Strategi Mengikuti Tren Garis Rata-Rata Berdasarkan SSL

Ikhtisar

Strategi ini memanfaatkan indikator saluran SSL untuk menilai arah tren pasar, dan mengikuti tren berdasarkan rata-rata bergerak sebagai acuan. Cocok untuk grafik 4 jam dan harian jangka menengah-panjang.

Prinsip Strategi

-

Saluran SSL terdiri dari rata-rata bergerak Keltner dan amplitudo sebenarnya. Saluran ini dapat menentukan arah tren pasar. Ketika harga menembus pita atas, itu adalah sinyal bullish; ketika menembus pita bawah, itu adalah sinyal bearish.

-

Strategi ini menggunakan indikator rata-rata bergerak seperti EMA untuk menghitung garis rata-rata acuan. Garis ini dapat menyaring sebagian sinyal palsu.

-

Strategi akan melakukan posisi long (beli) ketika harga menembus garis atas SSL, dan posisi short (jual) ketika harga menembus garis bawah SSL. Dalam tren naik, strategi membeli saat harga naik dan menjual saat harga turun; dalam tren turun, strategi membeli saat harga rendah.

-

Metode stop-loss meliputi stop-loss persentase, stop-loss ATR, dan stop-loss berdasarkan harga tertinggi/terendah sebelumnya. Take-profit adalah kelipatan dari stop-loss. Parameter spesifik ditentukan oleh pengguna.

Analisis Keunggulan

-

Saluran SSL akurat dalam menentukan arah tren, mengurangi sinyal palsu. Dikombinasikan dengan rata-rata bergerak sebagai dasar masuk posisi, menghindari membeli di puncak dan menjual di dasar.

-

Fleksibel dalam memilih berbagai jenis rata-rata bergerak, sehingga dapat beradaptasi dengan kondisi pasar yang lebih luas.

-

Metode stop-loss yang fleksibel dan beragam, mengendalikan risiko. Kelipatan take-profit juga dapat diatur secara fleksibel untuk memenuhi preferensi yang berbeda.

-

Dapat melakukan posisi long dan short secara bersamaan, menggali peluang dua arah pasar secara maksimal.

Analisis Risiko

-

Semua indikator rata-rata bergerak memiliki keterlambatan, dapat menyebabkan akumulasi kerugian.

-

Dalam kondisi pasar yang berosilasi, saat harga menembus pita atas/bawah, bisa langsung berbalik arah, sehingga mudah terjebak.

-

Stop-loss ATR dan stop-loss harga sebelumnya mungkin terlalu longgar saat terjadi penembusan abnormal, memperbesar kerugian.

Langkah penanganan risiko:

- Sesuaikan parameter rata-rata bergerak, atau pilih jenis rata-rata bergerak lain.

- Perbesar jarak stop-loss, segera lakukan stop-loss.

- Tambahkan faktor kelipatan pada ATR, atau sesuaikan periode harga sebelumnya.

Arah Optimasi

- Uji lebih banyak jenis indikator rata-rata bergerak untuk menemukan parameter terbaik.

- Optimalkan parameter periode ATR untuk stop-loss.

- Uji berbagai parameter kelipatan stop-loss.

- Uji koefisien risiko take-profit yang berbeda.

Kesimpulan

Strategi ini menggabungkan saluran SSL untuk menilai tren dan indikator rata-rata bergerak untuk mengonfirmasi masuk posisi, secara efektif mengikuti tren. Strategi ini menyediakan cara stop-loss dan take-profit yang fleksibel, mengendalikan risiko sambil memperoleh keuntungan lebih tinggi. Dengan terus menguji dan mengoptimalkan parameter, kinerja perdagangan yang lebih baik dapat dicapai. Ini adalah strategi efektif yang layak untuk dilacak dan digunakan dalam jangka panjang.

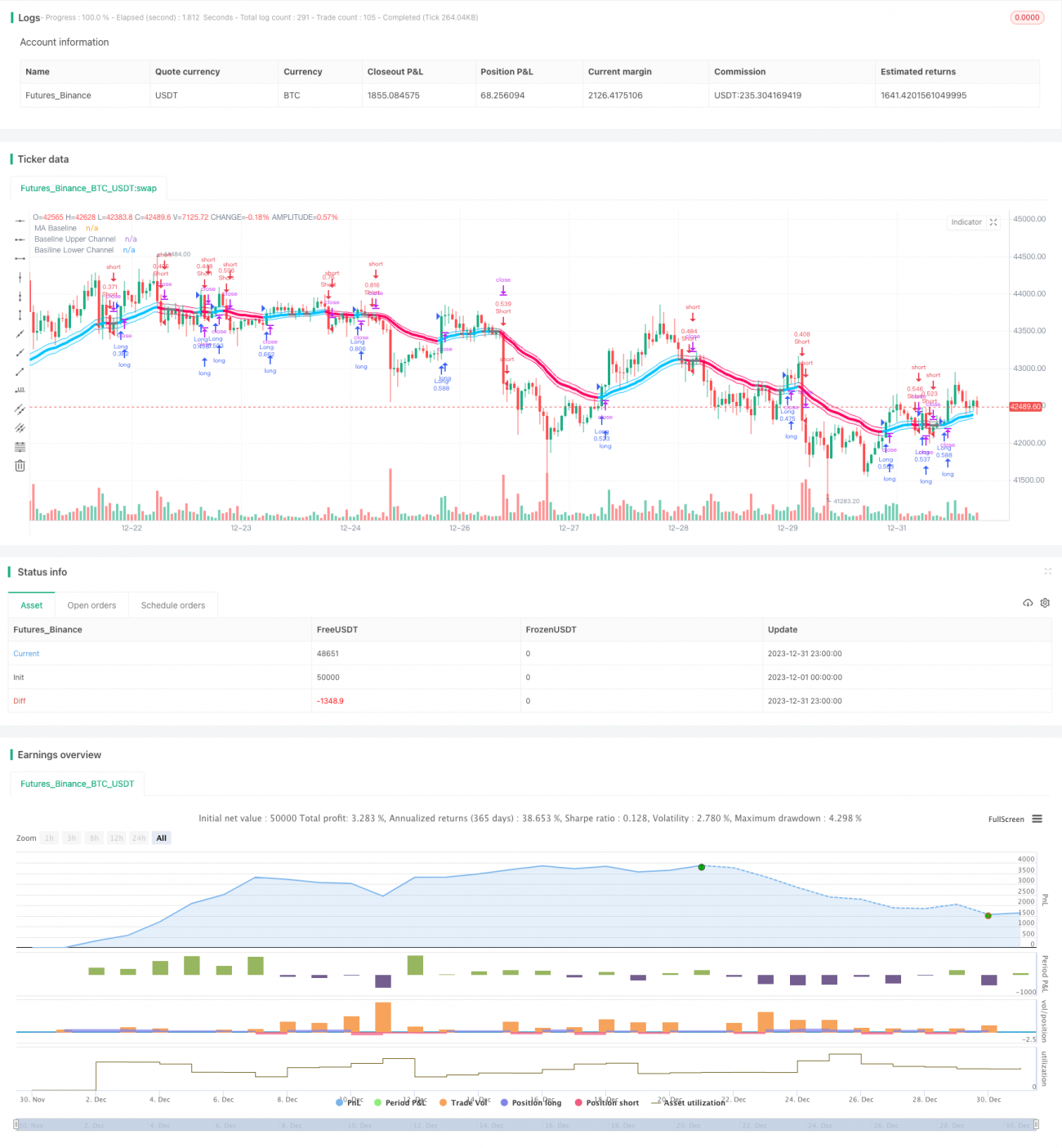

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// Thanks to @kevinmck100 for opensource strategy template and @Mihkel00 for SSL Hybrid

// @fpemehd

// @version=5- 1