Strategi Profit Jangka Pendek Berdasarkan Pola V pada RSI

Ringkasan

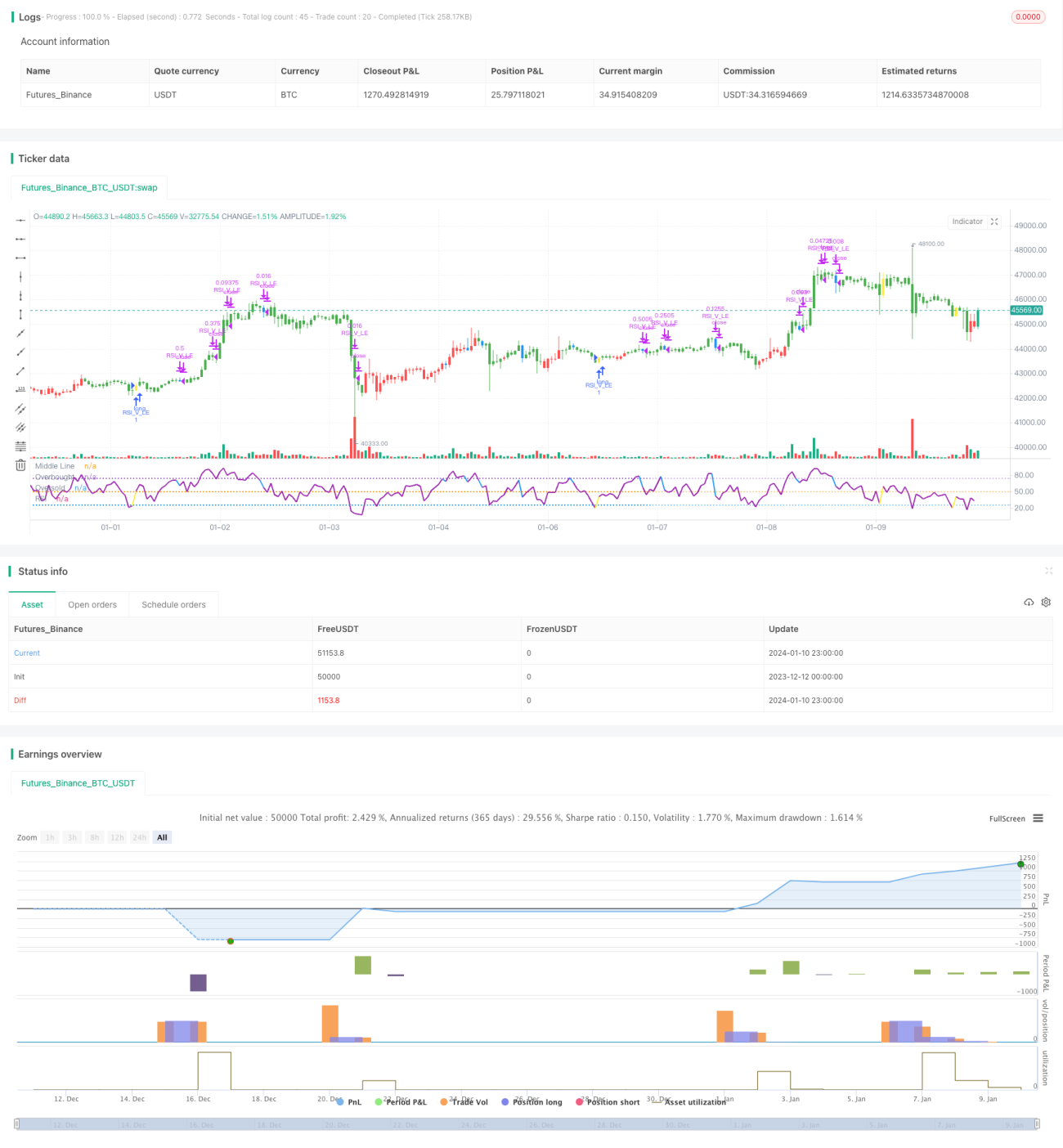

Strategi ini didasarkan pada formasi V dari indikator RSI, dikombinasikan dengan filter EMA, sehingga membentuk strategi profit jangka pendek yang cukup andal. Strategi ini dapat menangkap peluang rebound harga di area oversold, dengan sinyal formasi V RSI untuk melakukan posisi long secara tepat, sehingga mencapai keuntungan dalam jangka pendek.

Prinsip Strategi

- Menggunakan garis 20 hari di atas garis 50 hari sebagai penentu tren naik jangka panjang

- RSI membentuk formasi V, menunjukkan peluang rebound oversold

- Titik terendah candle sebelumnya lebih rendah dari titik terendah dua candle sebelumnya

- RSI candle saat ini lebih tinggi dari RSI dua candle sebelumnya

- RSI menembus ke atas 30 sebagai sinyal selesainya formasi V, lakukan long

- Stop loss ditetapkan 8% di bawah harga masuk

- RSI menembus 70 mulai menyesuaikan posisi tzinfo, stop loss dipindahkan ke harga masuk

- RSI menembus 90 mulai menyesuaikan 3/4 posisi tzinfo

- RSI menembus 10 / stop loss terpicu, tutup semua posisi

Analisis Keunggulan

- Menggunakan EMA untuk menentukan arah tren utama, menghindari trading melawan tren

- Formasi V RSI untuk mengidentifikasi peluang rebound di area oversold, menangkap tren pembalikan

- Mekanisme stop loss berganda untuk mengontrol risiko

Analisis Risiko

- Pasar yang turun tajam mungkin tidak dapat dihentikan kerugiannya, menyebabkan kerugian besar

- Sinyal formasi V RSI mungkin salah, menyebabkan kerugian yang tidak perlu

Arah Optimasi

- Optimalkan parameter RSI untuk mencari formasi V RSI yang lebih andal

- Gabungkan dengan indikator lain untuk menilai keandalan sinyal pembalikan

- Optimalkan strategi stop loss, untuk mencegah terlalu agresif sekaligus melakukan stop loss tepat waktu

Kesimpulan

Strategi ini mengintegrasikan filter EMA dan formasi V RSI, membentuk serangkaian strategi trading jangka pendek yang cukup andal. Strategi ini secara efektif dapat menangkap peluang rebound di area oversold, mencapai keuntungan dalam jangka pendek. Dengan terus mengoptimalkan parameter dan model, serta menyempurnakan mekanisme stop loss, strategi ini dapat semakin meningkatkan stabilitas dan profitabilitas. Ini membuka pintu lain menuju profit jangka pendek bagi para trader kuantitatif.

- 1