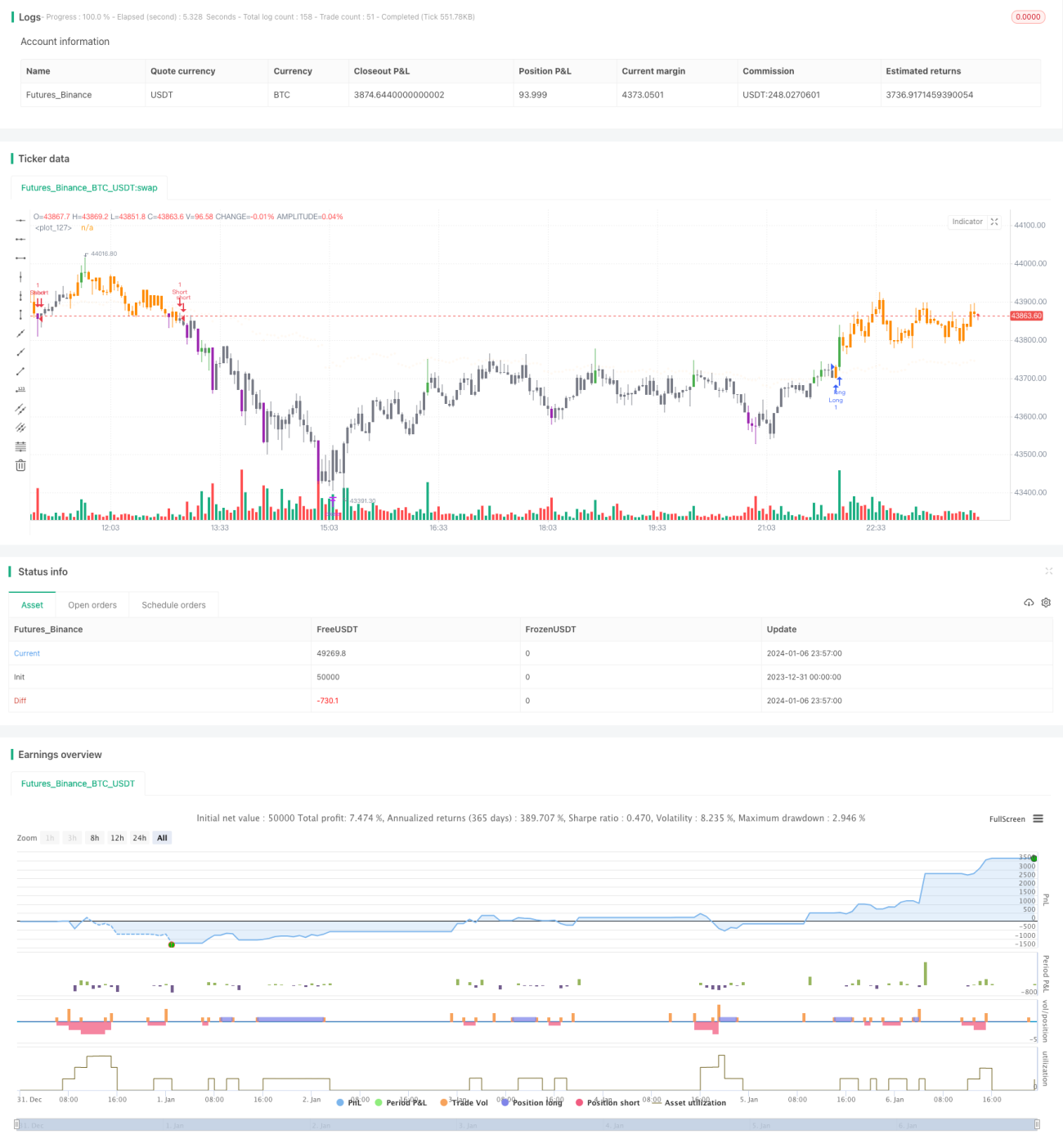

Strategi Trading Ranging Berdasarkan Dua Moving Average

Ikhtisar

Strategi ini adalah strategi trading osilasi berdasarkan dua rata-rata bergerak (double moving average). Strategi ini menggunakan persilangan antara rata-rata bergerak cepat (fast moving average) dan rata-rata bergerak lambat (slow moving average) sebagai sinyal beli dan jual. Sinyal beli dihasilkan ketika rata-rata bergerak cepat memotong ke atas dari bawah rata-rata bergerak lambat; sinyal jual dihasilkan ketika rata-rata bergerak cepat memotong ke bawah dari atas rata-rata bergerak lambat. Strategi ini cocok untuk kondisi pasar yang berosilasi, dapat menangkap fluktuasi harga jangka pendek untuk meraih keuntungan.

Prinsip Strategi

Strategi ini menggunakan RMA dengan panjang 6 sebagai rata-rata bergerak cepat, dan HMA dengan panjang 4 sebagai rata-rata bergerak lambat. Strategi menentukan tren harga dan menghasilkan sinyal trading melalui persilangan garis cepat dan garis lambat.

Ketika garis cepat memotong ke atas dari bawah garis lambat, hal ini menunjukkan harga dalam jangka pendek berubah dari turun menjadi naik, yang merupakan momen perpindahan posisi (chips conversion). Oleh karena itu, strategi menghasilkan sinyal beli pada saat ini. Ketika garis cepat memotong ke bawah dari atas garis lambat, hal ini menunjukkan harga dalam jangka pendek berubah dari naik menjadi turun, yang juga merupakan momen perpindahan posisi. Oleh karena itu, strategi menghasilkan sinyal jual pada saat ini.

Selain itu, strategi juga mendeteksi penilaian tren jangka panjang untuk menghindari trading melawan tren. Sinyal beli dan jual aktual hanya akan dihasilkan jika penilaian tren jangka panjang juga mendukung sinyal tersebut.

Keunggulan Strategi

Strategi ini memiliki keunggulan sebagai berikut:

- Menggunakan persilangan dua rata-rata bergerak, dapat mengidentifikasi titik balik harga jangka pendek secara efektif.

- Kombinasi panjang garis cepat dan garis lambat yang wajar dapat menghasilkan sinyal trading yang lebih akurat.

- Menggabungkan penilaian tren jangka panjang dan pendek dapat menyaring sebagian besar sinyal trading yang bersifat noise.

- Menerapkan logika take profit dan stop loss, yang secara aktif dapat menghindari risiko.

- Mudah dipahami dan diimplementasikan, cocok untuk pemula dalam trading kuantitatif.

Risiko dan Solusi

Strategi ini juga memiliki beberapa risiko:

-

Strategi dua rata-rata bergerak cenderung menghasilkan banyak keuntungan kecil namun satu kerugian besar. Solusinya adalah dengan menyesuaikan level take profit dan stop loss secara tepat.

-

Sinyal trading yang sering dalam kondisi pasar berosilasi dapat menyebabkan overtrading. Solusinya adalah dengan melonggarkan kondisi trading secara tepat untuk mengurangi jumlah transaksi.

-

Parameter strategi mudah dioptimasi secara berlebihan (overfitting), sehingga performa di pasar riil mungkin kurang baik. Solusinya adalah melakukan pengujian ketahanan parameter.

-

Strategi ini berkinerja buruk dalam kondisi pasar tren. Solusinya adalah menambahkan modul deteksi tren atau menggabungkannya dengan strategi tren.

Arah Optimasi

Arah optimasi lebih lanjut untuk strategi ini meliputi:

-

Memperbarui indikator rata-rata bergerak, menggunakan filter adaptif seperti Kalman.

-

Menambahkan modul machine learning, memanfaatkan pelatihan AI untuk menentukan titik beli dan jual.

-

Menambahkan modul manajemen modal agar pengendalian risiko lebih otomatis.

-

Menggabungkan dengan faktor frekuensi tinggi untuk mendapatkan sinyal trading yang lebih kuat.

-

Arbitrase multi-instrumen lintas pasar.

Kesimpulan

Secara keseluruhan, strategi osilasi dua rata-rata bergerak ini adalah strategi trading kuantitatif yang klasik dan praktis. Strategi ini memiliki adaptabilitas yang kuat, dan pemula dapat belajar banyak tentang pengembangan strategi darinya. Pada saat yang sama, strategi ini juga memiliki ruang perbaikan yang besar, dan dapat dioptimalkan lebih lanjut dengan menggabungkan lebih banyak teknik kuantitatif untuk mencapai hasil strategi yang lebih baik.

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-07 00:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © dc_analytics

// https://datacryptoanalytics.com/

- 1