Strategi Perdagangan Kuantitatif Indikator Ganda Hibrida

Ikhtisar

Strategi ini mengidentifikasi arah tren dan melakukan transaksi dengan menggabungkan dua indikator. Pertama, menggunakan persilangan dua moving average (garis cepat dan garis sedang) untuk menilai tren jangka pendek; kedua, menggunakan rentang saluran dan moving average jangka panjang untuk menentukan arah tren utama. Hanya ketika kedua hasil penilaian konsisten, sinyal transaksi akan dihasilkan. Strategi campuran yang menggunakan beberapa indikator ini dapat secara efektif menyaring sinyal palsu dan meningkatkan stabilitas.

Prinsip Strategi

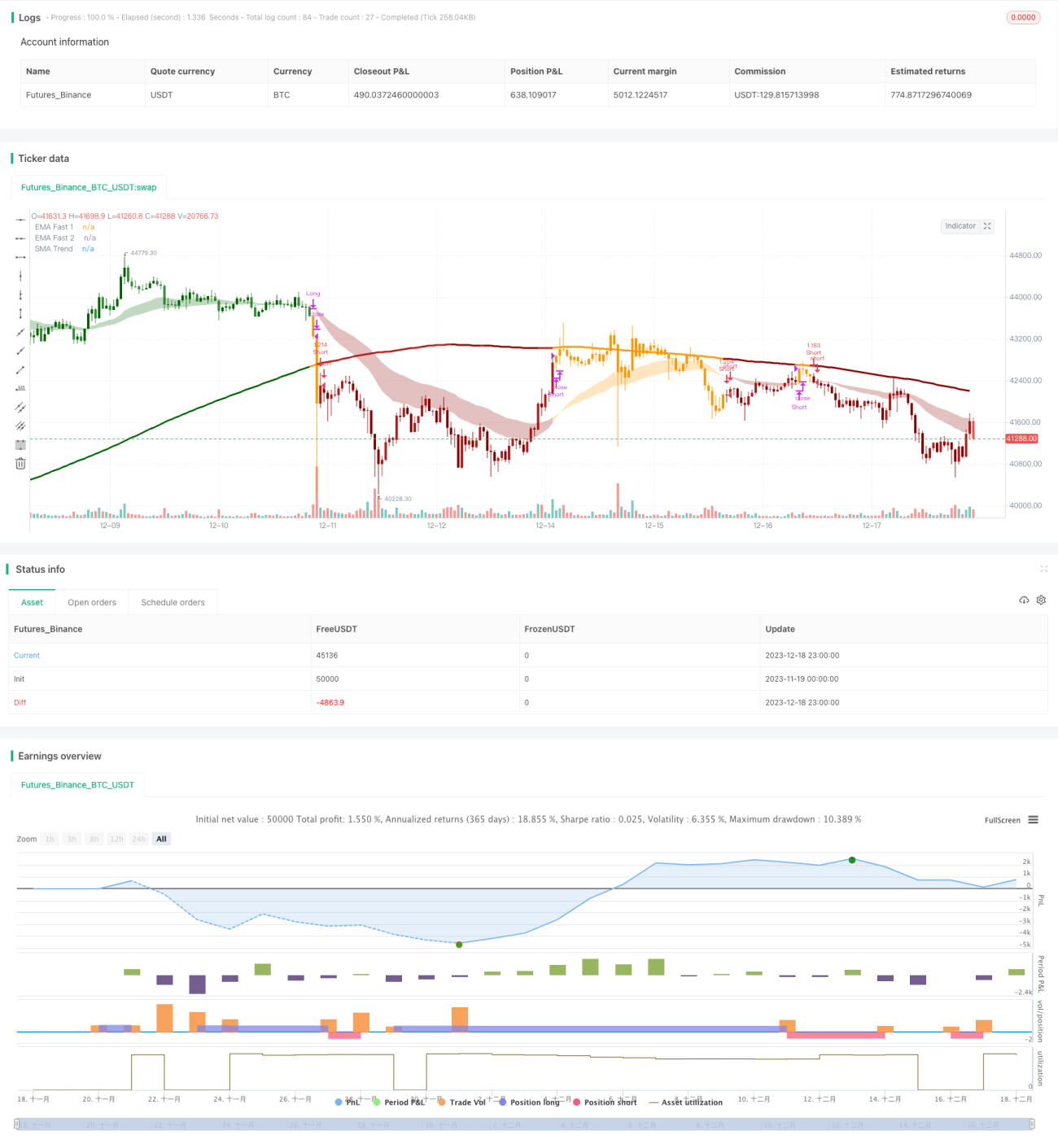

Strategi ini menggunakan tiga kelompok indikator untuk penilaian. Pertama, persilangan emas dan mati antara EMA cepat (periode 26) dan EMA sedang (periode 50) untuk menilai tren jangka pendek; kedua, menghitung rentang saluran, menentukan apakah harga menembus rentang tersebut untuk menilai arah bullish/bearish tren jangka menengah; terakhir, menghitung SMA jangka panjang (periode 200), membandingkannya dengan harga untuk menentukan arah tren utama. Hanya ketika ketiga hasil penilaian semuanya konsisten, sinyal transaksi akan dikeluarkan.

Secara spesifik, logika penilaian adalah:

-

Persilangan antara garis cepat dan garis sedang (golden cross = bullish, death cross = bearish) untuk menentukan arah tren jangka pendek.

-

Apakah harga menembus rentang saluran untuk menentukan arah tren jangka menengah. Rentang saluran didasarkan pada moving average jangka panjang ditambah atau dikurangi ATR dikalikan dengan koefisien. Jika harga menembus batas atas, itu bullish; jika menembus batas bawah, itu bearish.

-

Membandingkan hubungan besar-kecil antara harga dan moving average jangka panjang untuk menentukan arah tren utama.

Akhirnya, sinyal transaksi hanya akan dikeluarkan ketika ketiga penilaian (jangka pendek, menengah, panjang) semuanya konsisten. Penilaian campuran ini secara efektif dapat menyaring sinyal palsu dan meningkatkan stabilitas.

Keunggulan Strategi

Strategi campuran indikator ganda ini memiliki beberapa keunggulan:

-

Secara efektif menyaring sinyal palsu, meningkatkan stabilitas. Karena sinyal transaksi memerlukan verifikasi dari berbagai indikator jangka pendek, menengah, dan panjang, sehingga menghindari sinyal salah yang disebabkan oleh indikator tunggal.

-

Fleksibilitas tinggi, parameter indikator dapat disesuaikan dengan pasar. Parameter moving average cepat dan lambat serta rentang saluran dapat diubah, cocok untuk berbagai kondisi pasar.

-

Menggabungkan strategi trend trading dan range trading. Indikator jangka pendek dan menengah menangkap tren, indikator jangka panjang menentukan rentang, secara keseluruhan memiliki keunggulan dari strategi trend dan reversal.

-

Efisiensi penggunaan modal tinggi. Hanya melakukan order ketika hasil dari beberapa indikator konsisten, sehingga dapat menggunakan modal secara efektif dan menghindari transaksi yang tidak perlu.

Risiko Strategi

Strategi ini juga memiliki beberapa risiko:

-

Risiko pengaturan parameter. Periode moving average dan parameter rentang saluran perlu diatur secara wajar; jika tidak tepat, mungkin tidak dapat mendeteksi tren secara efektif atau menyebabkan terlalu banyak sinyal salah.

-

Indikator ganda meningkatkan biaya peluang transaksi. Dibandingkan dengan strategi indikator tunggal, mungkin melewatkan sebagian peluang transaksi, tidak dapat masuk dan keluar di titik terbaik.

-

Strategi stop-loss perlu hati-hati. Mekanisme stop-loss breakout dalam strategi ini dapat menyebabkan kerugian yang tidak perlu, persentase stop-loss perlu diatur dengan hati-hati.

-

Efektivitas mungkin kurang baik di pasar yang sangat bergejolak. Strategi ini lebih cocok untuk lingkungan pasar dengan tren yang jelas.

Arah Optimasi Strategi

Strategi ini dapat dioptimalkan dari beberapa aspek berikut:

-

Menguji berbagai kombinasi parameter untuk menemukan parameter terbaik. Dapat menggunakan lebih banyak data historis untuk pengujian guna menemukan pengaturan parameter optimal.

-

Menambahkan mekanisme stop-loss adaptif. Dapat dikombinasikan dengan Indikator Volatilitas untuk menyesuaikan besaran stop-loss secara dinamis.

-

Menambahkan indikator volume untuk membantu penilaian. Membantu menentukan ukuran posisi pada titik-titik kunci, meningkatkan efisiensi penggunaan modal.

-

Mengoptimalkan logika entry. Mempertimbangkan strategi cost averaging dengan entry bertahap untuk mengurangi risiko entry tunggal.

-

Menggabungkan model machine learning untuk penilaian. Memperkenalkan model seperti neural network untuk menilai ketahanan model dan goodness-of-fit.

Kesimpulan

Strategi ini menggunakan tiga indikator (cepat, sedang, panjang) dan mekanisme verifikasi ganda, secara efektif dapat menekan sinyal palsu dan meningkatkan stabilitas. Pada saat yang sama, memiliki keunggulan dari trend trading dan range trading, efisiensi penggunaan modal tinggi. Dapat ditingkatkan melalui optimasi parameter, optimasi stop-loss, kombinasi indikator volume, dan berbagai cara lainnya. Ini adalah strategi kuantitatif campuran yang direkomendasikan.

- 1