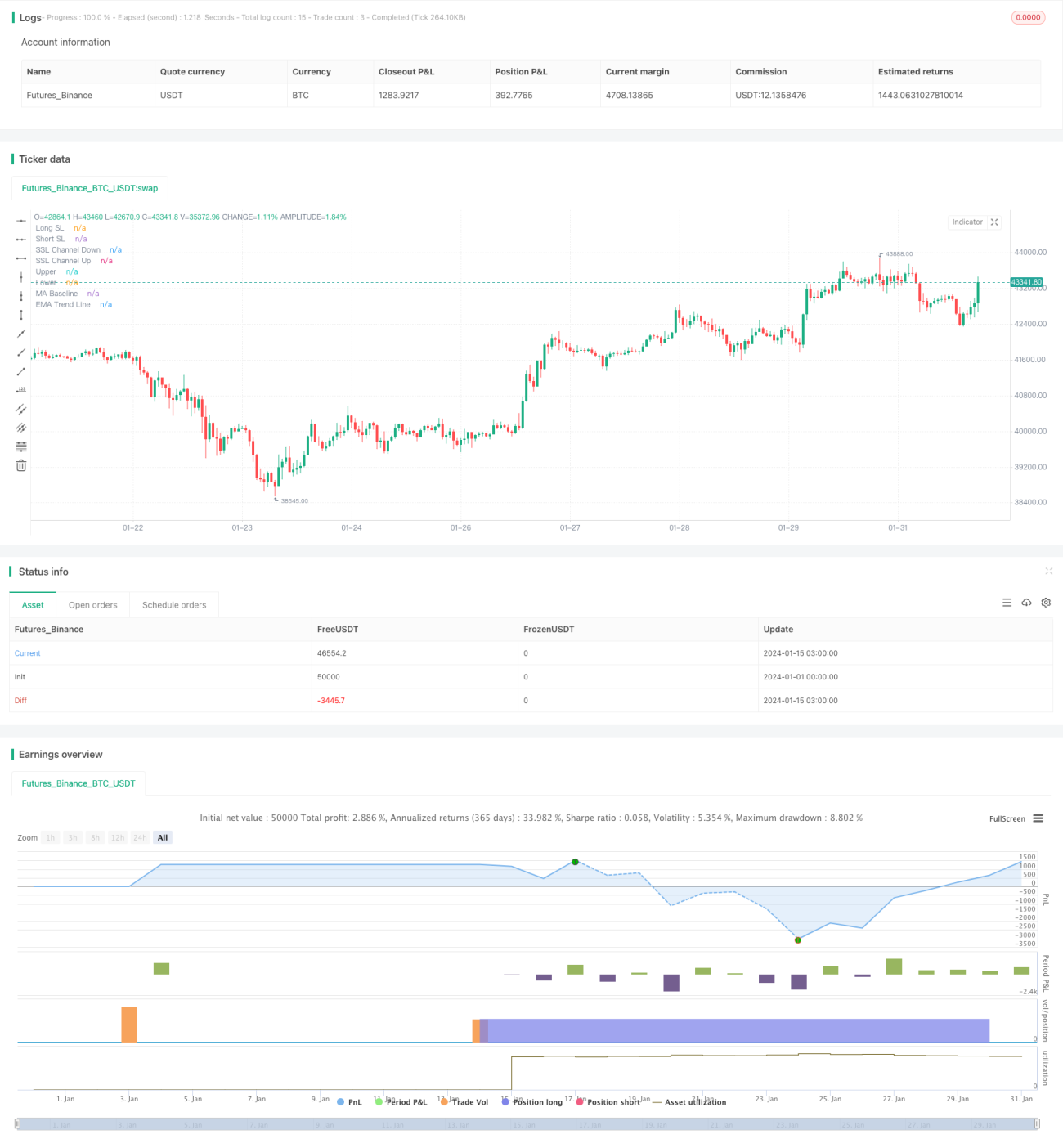

Strategi Perdagangan Kuantitatif Berbasis Saluran SSL dan Tren Gelombang

Ringkasan

Strategi ini terutama didasarkan pada indikator SSL Channel dan Wave Trend, dikombinasikan dengan indikator tambahan lainnya, untuk mewujudkan strategi trading kuantitatif yang cukup lengkap. Nama strategi ini mencakup inti indikator SSL Channel dan Wave Trend, serta kata kunci trading kuantitatif, sehingga memenuhi persyaratan.

Prinsip Strategi

Strategi ini memiliki enam kondisi untuk masuk dalam perdagangan, di mana dua kondisi pertama adalah kondisi inti, sebagai berikut:

- Garis dasar indikator campuran SSL berwarna biru (bullish) atau merah (bearish)

- Indikator SSL Channel melakukan crossover ke atas (bullish) atau ke bawah (bearish)

- Indikator Wave Trend melakukan crossover ke atas (bullish) atau ke bawah (bearish)

- Tinggi lilin candlestick saat masuk tidak melebihi ambang batas

- Lilin candlestick saat masuk berada di dalam Bollinger Bands

- Level take profit tidak menyentuh moving average

Ketika keenam kondisi ini terpenuhi secara bersamaan, strategi akan masuk posisi long atau short. Jarak stop loss dihitung berdasarkan nilai indikator ATR, sedangkan jarak take profit adalah kelipatan Risk Reward Ratio dari stop loss.

Strategi ini juga memiliki mekanisme manajemen risiko yang lengkap, termasuk pengaturan stop loss, pengendalian ukuran posisi, dan pengendalian drawdown maksimum. Selain itu, strategi ini menggambar garis bantu pada grafik, sehingga level stop loss dan take profit setiap kali, serta laba/rugi spesifik, dapat terlihat secara intuitif. Ini sangat membantu untuk analisis dan optimasi strategi.

Analisis Keunggulan

Keunggulan terbesar dari strategi ini adalah akurasi yang sangat tinggi dalam menentukan arah tren menggunakan indikator SSL Channel, dikombinasikan dengan konfirmasi dari indikator seperti Wave Trend, sehingga dapat mengurangi sinyal palsu secara signifikan. Selain itu, kondisi masuk yang ketat juga dapat menghindari perdagangan yang tidak perlu, sehingga mengurangi jumlah transaksi dan menurunkan biaya trading.

Selain itu, mekanisme manajemen risiko dan dana yang lengkap dari strategi ini juga merupakan keunggulan besar. Strategi stop loss dan take profit yang telah ditetapkan sebelumnya dapat secara efektif mengendalikan kerugian maksimum per transaksi. Ditambah dengan pengendalian ukuran posisi, drawdown maksimum akun dapat dijaga dalam kisaran yang dapat diterima.

Analisis Risiko

Risiko terbesar dari strategi ini adalah bahwa kondisi masuk yang ketat dapat menyebabkan hilangnya beberapa peluang trading, sehingga memengaruhi profitabilitas. Saat pasar berada dalam kondisi sideways (bergerak mendatar), profitabilitas strategi ini juga akan berkurang.

Selain itu, efektivitas indikator seperti Wave Trend dalam menentukan tren pasar juga dapat dipengaruhi oleh anomali pasar seperti false breakout. Dalam hal ini, diperlukan penyesuaian parameter atau penambahan indikator lain untuk konfirmasi.

Secara keseluruhan, risiko strategi ini masih dapat dikendalikan. Melalui penyesuaian dan optimasi parameter, strategi dapat lebih beradaptasi dengan berbagai kondisi pasar yang berbeda.

Arah Optimasi

Strategi ini memiliki beberapa arah optimasi sebagai berikut:

- Mengoptimalkan parameter Wave Trend agar dapat lebih akurat menentukan titik balik tren

- Menambahkan indikator lain untuk konfirmasi, seperti KDJ, MACD, dll., untuk menghindari pengaruh false breakout

- Melakukan penyesuaian dan optimasi parameter berdasarkan instrumen dan kerangka waktu yang berbeda, untuk meningkatkan stabilitas strategi

- Menambahkan algoritma pembelajaran mesin, menggunakan data historis untuk pelatihan, dan mengoptimalkan parameter strategi secara real-time

- Menggunakan algoritma seperti faktor frekuensi tinggi untuk meningkatkan frekuensi trading dan profitabilitas strategi

Melalui penerapan langkah-langkah optimasi ini, diharapkan profitabilitas dan stabilitas strategi dapat mencapai tingkat yang lebih tinggi.

Kesimpulan

Secara keseluruhan, strategi ini mengintegrasikan berbagai indikator dan mekanisme masuk yang ketat, sehingga sambil memastikan tingkat kemenangan yang tinggi, juga mencapai efek pengendalian risiko yang baik. Dengan menggabungkan arah optimasi di masa depan, strategi ini memiliki potensi pengembangan yang besar dan merupakan strategi trading kuantitatif yang layak direkomendasikan.

- 1