Strategi kuantitatif jangka pendek berdasarkan RSI dan VWAP

Ringkasan

Strategi ini diberi nama "Strategi Jangka Pendek RSI-VWAP". Strategi ini menggunakan indikator RSI dan Volume Weighted Average Price (VWAP) sebagai indikator teknis, menetapkan sinyal long dan short, sehingga menghasilkan keputusan beli dan jual. Strategi ini bertujuan untuk menangkap kondisi overbought dan oversold pasar dalam jangka pendek, dengan harapan memperoleh keuntungan berlebih.

Prinsip Strategi

- Menggunakan indikator RSI untuk menentukan apakah pasar berada dalam kondisi overbought atau oversold. Nilai RSI di atas 80 adalah zona overbought, di bawah 20 adalah zona oversold.

- Indikator RSI menggunakan VWAP sebagai sumber data, bukan harga penutupan. VWAP lebih mencerminkan harga rata-rata perdagangan harian.

- Ketika nilai RSI menembus ke atas dari 20 dari zona oversold, sinyal beli dihasilkan. Ketika nilai RSI menembus ke bawah dari 80 dari zona overbought, sinyal jual dihasilkan.

- Strategi ini hanya melakukan posisi long, tidak short. Artinya, hanya membeli saat oversold dan menjual saat overbought.

Analisis Keunggulan

- Menggunakan VWAP sebagai sumber data RSI membuat indikator RSI lebih akurat dalam menilai pasar, menghindari kesalahan akibat breakout palsu.

- Hanya melakukan posisi long, mengurangi frekuensi perdagangan, yang bermanfaat untuk memperoleh keuntungan yang stabil dalam jangka panjang.

- Parameter RSI adalah 17, cocok untuk perdagangan jangka pendek.

- Menggunakan metode perdagangan jangka pendek dengan jumlah transaksi yang tidak terlalu tinggi, mengurangi biaya perdagangan, sehingga membantu memperoleh tingkat pengembalian yang lebih tinggi.

Analisis Risiko

- Pengujian ulang strategi kuantitatif memiliki risiko overfitting, hasil perdagangan nyata mungkin tidak sesuai dengan hasil backtest.

- Hanya melakukan posisi long tidak dapat memanfaatkan peluang saat tren turun.

- Standar penentuan overbought/oversold mungkin tidak cocok untuk semua instrumen, perlu menyesuaikan parameter untuk setiap instrumen.

- Indikator teknis apa pun dapat menghasilkan sinyal yang salah, tidak dapat sepenuhnya menghindari terjadinya kerugian.

Risiko dapat dikurangi dengan melonggarkan standar overbought/oversold, menggabungkan indikator lain untuk mengonfirmasi sinyal, menyesuaikan rentang parameter, dan metode lainnya.

Arah Optimasi

- Menguji pengaruh parameter yang berbeda terhadap kinerja strategi, mengoptimalkan panjang RSI dan ambang batas overbought/oversold.

- Menambahkan strategi stop-loss, melalui trailing stop, time stop, dll. untuk mengunci sebagian keuntungan dan mengurangi drawdown.

- Menggabungkan indikator lain untuk memfilter sinyal, meningkatkan akurasi sinyal.

- Menetapkan rentang parameter independen berdasarkan karakteristik masing-masing instrumen, sehingga strategi dapat beradaptasi lebih baik dengan berbagai instrumen.

Kesimpulan

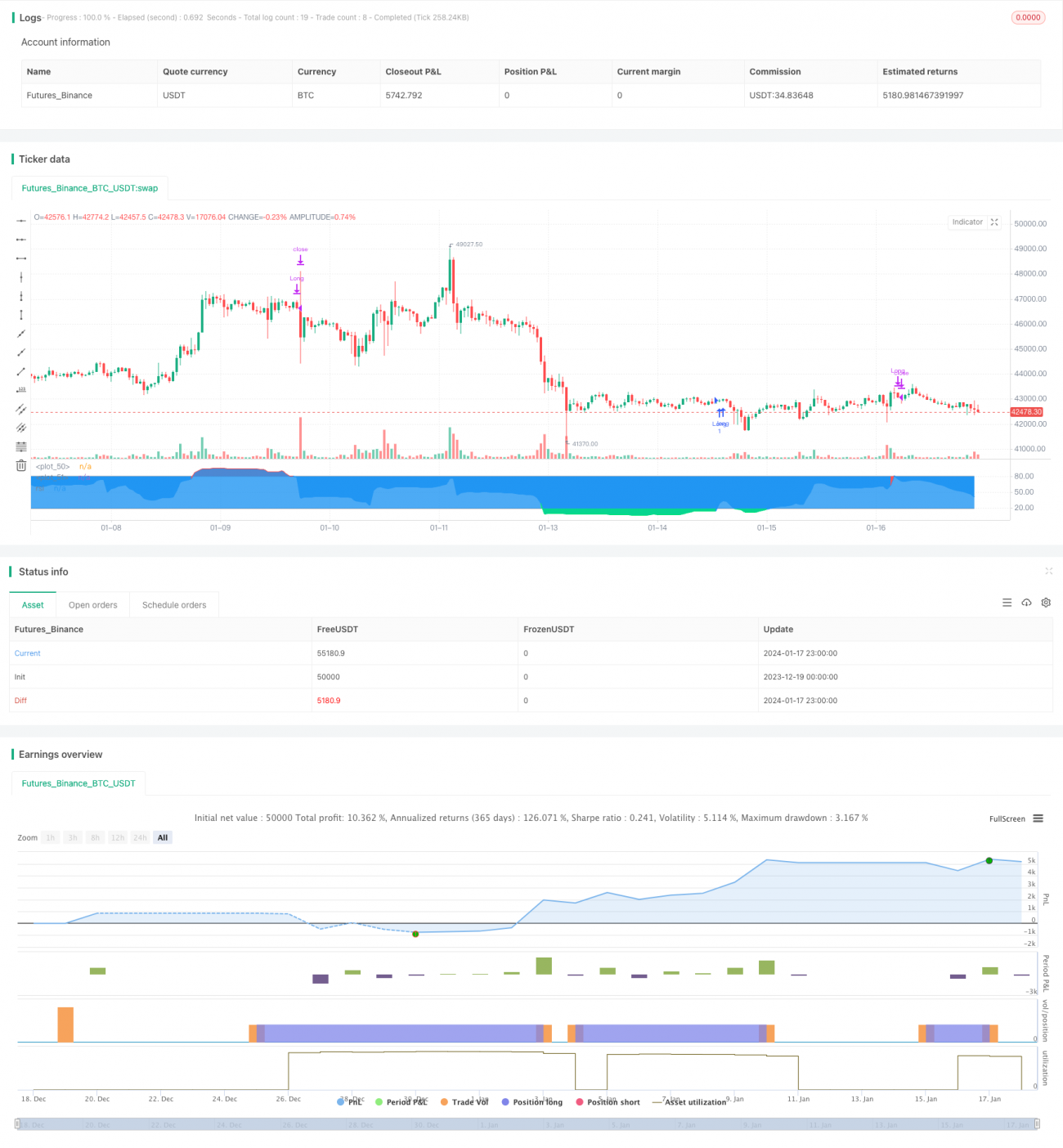

Secara keseluruhan, strategi ini adalah strategi jangka pendek yang sederhana dan praktis. Penggunaan VWAP membuat penilaian indikator RSI lebih akurat, dan hanya melakukan posisi long mengurangi frekuensi perdagangan. Ide strategi jelas, mudah dipahami dan diimplementasikan, cocok untuk pemula dalam perdagangan kuantitatif. Namun, strategi indikator tunggal mana pun sulit untuk sempurna, dan masih perlu dioptimalkan terus-menerus agar menghasilkan kinerja perdagangan nyata yang lebih baik.

/*backtest

start: 2023-12-19 00:00:00

end: 2024-01-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Xaviz

//#####©ÉÉÉɶN###############################################- 1