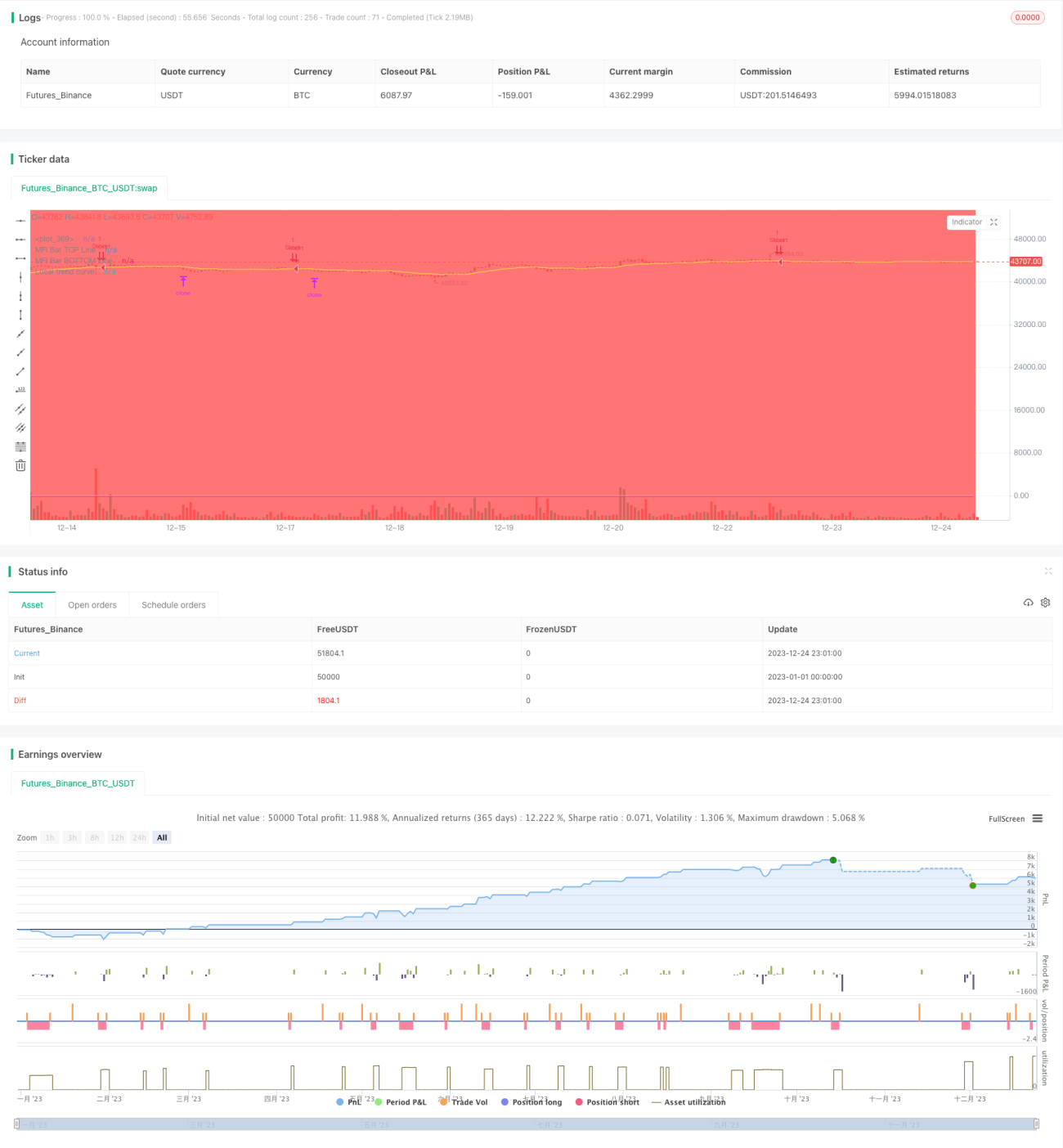

Strategi Perdagangan Kuantitatif Berdasarkan Filter Tren Ganda

Ringkasan

Strategi ini adalah strategi trading kuantitatif yang menggunakan filter tren ganda. Strategi ini menggabungkan filter tren global dan filter tren lokal, memastikan hanya membuka posisi ketika arah tren sesuai. Selain itu, strategi ini juga menetapkan beberapa kondisi filter tambahan, seperti filter RSI, filter harga, filter kemiringan, dll., untuk lebih meningkatkan keandalan sinyal trading. Dalam hal keluar posisi, strategi telah menetapkan level stop loss dan take profit. Secara keseluruhan, ini adalah strategi trading kuantitatif yang stabil dan akurat.

Prinsip Strategi

Logika inti dari strategi ini didasarkan pada filter tren ganda. Filter tren global menggunakan EMA periode tinggi untuk menilai tren keseluruhan pasar, sedangkan filter tren lokal menggunakan EMA periode rendah untuk menilai tren lokal. Posisi hanya dibuka ketika kedua filter menunjukkan arah tren yang sama.

Secara spesifik, strategi menghitung garis EMA BTCUSDT untuk menentukan apakah pasar secara keseluruhan berada dalam tren naik atau turun – ini adalah filter tren global. Pada saat yang sama, strategi menghitung garis EMA kontrak ini untuk menentukan tren pasar lokal – ini adalah filter tren lokal. Ketika kedua filter menunjukkan arah tren yang sama, dikombinasikan dengan beberapa filter bantu lainnya, strategi akan menghasilkan sinyal trading dan membuka posisi dengan harga take profit dan stop loss yang telah ditentukan.

Setelah sinyal trading ditentukan, strategi akan segera memasuki posisi. Pada saat yang sama, strategi telah menetapkan harga take profit dan stop loss. Ketika harga menyentuh level take profit atau stop loss, strategi akan secara otomatis menutup posisi dengan untung atau rugi.

Analisis Keunggulan

Ini adalah strategi trading kuantitatif yang stabil dan andal, dengan keunggulan utama sebagai berikut:

-

Menggunakan mekanisme filter tren ganda, mampu menyaring sebagian besar sinyal palsu, membuat sinyal trading lebih andal dan akurat.

-

Menggabungkan beberapa filter bantu, seperti filter RSI, filter harga, dll., untuk lebih meningkatkan kualitas sinyal.

-

Secara otomatis menghitung level take profit dan stop loss, tanpa perlu pemantauan manual, mengurangi risiko trading.

-

Parameter strategi dapat disesuaikan secara kustom untuk beradaptasi dengan lebih banyak instrumen trading, memiliki daya adaptasi yang kuat.

-

Logika strategi jelas dan mudah dipahami, memudahkan optimasi dan peningkatan, serta memiliki potensi pengembangan yang besar.

Analisis Risiko

Meskipun strategi ini memiliki banyak keunggulan, masih ada beberapa risiko trading yang perlu diperhatikan, terutama:

-

Filter tren ganda mungkin tidak akurat dalam menentukan waktu masuk posisi. Dapat dioptimalkan dengan menyesuaikan parameter filter.

-

Penetapan harga take profit dan stop loss yang tidak tepat dapat menyebabkan posisi ditutup terlalu awal. Dapat diuji dengan berbagai kombinasi parameter untuk mencari solusi optimal.

-

Pemilihan instrumen trading dan timeframe yang tidak tepat dapat menyebabkan strategi tidak efektif. Disarankan untuk melakukan optimasi dan pengujian parameter secara terpisah untuk setiap instrumen trading.

-

Ada risiko overfitting tertentu. Perlu dilakukan backtest di lebih banyak kondisi pasar untuk memastikan ketahanan strategi.

Arah Optimasi

Strategi ini dapat dioptimalkan dari beberapa arah berikut:

-

Menyesuaikan parameter filter ganda untuk menemukan kombinasi parameter terbaik.

-

Menguji dan memilih filter bantu yang paling optimal.

-

Mengoptimalkan algoritma take profit dan stop loss agar lebih cerdas.

-

Mencoba memperkenalkan metode seperti machine learning untuk menyesuaikan parameter secara dinamis.

-

Melakukan backtest pada lebih banyak instrumen trading dan dalam jangka waktu yang lebih panjang untuk meningkatkan stabilitas strategi.

Kesimpulan

Secara keseluruhan, strategi ini adalah strategi trading kuantitatif yang stabil, akurat, dan mudah dioptimalkan. Ia menggunakan filter tren ganda yang dikombinasikan dengan beberapa filter bantu untuk menghasilkan sinyal trading, mampu menyaring sebagian besar noise, sehingga sinyal menjadi lebih akurat dan andal. Selain itu, strategi ini memiliki pengaturan take profit dan stop loss bawaan, yang dapat mengurangi risiko trading. Ini adalah strategi yang sangat bernilai praktis, dan setelah dioptimalkan serta divalidasi, dapat langsung digunakan dalam perdagangan real-time. Strategi ini juga memiliki potensi pengembangan yang besar, menjadikannya strategi kuantitatif yang layak untuk diteliti lebih dalam.

- 1