Strategi Take Profit dan Stop Loss Dinamis untuk Long dan Short Berdasarkan VWAP dan Sinyal Lintas Periode

Gambaran Umum

Strategi ini menggunakan VWAP (Volume Weighted Average Price) harian sebagai sinyal masuk dan keluar. Ketika harga penutupan menembus ke atas VWAP, sinyal long diaktifkan, stop loss ditempatkan di bawah VWAP pada low candle sebelumnya, target harga ditetapkan 3 poin di atas harga buka. Ketika harga penutupan menembus ke bawah VWAP, sinyal short diaktifkan, stop loss ditempatkan di atas VWAP pada high candle sebelumnya, target harga ditetapkan 3 poin di bawah harga buka. Strategi ini tidak memiliki kondisi keluar, perdagangan akan terus dipegang sampai sinyal sebaliknya muncul.

Prinsip Strategi

- Mendapatkan data VWAP harian sebagai dasar penentuan tren dan sinyal perdagangan.

- Memeriksa apakah harga penutupan saat ini menembus ke atas/ke bawah VWAP, masing-masing sebagai kondisi pemicu untuk long dan short.

- Saat long, jika low candle sebelumnya berada di bawah VWAP, maka digunakan sebagai level stop loss, jika tidak, langsung menggunakan VWAP sebagai stop loss; untuk short berlaku sebaliknya.

- Setelah posisi dibuka, menetapkan target take profit tetap sebesar 3 poin.

- Strategi berjalan terus menerus hingga sinyal sebaliknya memicu penutupan posisi dan pembukaan posisi baru.

Dengan menggunakan data VWAP lintas kerangka waktu untuk menentukan tren, serta memanfaatkan stop loss dinamis dan take profit tetap, strategi ini dapat secara efektif menangkap pergerakan tren, mengendalikan risiko drawdown, dan mengunci keuntungan tepat waktu.

Analisis Keunggulan

- Sederhana dan efektif: Logika strategi jelas, hanya menggunakan satu indikator VWAP untuk menentukan tren dan memicu sinyal, mudah diimplementasikan dan dioptimalkan.

- Stop loss dinamis: Menggunakan high/low candle sebelumnya untuk menempatkan stop loss, lebih mampu beradaptasi dengan fluktuasi pasar, mengurangi risiko.

- Take profit tetap: Menetapkan target harga dengan jumlah poin tetap, membantu mengunci keuntungan tepat waktu dan menghindari pengembalian laba.

- Stop loss dan take profit tepat waktu: Strategi segera menutup posisi ketika sinyal sebaliknya muncul, tidak menyebabkan kerugian tambahan pada laba yang ada, sekaligus membuka posisi baru untuk menangkap tren baru.

Analisis Risiko

- Optimasi parameter: Strategi menggunakan 3 poin tetap sebagai take profit. Dalam perdagangan nyata, perlu dioptimalkan sesuai dengan instrumen dan karakteristik pasar yang berbeda untuk memilih parameter terbaik.

- Pasar sideways: Dalam kondisi pasar sideways, seringnya masuk dan keluar dapat menyebabkan biaya transaksi yang tinggi, mempengaruhi keuntungan.

- Keberlanjutan tren: Strategi bergantung pada pergerakan tren. Jika pasar berada dalam kisaran atau tren tidak berkelanjutan, mungkin muncul banyak sinyal perdagangan yang membawa risiko lebih besar.

Arah Optimasi

- Filter tren: Menambahkan indikator tren lain seperti moving average, MACD, dll. untuk konfirmasi sekunder terhadap tren, meningkatkan keandalan sinyal.

- Take profit dinamis: Menyesuaikan jumlah poin take profit secara dinamis berdasarkan volatilitas pasar, indikator ATR, dll., agar lebih sesuai dengan pasar.

- Manajemen posisi: Menyesuaikan ukuran posisi setiap perdagangan secara dinamis berdasarkan modal akun, toleransi risiko, dll.

- Pemilihan sesi perdagangan: Memilih sesi perdagangan terbaik berdasarkan karakteristik instrumen dan tingkat aktivitas perdagangan untuk meningkatkan efisiensi strategi.

Kesimpulan

Strategi ini menggunakan data VWAP lintas kerangka waktu untuk menentukan tren dan memicu sinyal, serta menerapkan stop loss dinamis dan take profit tetap untuk mengendalikan risiko dan mengunci keuntungan. Ini adalah strategi perdagangan kuantitatif yang sederhana dan efektif. Melalui optimasi filter tren, take profit dinamis, manajemen posisi, dan pemilihan sesi perdagangan, stabilitas dan potensi keuntungan strategi dapat lebih ditingkatkan. Namun, dalam penerapan nyata, perlu memperhatikan karakteristik pasar, biaya transaksi, dan optimasi parameter untuk mendapatkan kinerja strategi yang lebih baik.

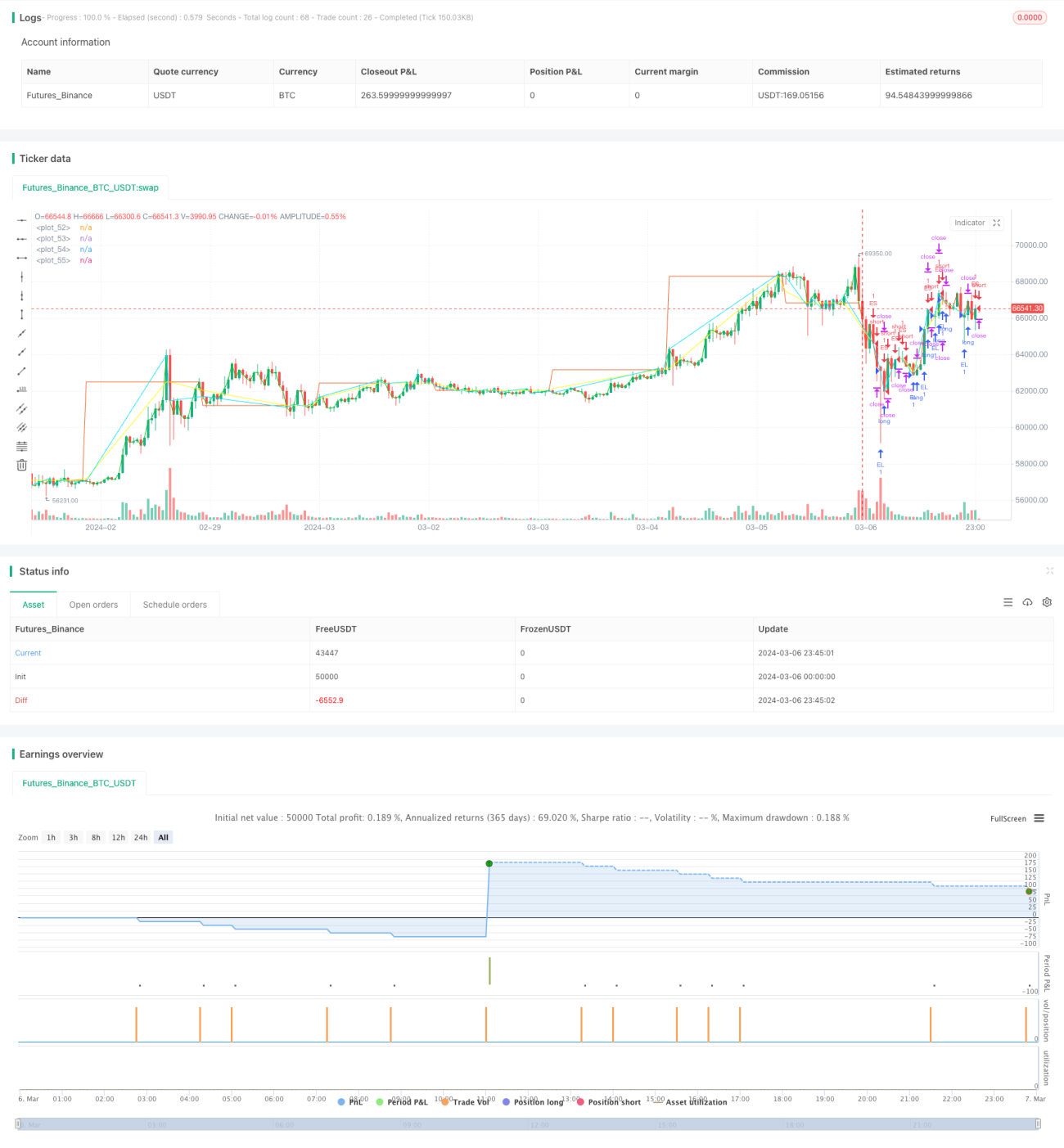

/*backtest

start: 2024-03-06 00:00:00

end: 2024-03-07 00:00:00

period: 45m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy('Pine Script Tutorial Example Strategy 1', overlay=true, initial_capital=1000, default_qty_value=100, default_qty_type=strategy.percent_of_equity)

// fastEMA = ta.ema(close, 24)

// slowEMA = ta.ema(close, 200)- 1