Strategi Trailing Stop Bollinger Bands ATR

Ikhtisar

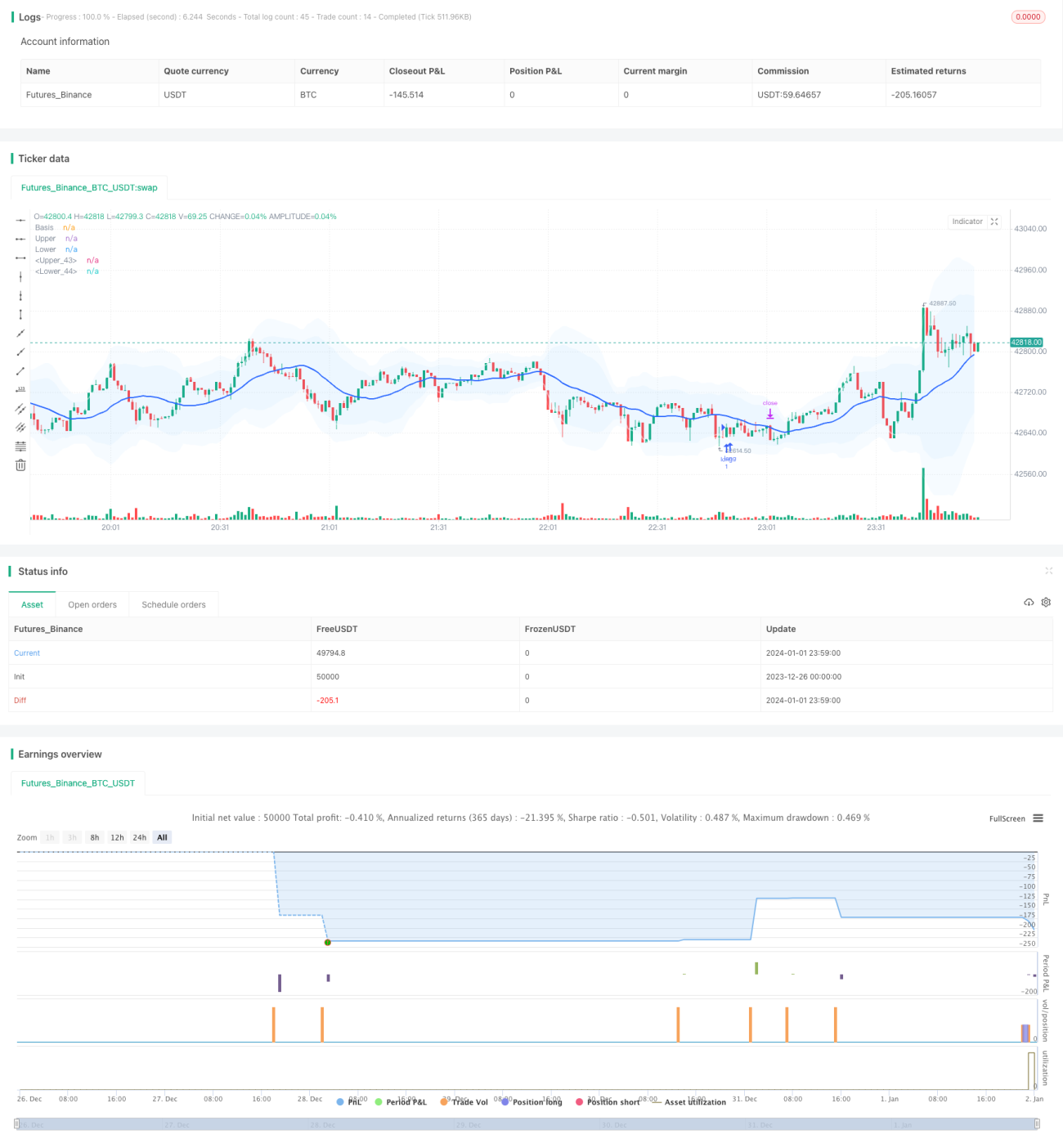

Strategi ini menggabungkan indikator Bollinger Bands dan indikator Average True Range (ATR) untuk membentuk strategi trading breakout dengan trailing stop. Ketika harga menembus upper band atau lower band Bollinger Bands dengan deviasi standar tertentu, sinyal trading dikeluarkan. Pada saat yang sama, indikator ATR digunakan untuk menghitung level stop loss dan take profit, sehingga mengontrol rasio risiko-hasil. Selain itu, strategi ini juga memiliki fitur filter waktu dan optimasi parameter.

Prinsip Strategi

Langkah pertama, hitung garis tengah (middle band), upper band, dan lower band. Garis tengah adalah Simple Moving Average (SMA) dari harga, sedangkan upper dan lower band adalah kelipatan dari standar deviasi harga. Ketika harga menembus ke atas dari lower band, lakukan posisi long; ketika menembus ke bawah dari upper band, lakukan posisi short.

Langkah kedua, hitung indikator ATR. ATR mencerminkan rata-rata rentang volatilitas harga. Berdasarkan nilai ATR, tetapkan level stop loss untuk posisi long dan short. Pada saat yang sama, tetapkan level take profit berdasarkan nilai ATR untuk mengontrol rasio risiko-hasil.

Langkah ketiga, gunakan filter waktu untuk hanya bertransaksi pada periode waktu yang ditentukan, untuk menghindari volatilitas ekstrem dari peristiwa berita besar.

Langkah keempat, mekanisme trailing stop. Sesuaikan level stop loss secara real-time berdasarkan posisi ATR terbaru untuk mengunci lebih banyak keuntungan.

Analisis Keunggulan

- Indikator Bollinger Bands sendiri mencerminkan pusat harga, lebih efektif daripada single moving average;

- Stop loss berbasis ATR membuat rasio risiko-hasil setiap posisi terkendali, efektif mengelola risiko;

- Trailing stop dapat menyesuaikan secara otomatis berdasarkan volatilitas pasar, mengunci lebih banyak keuntungan;

- Parameter strategi yang kaya, dapat dikustomisasi secara personal.

Analisis Risiko

- Ketika pasar berosilasi dan terkonsolidasi, sering terjadi kerugian kecil berulang;

- Breakout Bollinger Bands untuk reversal bisa gagal;

- Risiko trading pada malam hari dan saat berita besar tinggi, harus dihindari.

Tindakan korektif:

- Patuhi prinsip manajemen risiko dengan ketat, kendalikan kerugian per posisi;

- Optimalkan parameter untuk meningkatkan win rate;

- Gunakan filter waktu untuk menghindari periode berisiko tinggi.

Arah Optimasi

- Uji berbagai kombinasi parameter untuk konfigurasi optimal;

- Tambahkan indikator volume seperti OBV untuk pemilihan waktu;

- Tambahkan modul machine learning untuk optimasi.

Kesimpulan

Strategi ini secara komprehensif menggunakan Bollinger Bands untuk menentukan pusat tren dan arah breakout, ATR untuk menghitung take profit dan stop loss guna memastikan rasio risiko-hasil, serta trailing stop untuk mengunci keuntungan. Keunggulan strategi terletak pada kustomisasi yang tinggi, risiko yang terkendali, cocok untuk trading intraday jangka pendek. Optimasi parameter dan machine learning dapat lebih meningkatkan win rate dan profitabilitas strategi.

- 1