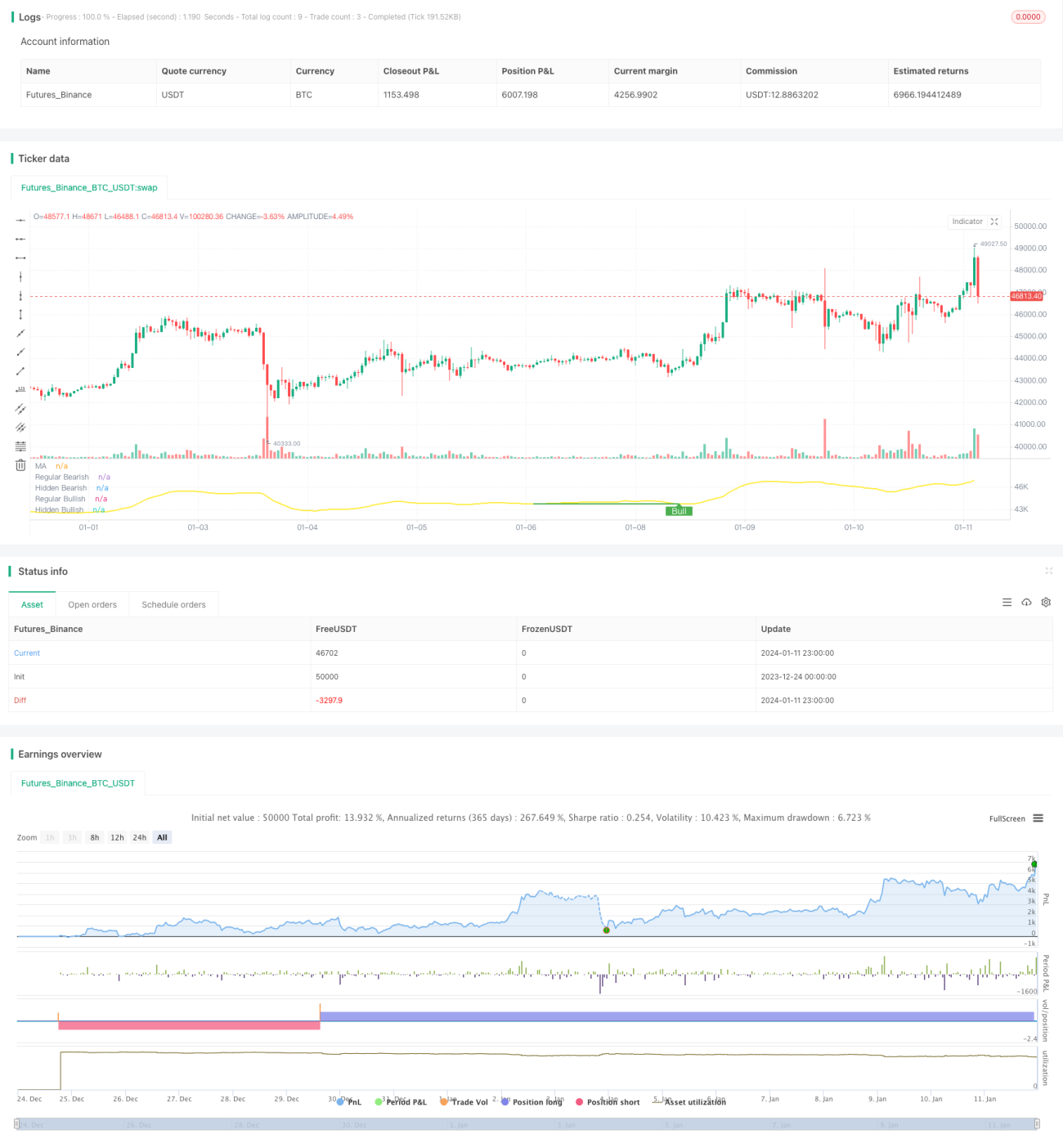

Strategi divergensi berbasis rata-rata bergerak

1

Follow

1788

Followers

Ringkasan

Strategi ini bekerja dengan menghitung Moving Average dan pivot point-nya, dan menemukan deviasi antara harga dan Moving Average, sebagai sinyal untuk membeli dan menjual. Ini dapat diterapkan pada indikator osilasi apa pun untuk menemukan deviasi. Ini adalah alat yang berharga yang dapat digunakan untuk retrospeksi dan perdagangan langsung.

Prinsip Strategi

- Penghitungan panjang adalah Moving Average of Len (MA)

- Deteksi MA pada titik pivotal rendah (PL) dan titik pivotal tinggi (PH)

- Penilaian apakah ada deviasi positif: harga menginovasi low point dan MA tidak menginovasi low atau harga tidak menginovasi low point dan MA menginovasi low

- Periksa apakah ada reversal deviasi: harga inovasi tinggi dan MA tidak inovasi tinggi atau harga tidak inovasi tinggi dan MA inovasi tinggi

- Membeli dan menjual berdasarkan situasi yang berbeda

Analisis Keunggulan

- Dapat secara otomatis mendeteksi deviasi antara harga dan MA, menghindari kesalahan penilaian manual

- Dapat diterapkan pada indikator osilasi apa pun, sangat ekspansif

- Dapat digunakan untuk mengevaluasi kembali profitabilitas strategi

- Parameter yang dapat dikonfigurasi menyesuaikan sensitivitas untuk menghindari sinyal yang salah

- Berbagai jenis deviasi, penilaian yang akurat dan komprehensif

Analisis risiko

- Jika indikator osilasi tidak diatur dengan benar, dapat menghasilkan banyak sinyal yang salah

- Pembagian dari titik pusat yang diperlukan sebelum terjadi, kemungkinan kurangnya sinyal

- Parameter harus disesuaikan untuk menyeimbangkan sensitivitas dengan sinyal kesalahan penyaringan

- Lebih efektif bila dikombinasikan dengan faktor-faktor lain, dan kurang dapat diandalkan bila digunakan sendiri

Arah optimasi

- Mengoptimalkan parameter moving average untuk mencari kombinasi parameter yang optimal

- Gabungan dengan indikator lain seperti indikator harga dan kuantitas untuk menghindari sinyal yang salah

- Menambahkan penilaian model pembelajaran mesin jauh dari kepercayaan

- Meningkatkan mekanisme manajemen risiko untuk mengendalikan kerugian tunggal

Meringkaskan

Strategi ini dapat mengotomatiskan penilaian dan menghindari kesalahan subjektif dengan mendeteksi perbedaan antara harga dan rata-rata bergerak sebagai sinyal perdagangan. Ini dapat diterapkan secara luas pada indikator osilasi apa pun dan memiliki skalabilitas yang kuat.

Source

Pine

/*backtest

start: 2023-12-24 00:00:00

end: 2024-01-12 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © tista

//https://www.tradingview.com/u/tista/#published-scripts

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1