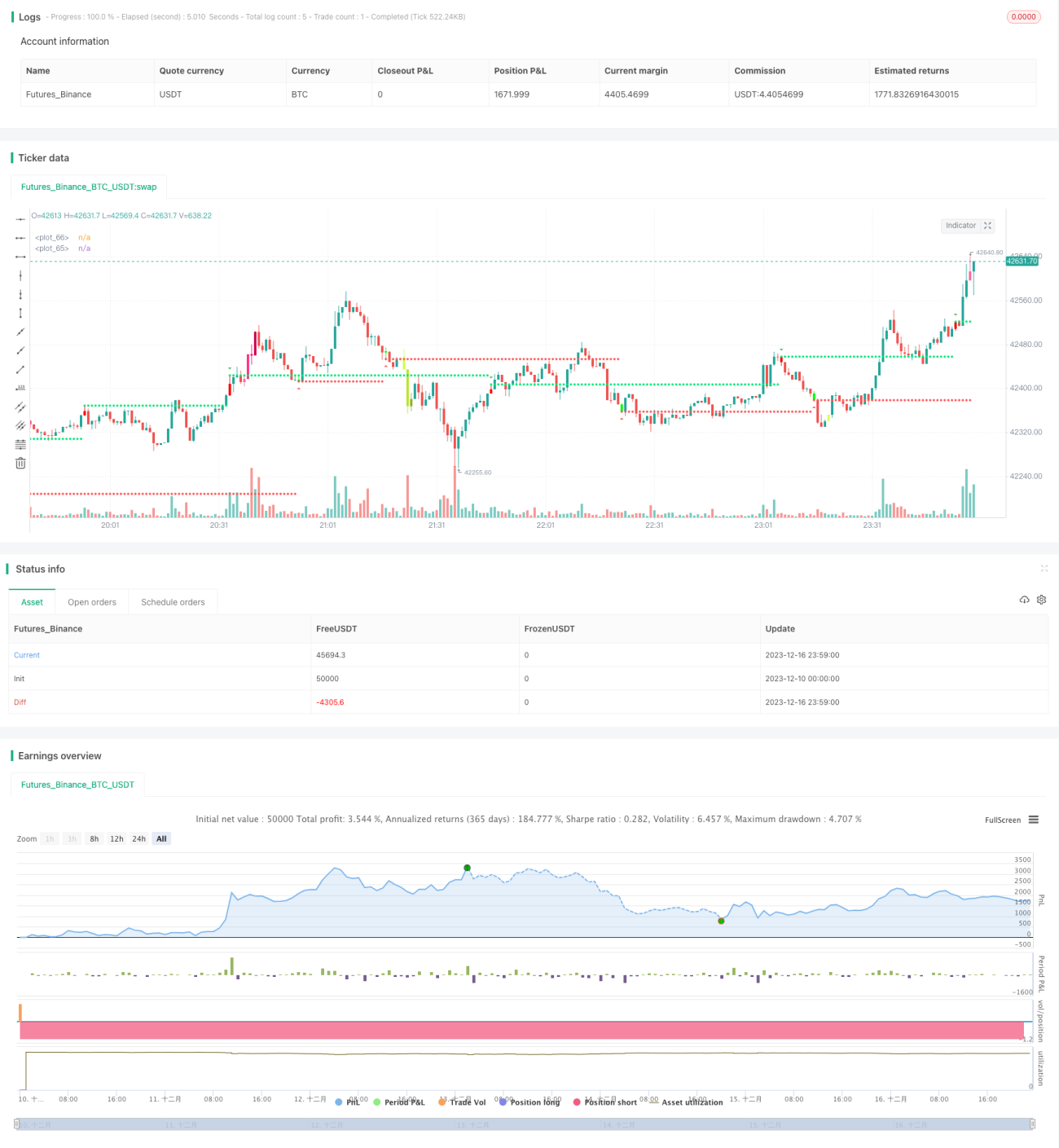

/*backtest

start: 2023-12-10 00:00:00

end: 2023-12-17 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//This strategy is based on TD sequential study from glaz.

//I made some improvement and modification to comply with pine script version 4.

//Basically, it is a strategy based on proce action, supports and resistance.- 1