Strategi Trading Bitcoin Berdasarkan Indikator Kuantitatif

Ikhtisar

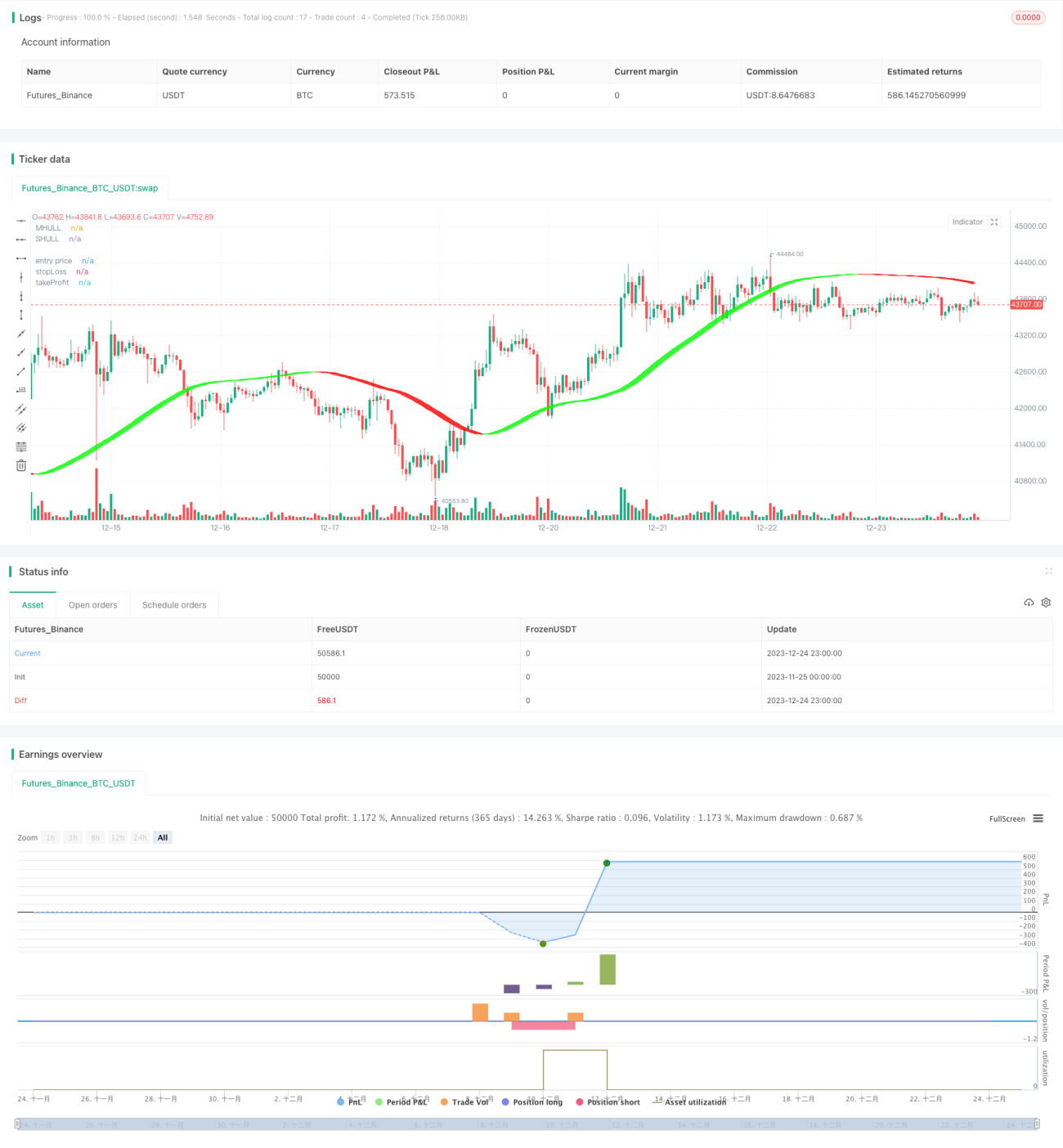

Strategi ini menggunakan berbagai indikator kuantitatif untuk menentukan waktu beli dan jual Bitcoin, sehingga memungkinkan perdagangan otomatis. Indikator utama meliputi Hull Moving Average (HMA), Relative Strength Index (RSI), Bollinger Bands (BB), dan Volume Oscillator (VO).

Prinsip Strategi

-

Menggunakan Hull Moving Average yang dimodifikasi untuk menentukan arah tren utama pasar, dikombinasikan dengan Bollinger Bands untuk membantu mengidentifikasi titik breakout beli/jual.

-

Indikator RSI dikombinasikan dengan rentang volatilitas adaptif untuk mendeteksi area overbought/oversold dan menghasilkan sinyal trading. Pada saat yang sama, dua set parameter disiapkan sebagai verifikasi sinyal Duplikat.

-

Volume Oscillator digunakan untuk menilai kekuatan beli/jual dan menghindari breakout palsu.

-

Berdasarkan rasio parameter stop loss/take profit, posisi stop loss dan take profit telah ditetapkan sebelumnya untuk manajemen risiko.

Analisis Keunggulan

-

Kurva Hull dapat menangkap perubahan tren lebih cepat, dan bantuan Bollinger Bands mengurangi sinyal palsu.

-

Parameter RSI yang dioptimalkan dan verifikasi sinyal Duplikat meningkatkan keandalan.

-

Volume Oscillator yang dikombinasikan dengan tren dan sinyal indikator menghindari perdagangan yang tidak akurat.

-

Metode stop loss/take profit yang ditetapkan sebelumnya dapat secara otomatis mengontrol kerugian per perdagangan, sehingga mengelola risiko keseluruhan secara efektif.

Analisis Risiko

-

Pengaturan parameter yang tidak tepat dapat menyebabkan frekuensi perdagangan terlalu tinggi atau efektivitas sinyal menurun.

-

Ketika peristiwa tak terduga menyebabkan volatilitas pasar yang ekstrem, stop loss dapat tertembus, mengakibatkan kerugian besar.

-

Ketika aset perdagangan diganti dengan koin lain, parameter perlu diuji ulang dan dioptimalkan.

-

Jika data volume hilang, Volume Oscillator tidak akan berfungsi.

Arah Optimasi

-

Melakukan lebih banyak pengujian kombinasi parameter RSI untuk menemukan parameter terbaik.

-

Mencoba indikator lain seperti MACD, KD, dan lainnya yang dikombinasikan dengan RSI untuk meningkatkan akurasi sinyal.

-

Menambahkan modul prediksi model, menggabungkan pembelajaran mesin untuk menentukan arah pasar.

-

Menguji efek parameter saat mengganti ke aset perdagangan lain.

-

Mengoptimalkan algoritma stop loss/take profit untuk memaksimalkan keuntungan.

Kesimpulan

Strategi ini secara komprehensif menggunakan berbagai indikator teknikal kuantitatif untuk menentukan waktu beli/jual. Melalui optimasi parameter, kontrol risiko, dan metode lainnya, perdagangan otomatis Bitcoin telah terwujud. Efeknya cukup baik, namun masih perlu pengujian dan optimasi berkelanjutan untuk beradaptasi dengan perubahan pasar. Dapat memberikan referensi bagi investor dan membantu pengambilan keputusan perdagangan.

- 1