Strategi perdagangan kombinasi penembusan penutupan tiga pita Bollinger dengan indikator RSI

Gambaran Umum

Strategi ini menghasilkan sinyal trading dengan menggabungkan indikator Bollinger Bands dan Relative Strength Index (RSI). Strategi ini memantau apakah harga penutupan dari tiga lilin secara bersamaan menembus pita atas atau bawah, dan mengonfirmasi sinyal trading dengan indikator turbo dan RSI.

Prinsip Strategi

Strategi ini terutama didasarkan pada prinsip-prinsip berikut:

- Menggunakan Bollinger Bands dengan panjang 20. Ketika harga penutupan menembus pita atas atau bawah, sinyal trading dipertimbangkan.

- Mensyaratkan harga penutupan tiga lilin secara bersamaan menembus untuk menghindari sinyal palsu.

- Menggabungkan indikator turbo: VIP>1,25 saat overbought kuat, VIM>1,25 saat oversold kuat, untuk menyaring sinyal.

- Menggabungkan RSI untuk menentukan overbought/oversold. RSI menembus 70 dipertimbangkan untuk short, RSI menembus 30 dipertimbangkan untuk long.

- Ketika kondisi di atas terpenuhi, sinyal long atau short dihasilkan.

Analisis Keunggulan

Strategi ini memiliki keunggulan utama sebagai berikut:

- Triple BB bands menyaring sinyal palsu, memastikan keandalan penembusan.

- Indikator turbo menilai kekuatan pasar, menghindari trading dalam kondisi pasar yang tidak menguntungkan.

- RSI menentukan area overbought/oversold, dikombinasikan dengan Bollinger Bands untuk entry.

- Kombinasi berbagai indikator, penilaian komprehensif terhadap kondisi pasar, keandalan sinyal cukup tinggi.

Analisis Risiko

Strategi ini juga memiliki beberapa risiko:

- Bollinger Bands sangat sensitif terhadap parameter, perlu dioptimalkan panjang dan kelipatan StdDev.

- Indikator turbo juga sensitif terhadap parameter periode, perlu disesuaikan untuk pasar yang berbeda.

- RSI rentan terhadap divergensi, juga dapat melewatkan tren.

- Jika ketiga indikator menghasilkan penilaian yang berbeda, tidak dapat masuk, sehingga melewatkan beberapa peluang.

Langkah-langkah pengendalian risiko meliputi:

- Optimasi parameter, uji parameter dengan rasio kemenangan tertinggi.

- Menggabungkan indikator lain, misalnya penyaringan volume.

- Melonggarkan logika penilaian indikator secara tepat untuk mencegah kehilangan peluang.

Arah Optimasi

Strategi ini dapat dioptimasi dari beberapa aspek berikut:

- Optimasi panjang dan kelipatan StdDev Bollinger Bands untuk menemukan parameter terbaik.

- Optimasi periode indikator turbo agar lebih sesuai dengan pasar yang berbeda.

- Menambahkan penilaian indikator lain, misalnya volume, MACD, dll., untuk memperkaya diversifikasi sinyal.

- Menyesuaikan logika penilaian indikator untuk mencegah ketidaksepakatan yang menyebabkan tidak bisa masuk.

- Menambahkan strategi stop loss untuk mengendalikan kerugian maksimum per transaksi.

Kesimpulan

Strategi ini menggunakan kombinasi berbagai indikator untuk penilaian. Meskipun memastikan keandalan sinyal, juga memiliki beberapa masalah. Melalui optimasi parameter, memperkaya sumber sinyal, menyesuaikan logika penilaian, dan stop loss, stabilitas dan profitabilitas strategi dapat lebih ditingkatkan. Ini memberikan ide yang baik untuk trading kuantitatif.

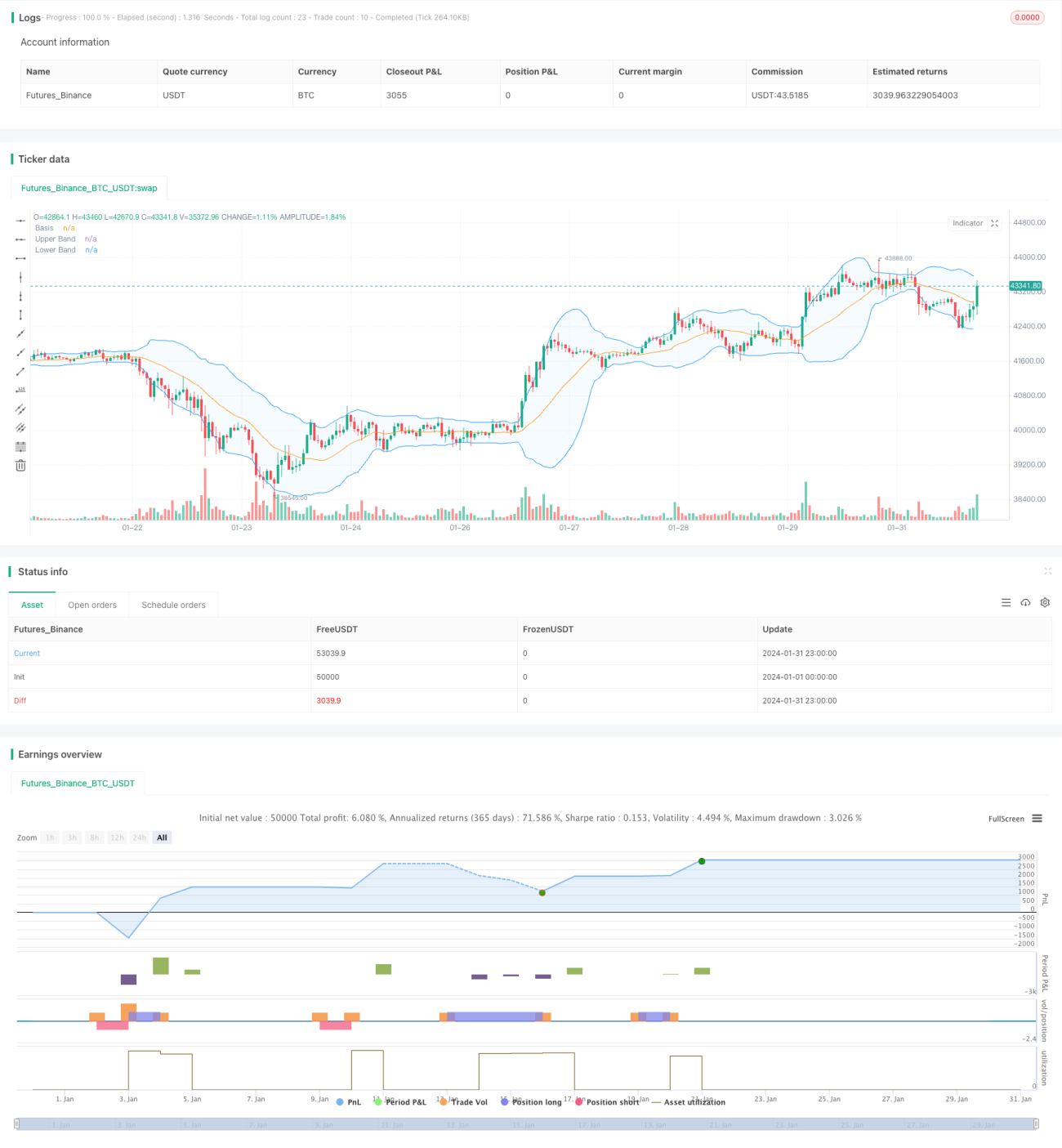

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Noway0utstorm

//@version=5- 1