Strategi Breakout Bullish Berdasarkan Bollinger Bands dan VWAP

Gambaran Umum

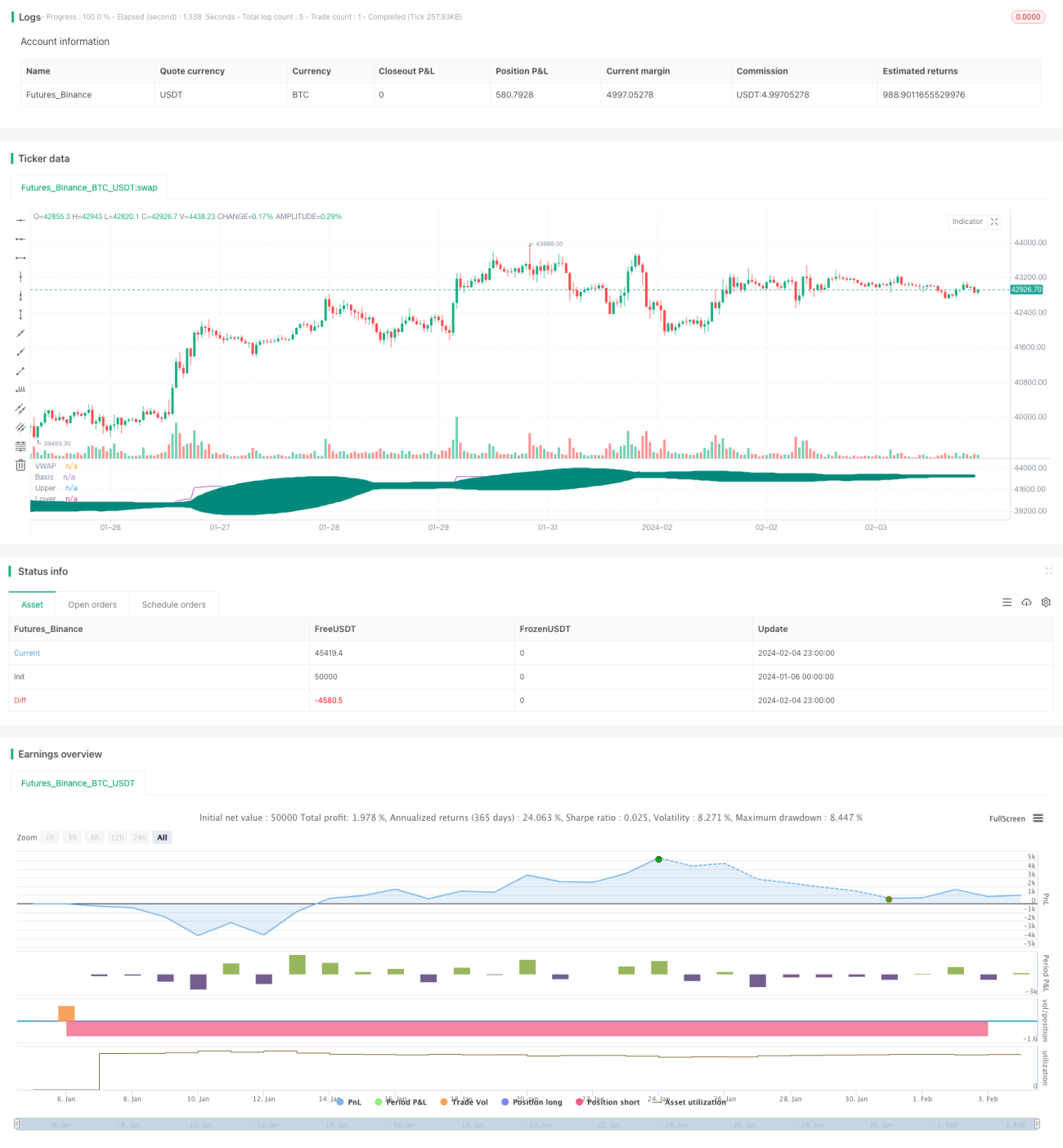

Strategi ini menggunakan indikator Bollinger Bands untuk melacak VWAP. Ketika VWAP menembus ke atas garis tengah Bollinger Bands, ini dianggap sebagai breakout bullish dan strategi long diambil. Sebaliknya, ketika VWAP menembus ke bawah garis bawah Bollinger Bands, ini dianggap sebagai konfirmasi bearish dan posisi ditutup. Selain itu, strategi ini juga menyertakan level support utama Pivot Point sebagai kondisi bantu untuk sinyal masuk, sehingga dapat menyaring beberapa breakout palsu.

Prinsip Strategi

- Hitung nilai VWAP.

- Hitung Bollinger Bands dari VWAP, yang terdiri dari garis atas, garis tengah, dan garis bawah.

- Periksa apakah VWAP menembus ke atas garis tengah Bollinger Bands. Jika ya, dan harga di atas level support utama Pivot Point, maka ambil posisi long.

- Stop loss ditetapkan sebesar 5%.

- Jika VWAP menembus ke bawah garis bawah Bollinger Bands, maka dianggap bearish telah terkonfirmasi dan posisi ditutup; jika stop loss tersentuh, juga keluar dari posisi.

Analisis Keunggulan

- VWAP memiliki kemampuan mengikuti tren yang kuat, dikombinasikan dengan Bollinger Bands dapat secara akurat menentukan awal tren.

- Penambahan Pivot Point sebagai kondisi bantu dapat menyaring banyak breakout palsu, menghindari kerugian yang tidak perlu.

- Menggunakan strategi keluar sebagian dapat mengunci sebagian keuntungan dan mengendalikan risiko.

- Hasil backtesting menunjukkan bahwa strategi ini berkinerja baik di pasar bullish dan memiliki stabilitas yang tinggi.

Analisis Risiko

- Dalam kondisi pasar sideways, breakout palsu sering terjadi yang dapat menyebabkan kerugian.

- Pivot Point tidak sepenuhnya dapat menghindari breakout palsu; perlu dikombinasikan dengan lebih banyak indikator untuk menyaring sinyal.

- Keluar sebagian meningkatkan frekuensi transaksi dan juga biaya transaksi.

- Efektivitasnya tidak ideal di pasar bearish; perlu pengendalian risiko yang baik.

Arah Optimasi

- Dapat dikombinasikan dengan indikator lain seperti MACD, KDJ untuk membantu menyaring sinyal masuk dan keluar.

- Dapat mengoptimalkan panjang dan standar deviasi Bollinger Bands untuk menemukan kombinasi parameter optimal.

- Dapat memperkenalkan algoritma pembelajaran mesin untuk mengoptimalkan parameter Bollinger Bands secara dinamis.

- Dapat menguji berbagai level stop loss untuk menemukan titik stop loss yang optimal.

- Dapat menambahkan mekanisme keluar adaptif yang menyesuaikan target profit berdasarkan volatilitas pasar.

Kesimpulan

Secara keseluruhan, strategi ini adalah sistem breakout yang stabil. Metode operasinya yang terstandarisasi dan ruang optimasi parameter yang besar membuatnya cocok untuk perdagangan kuantitatif. Namun, perhatian juga perlu diberikan pada pengendalian risiko untuk mencegah kerugian akibat kondisi pasar yang tidak normal. Secara keseluruhan, ini adalah strategi breakout yang layak untuk dipelajari dan dioptimalkan secara berkelanjutan.

- 1