Strategi Perdagangan Mengikuti Tren Berdasarkan Volume Oscillator

Ikhtisar

Strategi ini adalah strategi pengikut tren yang berdagang berdasarkan indikator osilator volume yang dimodifikasi. Strategi ini menggunakan rata-rata bergerak volume untuk mengidentifikasi sinyal peningkatan volume, sehingga menentukan kapan harus masuk atau keluar dari posisi. Pada saat yang sama, strategi ini menggabungkan penilaian tren harga itu sendiri untuk menghindari sinyal palsu saat harga berfluktuasi.

Prinsip Strategi

- Hitung rata-rata bergerak volume

vol_sumdengan panjangvol_length, lalu lakukan penghalusan rata-rata bergerak dengan panjangvol_smooth. - Ketika

vol_sumnaik melebihi ambang batasthreshold, hasilkan sinyal beli; ketika turun melebihi ambang batas, hasilkan sinyal jual. - Untuk menyaring kesalahan operasi, operasi beli hanya dilakukan jika dibandingkan dengan harga penutupan

directionbatang sebelumnya dan tren harga naik. Operasi jual hanya dilakukan jika tren harga turun. - Tetapkan dua ambang batas:

thresholddanthreshold2.thresholddigunakan untuk menghasilkan sinyal perdagangan,threshold2digunakan untuk stop loss. - Kelola logika buka/tutup posisi melalui mesin keadaan.

Analisis Keunggulan

- Menggunakan indikator volume dapat menangkap perubahan kekuatan jual-beli di pasar, sehingga meningkatkan akurasi sinyal.

- Dengan menggabungkan penilaian tren harga, dapat menghindari sinyal palsu saat harga berfluktuasi.

- Menggunakan dua ambang batas untuk membuka posisi dan stop loss memungkinkan kontrol risiko yang lebih baik.

Analisis Risiko

- Indikator volume sendiri memiliki sifat lag, sehingga mungkin melewatkan titik balik harga.

- Pengaturan parameter yang salah dapat menyebabkan frekuensi perdagangan terlalu tinggi atau sinyal tertunda.

- Dalam skenario lonjakan volume, titik stop loss mungkin dapat ditembus.

Risiko-risiko ini dapat dikendalikan dengan menyesuaikan parameter, mengoptimalkan metode perhitungan indikator, dan menggabungkan konfirmasi dari indikator lain.

Arah Optimasi

- Dapat dipertimbangkan untuk mengoptimalkan parameter indikator secara adaptif, menyesuaikan secara otomatis berdasarkan kondisi pasar.

- Dapat menggabungkan indikator lain, misalnya osilator harga, untuk memverifikasi sinyal lebih lanjut guna meningkatkan akurasi.

- Dapat diteliti penerapan model pembelajaran mesin dalam penilaian sinyal, menggunakan model untuk meningkatkan akurasi.

Kesimpulan

Strategi ini menggunakan osilator volume yang ditingkatkan, dibantu dengan penilaian tren harga, dan menetapkan dua ambang batas untuk membuka posisi dan stop loss. Secara keseluruhan, ini adalah strategi pengikut tren yang cukup stabil. Ruang optimasi terutama terletak pada penyesuaian parameter, penyaringan sinyal, dan strategi stop loss. Secara keseluruhan, strategi ini memiliki nilai praktis tertentu dan layak untuk diteliti dan dioptimalkan lebih lanjut.

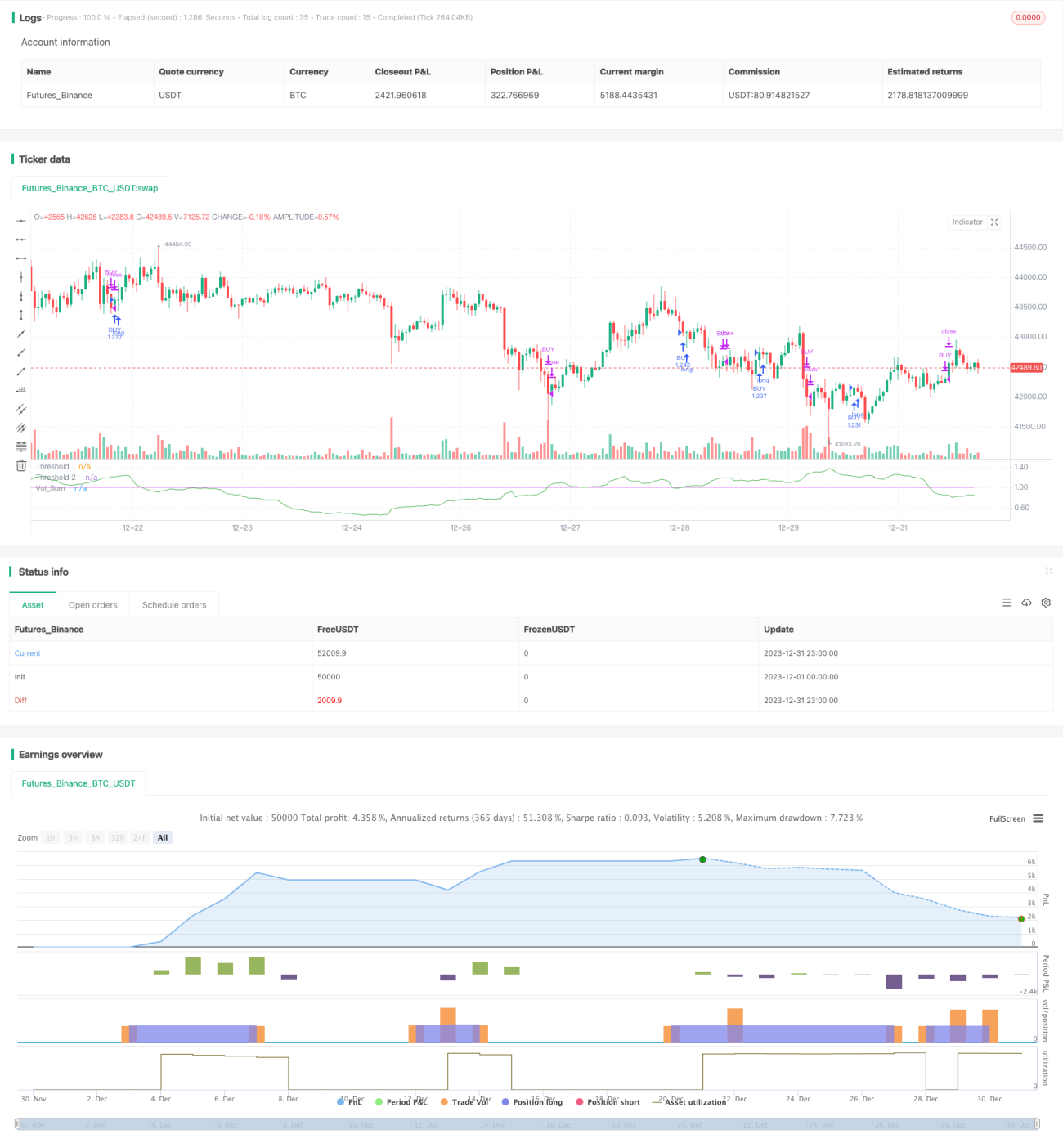

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy('Volume Advanced', default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.075, currency='USD')

startP = timestamp(input(2017, "Start Year"), input(12, "Start Month"), input(17, "Start Day"), 0, 0)

end = timestamp(input(9999, "End Year"), input(1, "End Month"), input(1, "End Day"), 0, 0)- 1