Strategi kuantitatif pengikut tren berdasarkan indikator Hull dan indikator LSMA

Ikhtisar

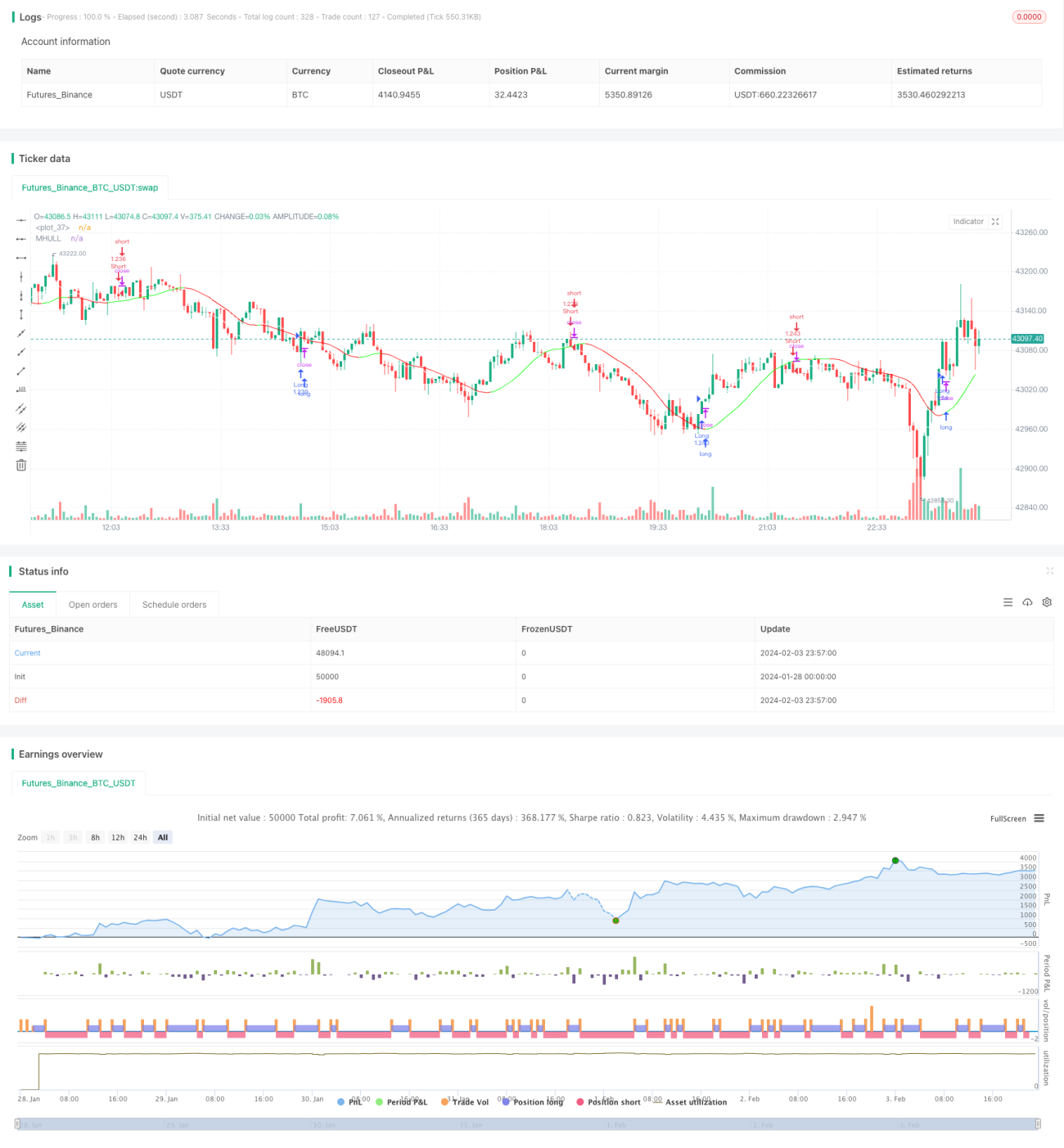

Strategi ini mengidentifikasi arah tren dan titik pembalikan tren dengan menggabungkan indikator Hull dan LSMA (Least Squares Moving Average), sehingga dapat mengikuti tren. Ketika indikator Hull menunjukkan tren naik dan LSMA melintasi ke atas Hull, maka lakukan posisi long; ketika indikator Hull menunjukkan tren turun dan LSMA melintasi ke bawah Hull, maka lakukan posisi short. Strategi ini cocok untuk trading frekuensi menengah-rendah dan dapat digunakan pada kerangka waktu 1 menit.

Prinsip Strategi

- Indikator Hull digunakan untuk menentukan arah tren harga. Ketika garis tengah (MHULL) berada di atas garis bawah (LHULL), ini menunjukkan tren naik; sebaliknya menunjukkan tren turun.

- Indikator LSMA digunakan untuk mengidentifikasi titik pembalikan tren. Ketika LSMA melintasi ke atas MHULL, ini menunjukkan tren naik terbentuk atau dipercepat; ketika LSMA melintasi ke bawah MHULL, ini menunjukkan tren turun terbentuk atau dipercepat.

- Menggabungkan keduanya, ketika indikator Hull menunjukkan tren naik (MHULL > LHULL) dan LSMA melintasi ke atas MHULL, lakukan long; ketika indikator Hull menunjukkan tren turun (MHULL < LHULL) dan LSMA melintasi ke bawah MHULL, lakukan short.

- Stop loss ditetapkan pada titik volatilitas terdekat. Stop loss untuk posisi long adalah titik terendah terbaru, stop loss untuk posisi short adalah titik tertinggi terbaru.

Analisis Keunggulan

Strategi ini memiliki keunggulan sebagai berikut:

- Indikator Hull bereaksi cepat, mampu menangkap perubahan tren tepat waktu; LSMA memiliki sifat smoothing yang kuat, mengidentifikasi sinyal pembalikan dengan akurat dan andal. Kombinasi keduanya memberikan efek yang baik.

- Dengan menggunakan persilangan LSMA untuk menyaring sinyal palsu dari indikator Hull, mengurangi kemungkinan kesalahan trading.

- Menggunakan titik volatilitas sebagai level stop loss, melindungi keamanan modal secara maksimal.

- Cocok untuk trading frekuensi menengah-rendah, dapat digunakan pada kerangka waktu 1 menit atau bahkan lebih rendah, memiliki penerapan yang luas.

Analisis Risiko

Strategi ini juga memiliki beberapa risiko:

- Dalam pasar yang bergerak sideway (ranging), indikator Hull dan LSMA dapat menghasilkan beberapa persilangan yang menyebabkan trading terlalu sering. Parameter harus disesuaikan dengan tepat untuk mengurangi frekuensi trading.

- Stop loss yang ditetapkan pada titik volatilitas dapat terpicu karena penyesuaian harga jangka pendek, sebaiknya melebarkan jarak stop loss secara memadai.

- Karena sifat lagging dari indikator LSMA, mungkin ada risiko kesalahan identifikasi. Sebaiknya dikonfirmasi dengan indikator lain seperti pola candlestick.

Arah Optimasi

Strategi ini dapat dioptimalkan dari beberapa aspek berikut:

- Optimasi parameter indikator Hull dan LSMA agar kombinasi lebih cocok untuk berbagai instrumen dan periode waktu.

- Menambahkan kondisi penyaringan berdasarkan volatilitas, volume trading, dll., untuk menghindari kesalahan trading dalam pasar yang sideway.

- Menambahkan algoritma pembelajaran mesin sebagai bantuan untuk menentukan kecenderungan tren.

- Menggabungkan teknik pembelajaran mendalam untuk mengidentifikasi area support/resistance kunci, sehingga stop loss menjadi lebih rasional.

Kesimpulan

Strategi ini menggunakan kombinasi indikator Hull dan LSMA untuk menilai perubahan arah tren dan menerapkan trading dengan mengikuti tren. Kelebihannya adalah operasi sederhana, respons cepat, dan dapat diterapkan secara luas pada trading kuantitatif frekuensi menengah-rendah. Dengan mengoptimalkan lebih lanjut kondisi penyaringan, bantuan penilaian, dan algoritma stop loss, diharapkan dapat diperoleh hasil strategi yang lebih baik.

- 1