Strategi Bullish Indikator Tren Utama

Ringkasan

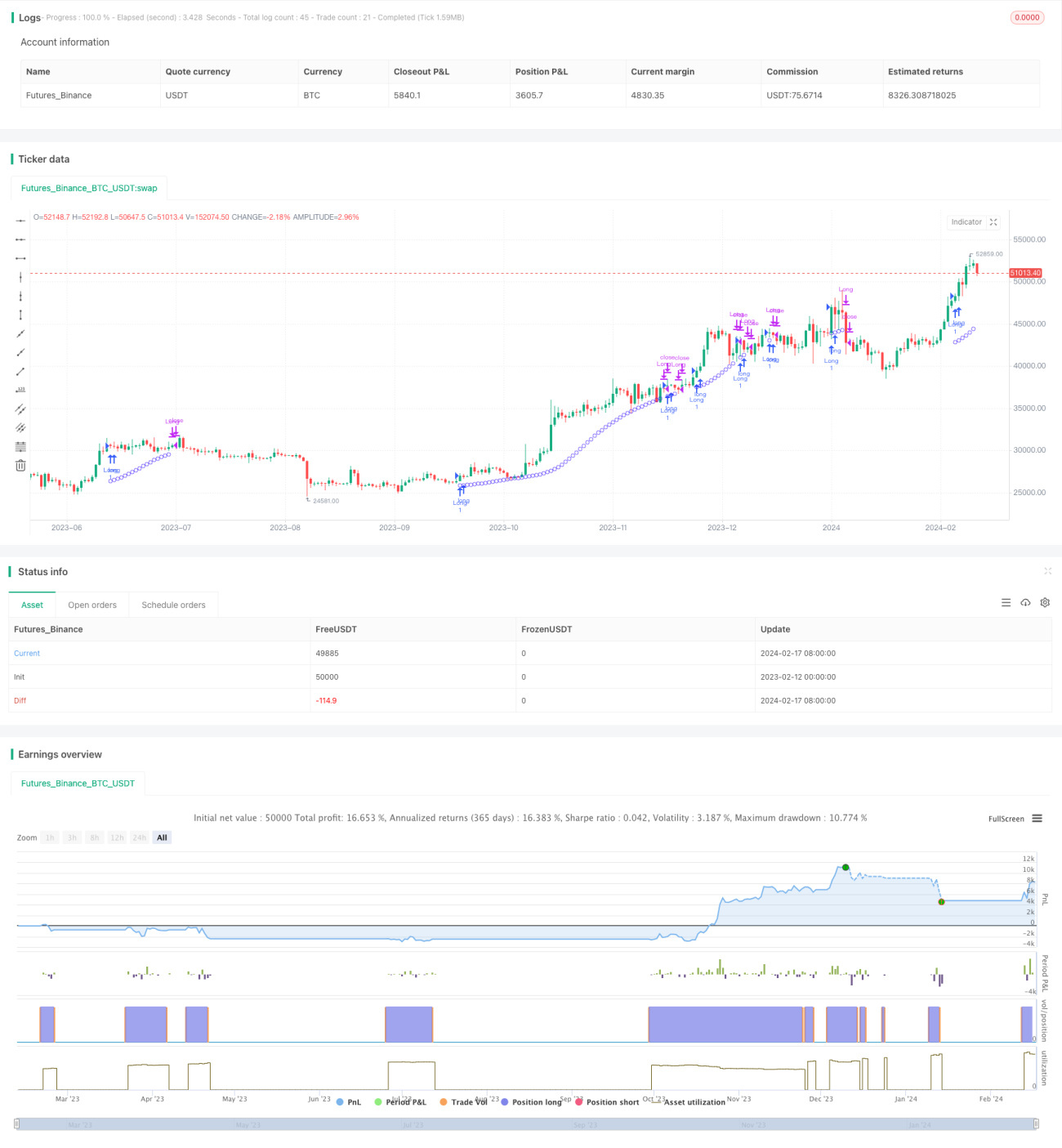

Strategi Indikator Tren Utama untuk Posisi Beli (Major Trend Indicator Long, disingkat MTIL) adalah strategi trading yang digunakan untuk berbagai instrumen keuangan (termasuk mata uang kripto Bitcoin, Ethereum, dan saham tradisional seperti Apple Inc.). Strategi ini dirancang untuk mengidentifikasi potensi tren naik guna membuka posisi beli jangka panjang.

Prinsip Strategi

Strategi MTIL menggunakan parameter yang dioptimalkan untuk menghitung harga tertinggi dan terendah dalam periode lookback tertentu. Kemudian metode regresi linier diterapkan untuk menghaluskan data harga, mengidentifikasi potensi tren bullish, dan menghasilkan sinyal beli.

Secara spesifik, strategi ini pertama-tama menghitung harga tertinggi dan terendah dalam periode tertentu. Kemudian menggunakan regresi linier dengan parameter berbeda untuk menghaluskan harga tertinggi dan terendah. Ini menghasilkan pita atas dan pita bawah. Ketika garis harga tertinggi yang dihaluskan menembus pita atas, dan garis harga terendah juga menembus pita bawah, serta regresi linier jangka pendek dari harga penutupan berada di atas regresi linier jangka panjang, maka sinyal bullish dihasilkan.

Analisis Keunggulan

Strategi MTIL memiliki keunggulan sebagai berikut:

- Menggunakan teknik penghalusan ganda untuk mengidentifikasi tren, dengan akurasi yang relatif tinggi

- Waktu mulai backtest dapat diatur, memudahkan pengujian kinerja historis strategi

- Parameter dapat disesuaikan sendiri untuk menyesuaikan preferensi trading masing-masing

- Dapat dikombinasikan dengan strategi short untuk analisis multi-timeframe

Analisis Risiko

Strategi MTIL juga memiliki risiko sebagai berikut:

- Risiko trading tren besar, memungkinkan kerugian yang membesar

- Pengaturan parameter yang tidak tepat dapat menyebabkan peluang terlewatkan atau sinyal palsu

- Perlu mempertimbangkan biaya trading dengan tepat, menghindari frekuensi trading yang terlalu tinggi

Beberapa risiko dapat dihindari dengan menyesuaikan parameter, memasang stop loss, mengendalikan biaya trading, dll.

Arah Optimasi

Strategi MTIL dapat dioptimalkan dari beberapa aspek berikut:

- Menguji kombinasi parameter periode yang berbeda untuk menemukan parameter optimal

- Menambahkan mekanisme konfirmasi volume-harga untuk menghindari sinyal palsu

- Menggabungkan indikator lain untuk menilai kekuatan dan pergerakan intraday guna mengonfirmasi sinyal lebih lanjut

- Menetapkan strategi stop loss dan take profit untuk mengontrol kerugian per perdagangan dan keuntungan keseluruhan

Kesimpulan

MTIL adalah strategi long yang menggunakan teknik regresi linier untuk mengidentifikasi tren utama. Strategi ini dapat disesuaikan dengan parameter untuk beradaptasi dengan kondisi pasar yang berbeda. Jika dikombinasikan dengan strategi short, dapat memberikan analisis yang lebih komprehensif. Setelah dioptimalkan dan disesuaikan, akurasi dan profitabilitasnya dapat ditingkatkan.

- 1