Strategi Trading Retracement RSI dengan Persilangan Bawah Bollinger Bands

Ikhtisar

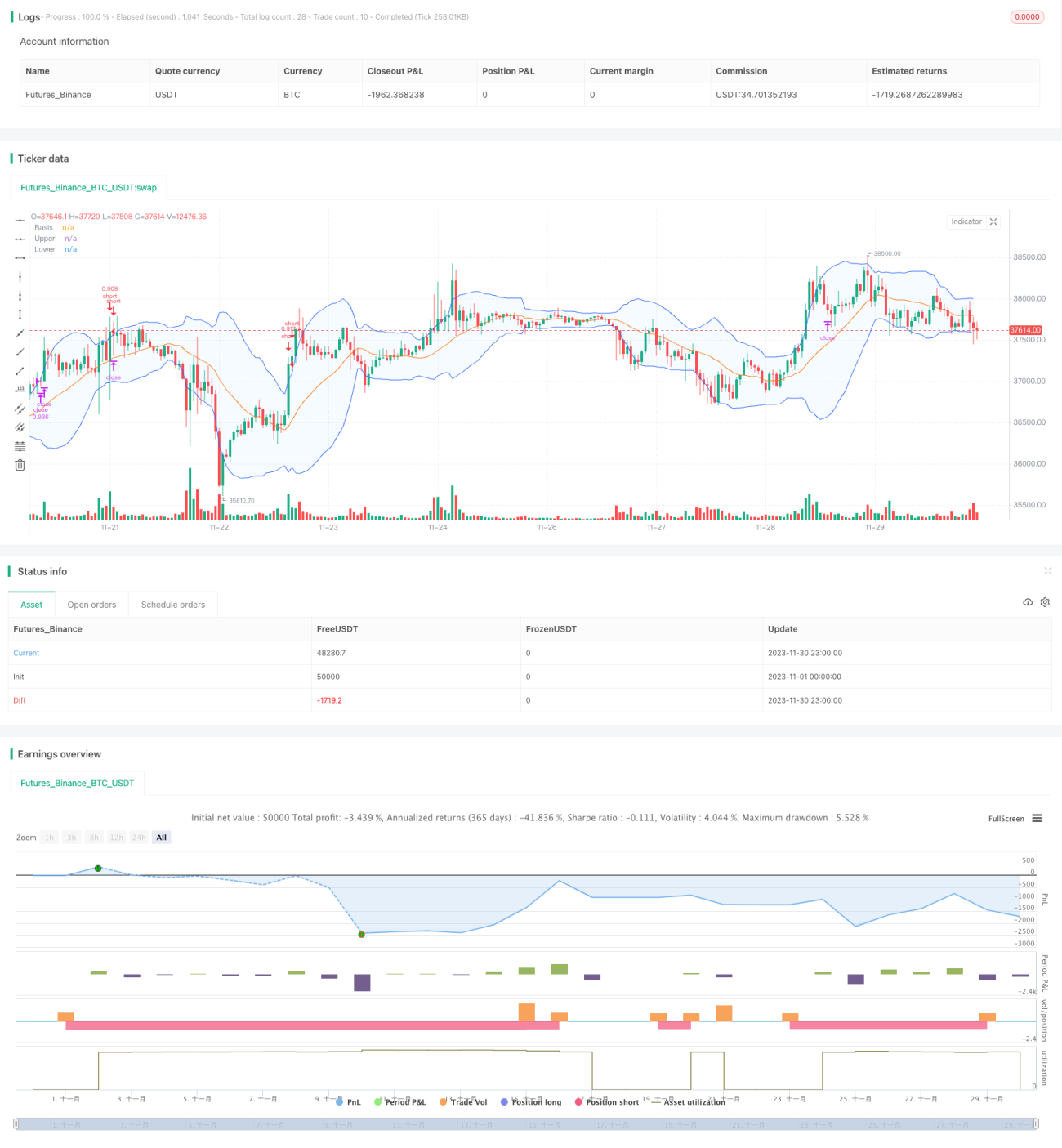

Strategi ini menggunakan indikator Bollinger Bands untuk menentukan apakah harga telah memasuki zona overbought atau oversold, dikombinasikan dengan indikator RSI untuk mengidentifikasi peluang koreksi. Ketika terjadi death cross di zona overbought, strategi akan membuka posisi short (jual). Stop loss diterapkan ketika harga naik melebihi upper band Bollinger Bands.

Prinsip Strategi

Strategi ini didasarkan pada prinsip-prinsip berikut:

- Ketika harga penutupan menembus ke atas upper band Bollinger Bands, ini menandakan aset memasuki zona overbought, sehingga terdapat peluang koreksi.

- Indikator RSI secara efektif dapat menentukan zona overbought dan oversold; RSI > 70 menandakan zona overbought.

- Ketika harga penutupan turun menembus upper band, posisi short (jual) dibuka.

- Ketika RSI turun dari zona overbought atau titik stop loss terpicu, posisi ditutup (stop loss).

Analisis Keunggulan

Strategi ini memiliki keunggulan sebagai berikut:

- Menggunakan Bollinger Bands untuk menentukan zona overbought/oversold, meningkatkan tingkat keberhasilan perdagangan.

- Menggabungkan indikator RSI untuk menyaring sinyal false breakout, menghindari kerugian yang tidak perlu.

- Rasio risk-reward yang tinggi, mengontrol risiko secara maksimal.

Analisis Risiko

Strategi ini memiliki risiko sebagai berikut:

- Harga terus naik setelah menembus upper band, menyebabkan kerugian semakin besar.

- RSI tidak segera turun, sehingga kerugian semakin besar.

- Posisi satu arah (hanya short), tidak dapat memperdagangkan pasar yang bergerak sideways (konsolidasi).

Risiko dapat dikurangi melalui metode berikut:

- Menyesuaikan titik stop loss secara tepat untuk menghentikan kerugian tepat waktu.

- Menggabungkan indikator lain untuk menentukan sinyal penurunan RSI.

- Menggabungkan indikator moving average untuk menentukan apakah pasar memasuki fase sideways.

Arah Optimasi

Strategi ini dapat dioptimalkan dari aspek-aspek berikut:

- Mengoptimalkan parameter Bollinger Bands agar sesuai dengan lebih banyak instrumen trading.

- Mengoptimalkan parameter RSI untuk meningkatkan efektivitas indikator.

- Menambahkan kombinasi indikator lain untuk menentukan titik pembalikan tren.

- Menambahkan logika perdagangan untuk posisi long (beli).

- Menggabungkan strategi stop loss untuk menyesuaikan titik stop loss secara dinamis.

Kesimpulan

Secara keseluruhan, strategi ini merupakan strategi perdagangan jangka pendek cepat yang khas di zona overbought. Menggunakan Bollinger Bands untuk menentukan titik entry/exit, dan RSI untuk menyaring sinyal. Dengan stop loss yang wajar, tingkat risiko dapat dikendalikan. Efektivitasnya dapat ditingkatkan melalui optimasi parameter, kombinasi indikator, dan penambahan logika pembukaan posisi.

- 1