Strategi Robot Skalabel Kustom HTF MACD MFI Non-Repaint

Ikhtisar

Strategi ini adalah strategi kombinasi indikator MACD dan MFI yang tidak menggambar ulang (non-repainting) dan sangat dapat disesuaikan, cocok untuk robot trading algoritmik. Ini menggabungkan indikator tren dan indikator momentum, menghasilkan sinyal trading melalui berbagai filter.

Prinsip Strategi

Strategi ini menggunakan indikator MACD untuk menentukan arah tren pasar. MACD adalah indikator momentum tipe yang mengikuti tren, diperoleh dengan mengurangi rata-rata bergerak cepat dengan rata-rata bergerak lambat untuk mendapatkan histogram MACD, kemudian menggunakan rata-rata bergerak eksponensial dari MACD untuk mendapatkan garis sinyal. Ketika garis cepat menembus ke atas garis lambat, itu adalah sinyal beli; ketika menembus ke bawah, itu adalah sinyal jual.

Selain itu, strategi ini juga menggunakan indikator MFI untuk menentukan kondisi overbought dan oversold pasar. Indikator MFI menggabungkan informasi harga dan volume, dengan nilai berfluktuasi antara 0 hingga 100. MFI di bawah 20 adalah zona oversold, di atas 80 adalah zona overbought.

Untuk menyaring sinyal palsu, strategi ini juga menambahkan filter tren dan filter RSI. Ketika harga berada dalam tren naik dan RSI kurang dari ambang batas yang ditentukan, sinyal beli dihasilkan.

Keunggulan Strategi

- Menggabungkan beberapa indikator, menilai kondisi pasar secara komprehensif, meningkatkan tingkat kemenangan

- Menambahkan mekanisme filter, menghindari sinyal palsu, mengurangi perdagangan yang tidak perlu

- Berbagai parameter dan filter dapat dikonfigurasi secara kustom, beradaptasi dengan berbagai instrumen dan preferensi trading

- Dapat digunakan untuk trading manual, juga dapat dihubungkan ke robot algoritmik untuk trading terprogram

Risiko dan Solusi Strategi

-

Pengaturan parameter indikator yang tidak tepat mudah menghasilkan sinyal palsu

-

Dapat menguji parameter yang berbeda, memilih kombinasi parameter optimal

-

Parameter tidak bersifat universal untuk berbagai instrumen, perlu diuji dan dioptimalkan secara terpisah

-

Frekuensi trading mungkin terlalu tinggi, meningkatkan biaya trading dan risiko slippage

-

Dapat menyesuaikan filter untuk mengurangi frekuensi trading

-

Saat trading live, perhatikan kontrol biaya

Arah Optimasi Strategi

- Menguji periode data yang lebih panjang, mengevaluasi stabilitas parameter

- Mencoba kombinasi parameter indikator yang berbeda

- Mengoptimalkan bobot indikator, meningkatkan stabilitas strategi

- Menambahkan lebih banyak filter untuk mengurangi perdagangan yang tidak perlu

Kesimpulan

Strategi ini adalah strategi tipe mengikuti tren yang sangat dapat disesuaikan, menggabungkan indikator tren dan momentum untuk menilai kondisi pasar, dan secara efektif memanfaatkan mekanisme filter untuk mengendalikan risiko. Ini dapat digunakan untuk trading manual, juga dapat dihubungkan ke robot algoritmik untuk mencapai trading terprogram dengan tingkat otomatisasi yang tinggi, merupakan sistem strategi yang layak untuk dipantau dan dioptimalkan dalam jangka panjang.

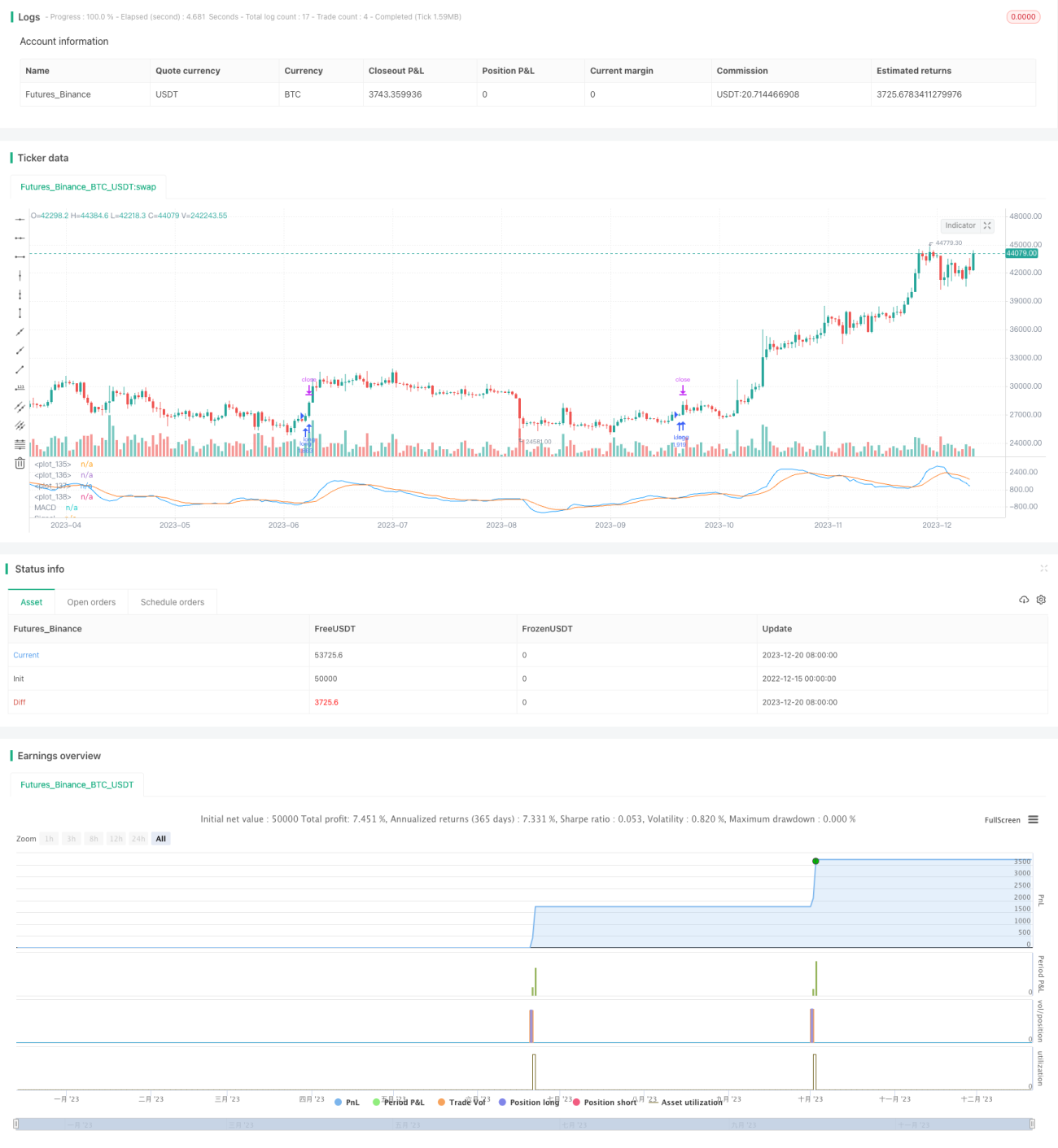

/*backtest

start: 2022-12-15 00:00:00

end: 2023-12-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//(c) Wunderbit Trading

//Modified by Mauricio Zuniga - Trade at your own risk

//This script was originally shared on Wunderbit website as a free open source script for the community. (https://help.wundertrading.com/en/articles/5246468-macd-mfi-trading-bot-for-ftx)

// - 1