Strategi Terobosan Fluktuasi Volume Transaksi Dinamis

Ikhtisar

Strategi ini menggunakan volume beli dan jual dalam jangka waktu kustom untuk menilai arah naik/turun, dikombinasikan dengan VWAP mingguan dan Bollinger Bands sebagai filter, untuk mencapai tren berikut dengan probabilitas tinggi. Selain itu, mekanisme take profit dan stop loss dinamis diterapkan untuk mengendalikan risiko sepihak secara efektif.

Prinsip Strategi

- Menghitung indikator volume beli dan jual dalam jangka waktu kustom

- BV: Volume beli, yang disebabkan oleh pembelian di titik terendah

- SV: Volume jual, yang disebabkan oleh penjualan di titik tertinggi

- Memproses volume beli dan jual

- Menghaluskan menggunakan EMA periode 20

- Memisahkan volume beli dan jual yang telah diproses menjadi positif dan negatif

- Menentukan arah indikator

- Indikator > 0 menunjukkan bullish, < 0 menunjukkan bearish

- Menggabungkan VWAP mingguan dan Bollinger Bands untuk mendeteksi divergensi

- Harga di atas VWAP dan indikator bullish = sinyal beli

- Harga di bawah VWAP dan indikator bearish = sinyal jual

- Take profit dan stop loss dinamis

- Mengatur persentase take profit dan stop loss berdasarkan ATR harian

Keunggulan Strategi

- Volume beli dan jual dapat mencerminkan momentum pasar yang sebenarnya, menangkap energi potensial dari tren

- VWAP mingguan menentukan arah tren jangka panjang, Bollinger Bands mendeteksi sinyal breakout

- ATR dinamis untuk take profit dan stop loss dapat mengunci keuntungan secara maksimal dan menghindari overshoot

Risiko Strategi

- Data volume beli dan jual memiliki beberapa kesalahan, yang dapat menyebabkan kesalahan penilaian

- Menggabungkan hanya satu indikator dapat menghasilkan sinyal palsu

- Pengaturan parameter Bollinger Bands yang tidak tepat dapat mempersempit breakout yang valid

Arah Optimasi Strategi

- Mengoptimalkan indikator volume beli dan jual dalam beberapa jangka waktu

- Menambahkan indikator pendukung seperti volume perdagangan untuk menyaring sinyal

- Menyesuaikan parameter Bollinger Bands secara dinamis untuk meningkatkan efisiensi breakout

Kesimpulan

Strategi ini memanfaatkan sepenuhnya daya prediksi volume beli dan jual, didukung oleh VWAP dan Bollinger Bands untuk menghasilkan sinyal probabilitas tinggi, serta mengendalikan risiko secara efektif melalui take profit dan stop loss dinamis. Ini adalah strategi trading kuantitatif yang efisien dan stabil. Dengan optimasi parameter dan aturan yang terus-menerus, hasil yang diharapkan akan semakin jelas.

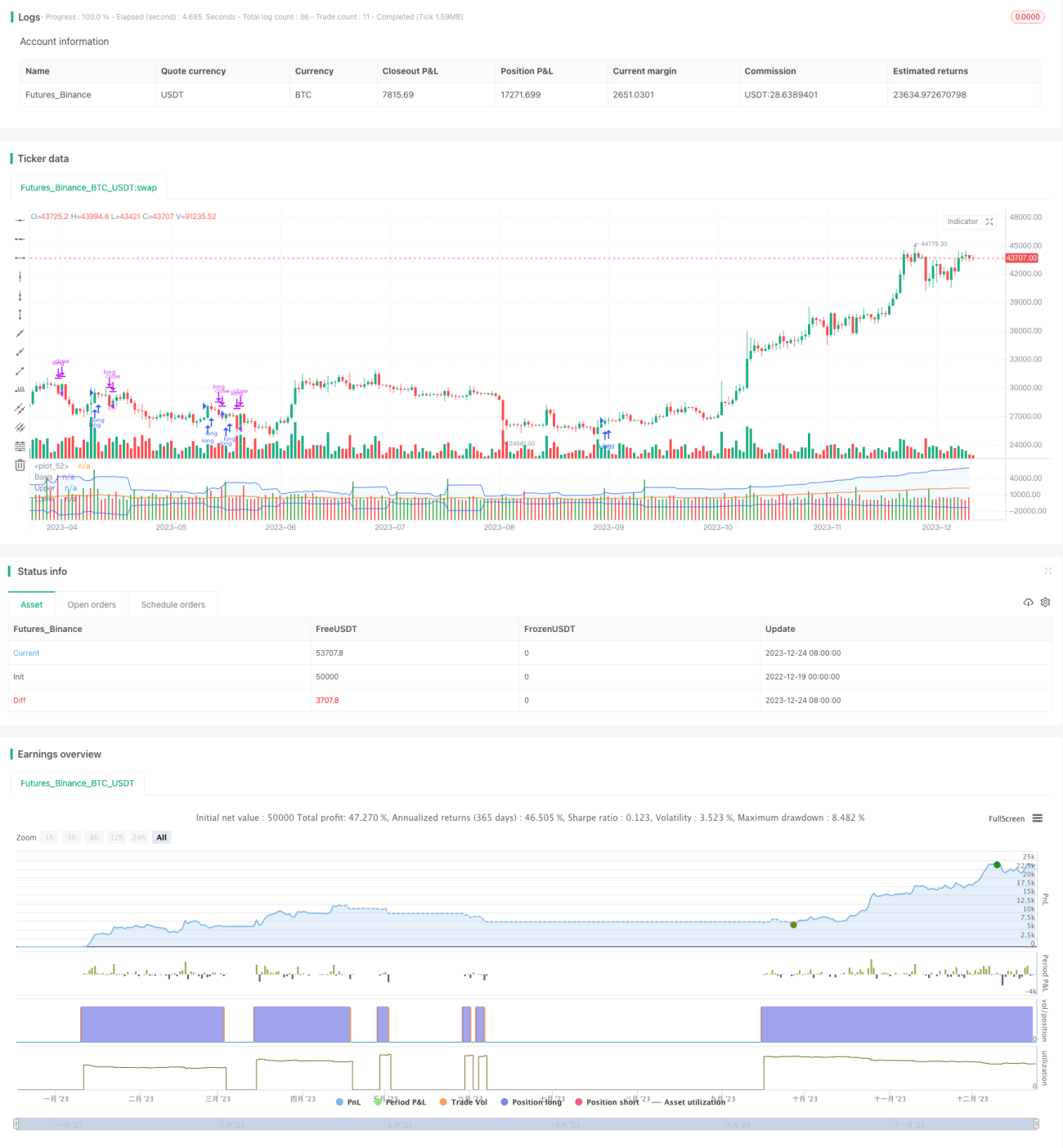

/*backtest

start: 2022-12-19 00:00:00

end: 2023-12-25 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © original author ceyhun

//@ exlux99 update

- 1