Strategi Perdagangan Multi-kerangka Waktu Berdasarkan Indikator Kompresi

Ikhtisar

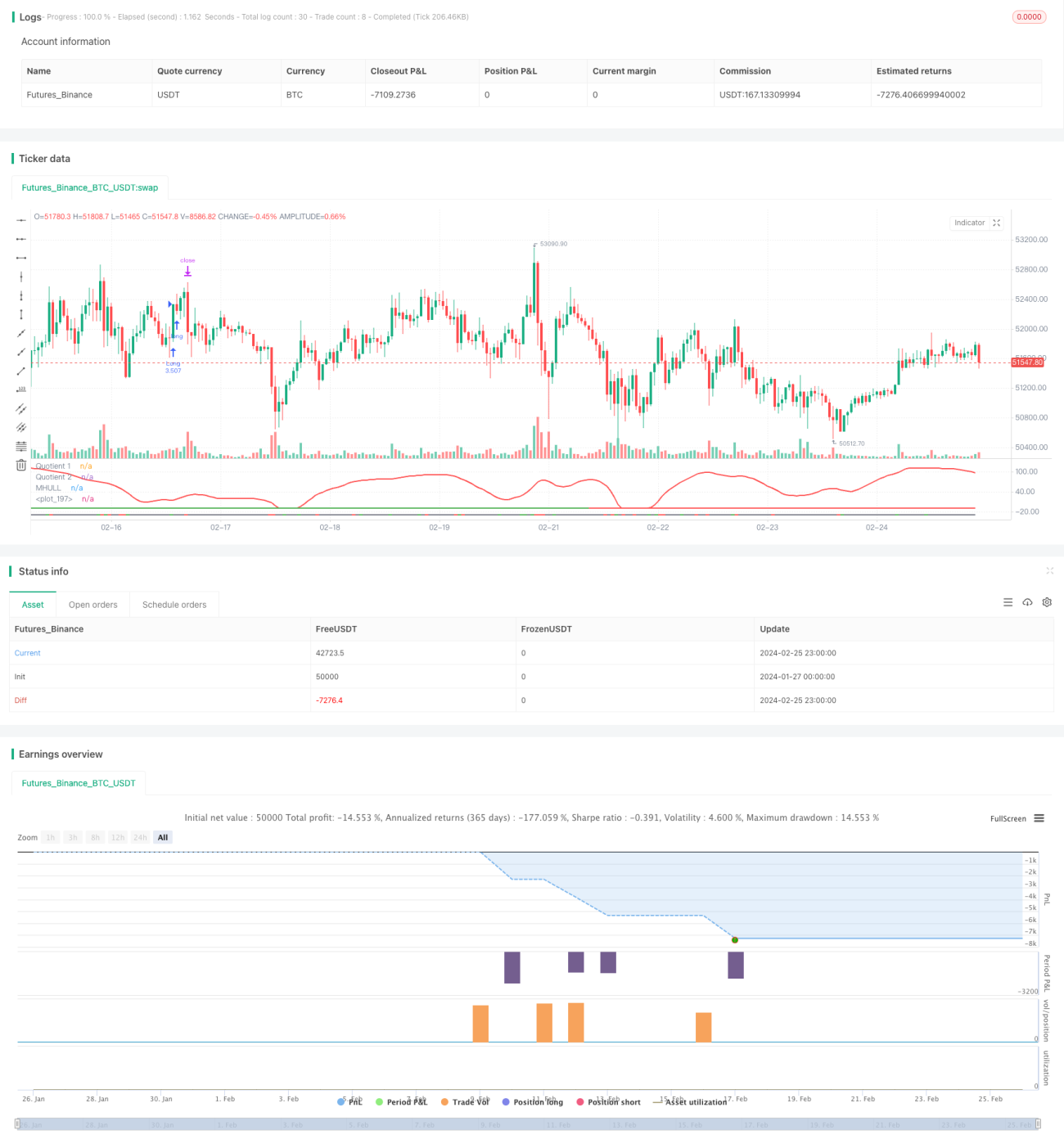

Strategi ini menggabungkan tiga indikator, yaitu Boom Hunter, Hull Suite, dan Volatility Oscillator, untuk mewujudkan strategi kuantitatif dalam melakukan trend following dan breakout trading di berbagai kerangka waktu. Strategi ini cocok untuk aset digital seperti Bitcoin yang memiliki volatilitas tinggi dan pergerakan harga yang tiba-tiba.

Prinsip

Logika inti strategi ini didasarkan pada tiga indikator berikut:

-

Boom Hunter: Sebuah osilator yang diimplementasikan menggunakan teknik kompresi indikator, dengan persilangan dua indikator (Quotient1 dan Quotient2) untuk menentukan sinyal beli dan jual.

-

Hull Suite: Sekelompok indikator moving average yang dihaluskan, yang menentukan arah tren melalui hubungan antara pita tengah dan pita atas/bawah.

-

Volatility Oscillator: Sebuah indikator osilator yang mengkuantifikasi informasi volatilitas harga.

Logika entry strategi ini adalah, pada saat dua indikator Quotient dari Boom Hunter mengalami persilangan ke atas atau ke bawah, harga harus menembus pita tengah Hull dan mengalami divergensi dengan pita atas atau pita bawah, sementara itu indikator Volatility berada di zona overbought atau oversold. Hal ini dapat menyaring sinyal breakout palsu dan meningkatkan akurasi entry.

Stop loss ditetapkan dengan mencari lembah terendah atau puncak tertinggi dalam periode tertentu (default 20 lilin). Profit diperoleh dengan mengalikan persentase stop loss dengan rasio take profit yang dikonfigurasi (default 3 kali). Ukuran posisi dihitung berdasarkan persentase total aset akun (default 3%) dan besaran stop loss dari instrumen tertentu.

Keunggulan

- Memanfaatkan teknik indikator kompresi untuk mengekstrak sinyal perdagangan utama dari harga, meningkatkan probabilitas keuntungan.

- Verifikasi kombinasi multi-indikator, menghindari breakout palsu, menentukan arah tren secara akurat.

- Pengaturan stop loss dan take profit dinamis, mewujudkan trend following dengan risiko terkendali.

- Menggunakan indikator volatilitas untuk memastikan perdagangan di lingkungan volatilitas tinggi.

- Analisis multi-kerangka waktu, meningkatkan stabilitas strategi.

Risiko

- Indikator Boom Hunter mungkin mengalami distorsi kompresi, menyebabkan sinyal yang salah.

- Pita tengah Hull Suite memiliki lag, tidak dapat melacak perubahan harga secara tepat waktu.

- Ketika volatilitas menurun, dapat melewatkan peluang trading atau memicu likuidasi rugi.

Solusi:

- Sesuaikan parameter indikator kompresi untuk menyeimbangkan sensitivitas indikator.

- Coba gunakan moving average eksponensial seperti EHMA untuk menggantikan indikator pita tengah.

- Tambahkan indikator penilaian lainnya untuk menghindari kesesatan volatilitas.

Optimasi

Strategi ini dapat dioptimalkan dari beberapa aspek berikut:

-

Optimasi Parameter: Dengan mengubah parameter indikator seperti panjang periode, koefisien kompresi, dll., untuk mendapatkan kombinasi parameter terbaik.

-

Optimasi Kerangka Waktu: Menguji berbagai periode waktu (1 menit, 5 menit, 30 menit, dll.) untuk menemukan siklus trading yang paling sesuai.

-

Optimasi Posisi: Mengubah ukuran dan rasio posisi setiap trading untuk menemukan skema pemanfaatan dana yang optimal.

-

Optimasi Stop Loss: Menyesuaikan posisi stop loss berdasarkan pasangan trading yang berbeda untuk mencapai rasio risk-reward terbaik.

-

Optimasi Kondisi: Menambah atau mengurangi kondisi penyaringan indikator untuk mendapatkan waktu entry yang lebih akurat.

Kesimpulan

Strategi ini, melalui kombinasi penggunaan tiga indikator yaitu Boom Hunter, Hull Suite, dan Volatility Oscillator, mewujudkan perdagangan trend following di multi-kerangka waktu, mampu mengidentifikasi perilaku harga yang tiba-tiba secara efektif, dan cocok untuk aset digital dengan volatilitas tinggi. Strategi ini memiliki risiko yang terkendali, dan melalui optimasi parameter, kondisi penyaringan, serta stop loss dari berbagai aspek, memiliki kepraktisan dan skalabilitas yang kuat.

- 1