Strategi Swing Tiga Moving Average yang Menganalisis dengan Sabar Informasi Berharga dari Candlestick

Gambaran Umum

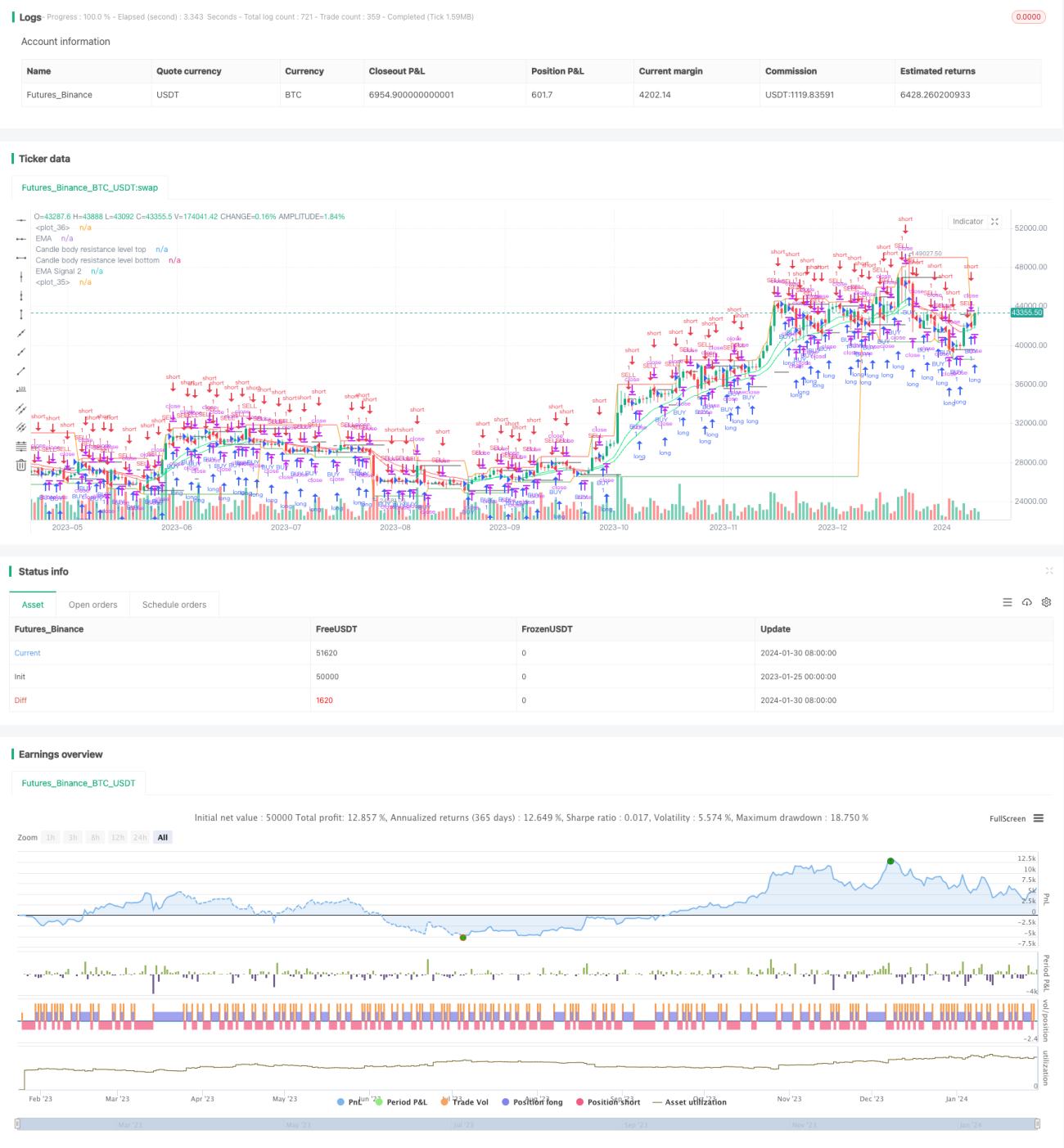

Strategi gelombang tiga rata-rata bergerak menggunakan beberapa indikator moving average, dengan menganalisis candlestick secara mendalam untuk menggali pola yang tersembunyi dalam fluktuasi harga, sehingga mencapai perdagangan arbitrase berisiko rendah.

Prinsip Strategi

Strategi ini menumpuk beberapa grup indikator EMA di atas Bollinger Bands, membangun saluran harga, dan menemukan pola fluktuasi harga. Secara spesifik:

- Menggunakan indikator BodyResistanceChannel untuk menggambar level resistensi badan candlestick.

- Menggunakan indikator Support/Resistance untuk menggambar level support dan resistensi multi-hari.

- Menggunakan sistem dual EMA untuk menilai arah tren harga.

- Menggunakan indikator Hull Moving Average untuk menghaluskan kurva harga.

Atas dasar ini, dikombinasikan dengan pengenalan pola untuk mengidentifikasi peluang pembalikan, lalu menyusun strategi perdagangan arbitrase.

Analisis Keunggulan

Strategi ini memiliki keunggulan sebagai berikut:

- Menggunakan beberapa grup EMA untuk membangun saluran harga, sehingga arah fluktuasi harga dapat dinilai secara jelas.

- Penerapan indikator Hull Moving Average dapat secara efektif menghaluskan penilaian breakout harga.

- Menggabungkan pola pembalikan dan indikator saluran, mewujudkan perdagangan berpeluang tinggi dan berisiko rendah.

- Membangun sistem indikator multi-lapis, sinyal perdagangan stabil dan andal.

Analisis Risiko

Strategi ini juga memiliki risiko sebagai berikut:

- Risiko kerugian besar akibat pecahnya saluran harga. Solusi yang ditargetkan adalah menggunakan stop loss bergerak untuk mengurangi kerugian per transaksi.

- Risiko sinyal palsu akibat kesalahan identifikasi pola pembalikan. Solusi yang ditargetkan adalah mengoptimalkan parameter untuk meningkatkan akurasi identifikasi pola.

- Risiko penurunan kualitas sinyal perdagangan akibat ketidaksesuaian parameter indikator. Solusi yang ditargetkan adalah melakukan pengujian optimasi parameter multi-kombinasi.

Arah Optimasi

Arah utama yang dapat dioptimalkan pada strategi ini adalah:

- Mengoptimalkan kombinasi parameter periode EMA agar indikator lebih cocok dengan karakteristik pasar.

- Menyesuaikan posisi stop loss untuk meminimalkan risiko kerugian per transaksi sambil tetap menjamin profitabilitas.

- Menambahkan modul penyesuaian posisi dinamis berbasis volatilitas untuk mengontrol risiko secara efektif.

- Memanfaatkan teknologi pembelajaran mendalam untuk menggali lebih banyak pola harga, meningkatkan kualitas sinyal.

Kesimpulan

Strategi gelombang tiga rata-rata bergerak secara mendalam menggali pola fluktuasi harga, stabil dan efisien, layak untuk diterapkan jangka panjang dan dioptimalkan secara berkelanjutan. Investasi membutuhkan rasionalitas dan kesabaran, bertransaksi secara bertahap adalah kunci kemenangan.

- 1