Strategi Trading Jangka Pendek Berdasarkan Pembalikan Moving Average

Ikhtisar

Strategi Moving Average Reversal adalah strategi trading jangka pendek yang didasarkan pada pembalikan rata-rata bergerak. Strategi ini menggabungkan beberapa indikator seperti Bollinger Bands, RSI, CCI, dll., untuk menangkap perubahan jangka pendek di pasar keuangan, mencapai tujuan membeli di harga rendah dan menjual di harga tinggi.

Strategi ini terutama digunakan untuk instrumen dengan likuiditas tinggi seperti indeks saham, valuta asing, dan logam mulia. Ia mengupayakan maksimalisasi keuntungan per perdagangan sambil mengendalikan rasio risiko-imbal hasil secara keseluruhan.

Prinsip Strategi

-

Menggunakan Bollinger Bands untuk menilai area nilai ekstrem harga. Ketika harga mendekati pita atas Bollinger, pertimbangkan untuk menjual (short); ketika harga mendekati pita bawah Bollinger, pertimbangkan untuk membeli (long).

-

Menggabungkan indikator RSI untuk menilai apakah terjadi kondisi overbought atau oversold. Indikator RSI dapat secara efektif mengidentifikasi kondisi overbought/oversold.

-

Indikator CCI untuk mendeteksi sinyal pembalikan harga. Indikator CCI cukup sensitif terhadap situasi abnormal dan dapat secara efektif menangkap peluang pembalikan harga.

-

Harga menembus di atas rata-rata bergerak 5 periode untuk membeli (long), dan menembus di bawah rata-rata bergerak 5 periode untuk menjual (short). Posisi rata-rata bergerak mewakili kisaran harga utama saat ini, dan hubungan antara harga dan rata-rata bergerak mencerminkan potensi perubahan tren.

-

Setelah sinyal masuk dikonfirmasi, segera tutup posisi untuk mengunci keuntungan. Tetapkan stop loss berdasarkan kondisi retracement untuk keluar, mencapai tingkat kemenangan yang tinggi.

Keunggulan Strategi

- Kombinasi multi-indikator, meningkatkan akurasi sinyal

Strategi Moving Average Reversal secara bersamaan menggunakan beberapa indikator seperti Bollinger Bands, RSI, CCI. Indikator-indikator ini cukup sensitif terhadap perubahan harga, dan penggunaan kombinasi dapat meningkatkan akurasi sinyal serta mengurangi sinyal palsu.

- Aturan masuk yang ketat, menghindari mengejar kenaikan dan menjual saat turun

Strategi mensyaratkan sinyal indikator dan harga muncul secara bersamaan, menghindari kesesatan dari satu indikator. Juga mensyaratkan harga telah berbalik secara signifikan, mengurangi risiko terkait.

- Mekanisme stop loss yang efisien, mengendalikan kerugian per perdagangan

Terlepas dari posisi long atau short, strategi akan menetapkan garis stop loss yang cukup ketat. Begitu harga menembus garis stop loss ke arah yang tidak menguntungkan, strategi akan segera melakukan stop loss, menghindari kerugian besar tunggal.

- Take profit yang wajar, mengupayakan maksimalisasi keuntungan per perdagangan

Strategi akan menetapkan dua target take profit, merealisasikan keuntungan secara bertahap. Pada saat yang sama, setelah take profit, menggunakan trailing stop yang disesuaikan secara bertahap untuk memperluas ruang keuntungan per perdagangan.

Analisis Risiko

- Fluktuasi harga yang tajam, stop loss terpicu

Dalam kondisi fluktuasi harga yang tajam, garis stop loss mungkin tertembus, menyebabkan kerugian yang tidak perlu. Situasi ini biasanya terjadi pada fluktuasi harga abnormal akibat peristiwa besar.

Risiko ini dapat diatasi dengan memperlebar jarak stop loss, serta menghindari operasi selama periode peristiwa besar.

- Kenaikan yang terlalu agresif, tidak dapat berbalik

Ketika kenaikan terlalu agresif, harga sering naik terlalu cepat sehingga tidak dapat berbalik tepat waktu. Jika pada saat ini tetap bersikeras melakukan posisi jual (short), mungkin menghadapi risiko mengejar kenaikan dan menjual saat turun.

Dalam situasi ini, sebaiknya menunggu dan melihat, baru mempertimbangkan untuk masuk posisi jual ketika momentum kenaikan harga jelas melemah.

Arah Optimasi

- Optimasi parameter indikator, meningkatkan akurasi sinyal

Dapat menguji hasil backtest dari berbagai kombinasi parameter untuk memilih parameter terbaik. Misalnya, dapat mengoptimalkan parameter RSI, parameter CCI, dll.

- Menggabungkan indikator volume, menilai momen pembalikan yang sebenarnya

Dapat menambahkan indikator volume seperti volume perdagangan atau lebar Bollinger Bands. Ini dapat menghindari menghasilkan sinyal palsu ketika harga hanya melakukan penyesuaian kecil.

- Mengoptimalkan strategi take profit dan stop loss, memperluas keuntungan per perdagangan

Dapat menguji berbagai titik take profit dan stop loss untuk memaksimalkan keuntungan per perdagangan. Pada saat yang sama, juga harus menyeimbangkan risiko, menghindari stop loss yang mudah terpicu.

Kesimpulan

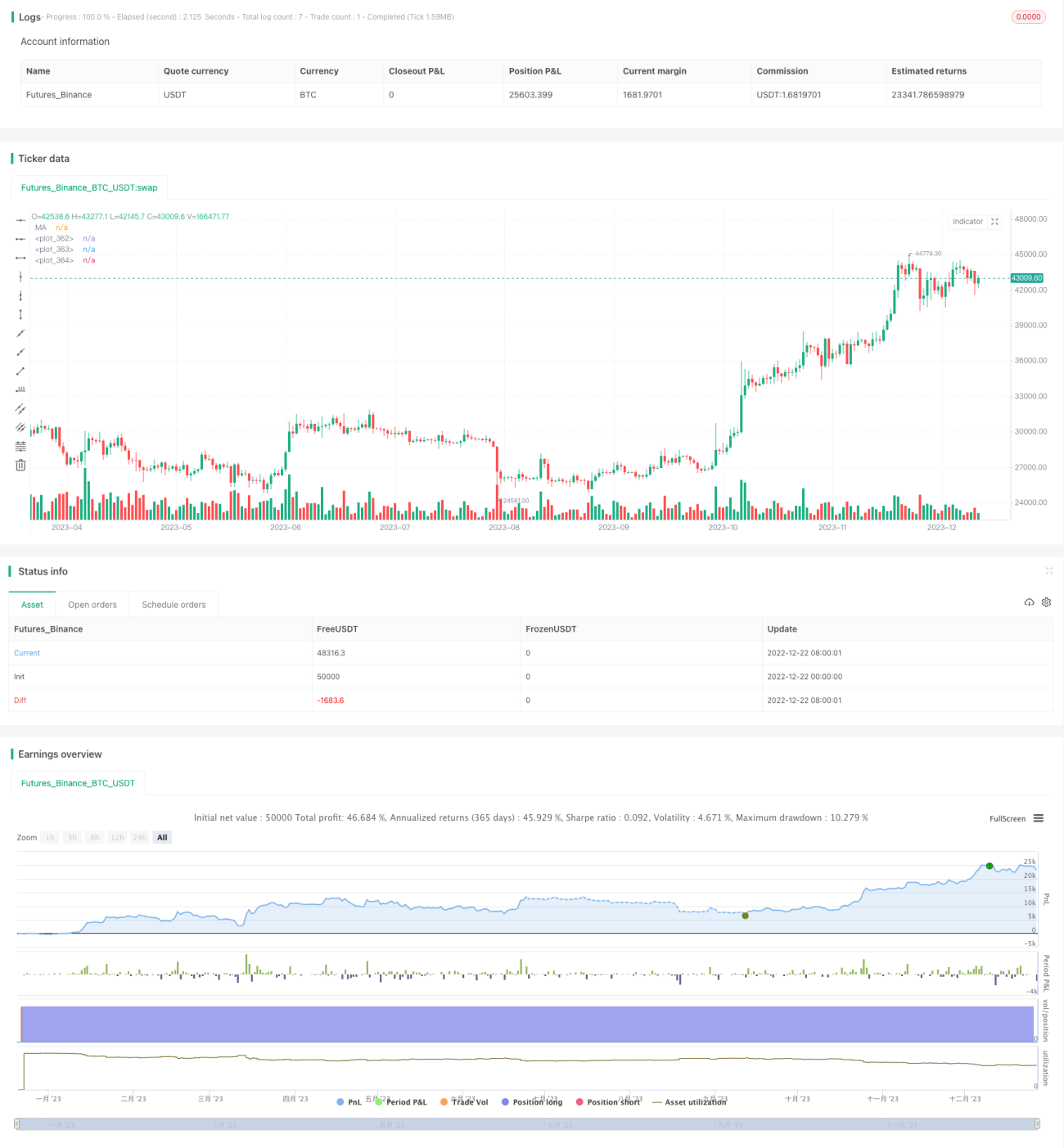

Strategi Moving Average Reversal secara komprehensif menggunakan kemampuan penilaian berbagai indikator, memiliki karakteristik sinyal yang akurat, operasi yang terstandarisasi, dan risiko yang terkendali. Ini cocok untuk instrumen dengan sensitivitas tinggi terhadap perubahan pasar dan likuiditas yang kuat, mampu menangkap peluang pembalikan harga antara Bollinger Bands dan rata-rata bergerak kunci, mencapai tujuan membeli di harga rendah dan menjual di harga tinggi.

Dalam penerapan praktis, tetap perlu memperhatikan optimasi parameter indikator, serta menggabungkan indikator volume untuk menilai titik pembalikan yang sebenarnya. Selain itu, harus melakukan manajemen risiko yang baik terhadap fluktuasi harga yang tajam. Jika digunakan dengan tepat, strategi ini dapat menghasilkan return Alpha yang relatif stabil.

- 1