Strategi Mengikuti Tren dengan Sabar

Sabar Mengikuti Strategi Tren

Ringkasan

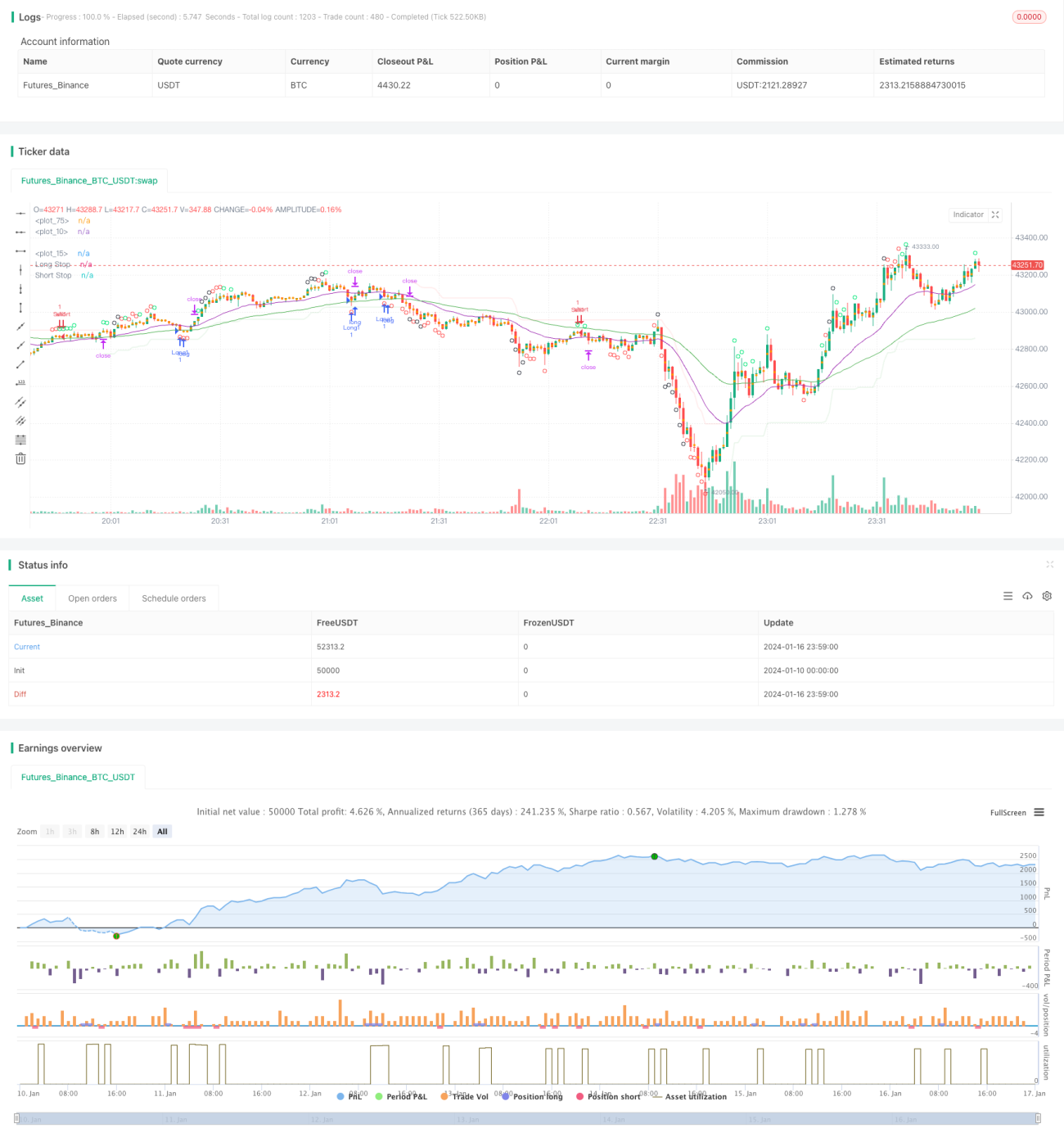

Strategi Sabar Mengikuti Tren adalah strategi pengikut tren. Strategi ini menggunakan kombinasi indikator moving average untuk menentukan arah tren, dan menggabungkannya dengan indikator overbought/oversold CCI untuk menghasilkan sinyal trading. Strategi ini mengejar tren besar, dan secara efektif dapat menghindari jebakan dalam kondisi pasar yang bergerak sideways (range-bound).

Prinsip Strategi

Strategi ini menggunakan kombinasi EMA 21 periode dan 55 periode untuk menentukan arah tren. Ketika EMA jangka pendek berada di atas EMA jangka panjang, itu didefinisikan sebagai tren naik; ketika EMA jangka pendek berada di bawah EMA jangka panjang, itu didefinisikan sebagai tren turun.

Indikator CCI digunakan untuk menentukan kondisi overbought/oversold. Ketika CCI menembus ke atas garis -100, itu adalah sinyal oversold di bagian bawah; ketika menembus ke bawah garis 100, itu adalah sinyal overbought di bagian atas. Berdasarkan garis overbought/oversold yang berbeda pada indikator CCI, strategi ini dibagi menjadi tiga tingkat kekuatan sinyal trading.

Ketika diputuskan sebagai tren naik, jika indikator CCI memberikan sinyal oversold kuat di bagian bawah, maka posisi beli (long) akan dimasukkan. Ketika diputuskan sebagai tren turun, jika indikator CCI memberikan sinyal overbought kuat di bagian atas, maka posisi jual (short) akan dimasukkan.

Stop loss ditetapkan berdasarkan indikator SuperTrend, dan target profit ditetapkan sebagai sejumlah poin (points) tetap.

Analisis Keunggulan

Strategi ini memiliki keunggulan utama sebagai berikut:

- Mengikuti tren besar, menghindari jebakan

- Indikator CCI secara efektif dapat menentukan titik pembalikan

- Pengaturan stop loss SuperTrend yang masuk akal

- Stop loss tetap dan take profit tetap, risiko terkendali

Analisis Risiko

Strategi ini memiliki risiko utama sebagai berikut:

- Probabilitas kesalahan dalam menentukan tren besar

- Probabilitas sinyal palsu dari indikator CCI

- Probabilitas stop loss yang tidak perlu karena titik stop loss yang terlalu sempit atau terlalu dalam

- Probabilitas take profit tetap yang tidak dapat terus mengikuti tren untuk mendapatkan keuntungan

Untuk mengatasi risiko-risiko ini, kita dapat mengoptimalkannya dengan menyesuaikan parameter periode EMA, parameter CCI, serta titik stop loss dan take profit. Pada saat yang sama, sangat penting juga untuk memperkenalkan lebih banyak indikator untuk memvalidasi sinyal strategi.

Arah Optimasi

Arah optimasi utama untuk strategi ini meliputi:

-

Menguji lebih banyak kombinasi indikator untuk menemukan indikator penentu tren dan validasi sinyal yang lebih optimal.

-

Menggunakan ATR untuk stop loss dan take profit dinamis guna melacak tren dan mengendalikan risiko dengan lebih baik.

-

Memperkenalkan model machine learning yang dilatih berdasarkan data historis untuk memprediksi probabilitas tren.

-

Melakukan penyesuaian dan optimasi parameter untuk instrumen yang berbeda.

Kesimpulan

Strategi Sabar Mengikuti Tren secara keseluruhan adalah strategi pengikut tren yang sangat praktis. Strategi ini menggunakan moving average untuk menentukan arah tren besar, indikator CCI untuk menemukan sinyal titik pembalikan, dan garis stop loss SuperTrend yang ditetapkan dengan wajar. Melalui penyesuaian parameter dan kombinasi validasi multi-indikator, strategi ini dapat dioptimalkan lebih lanjut dan layak untuk dilacak serta divalidasi dalam perdagangan riil jangka panjang.

- 1