Gambaran Umum

Strategi ini menggunakan beberapa rata-rata bergerak (VWMA), Indeks Arah Rata-rata (ADX), dan Indikator Pergerakan Arah (DMI) untuk menangkap peluang beli di pasar Bitcoin. Dengan menggabungkan momentum harga, arah tren, dan volume perdagangan, strategi ini bertujuan menemukan titik masuk dengan tren naik yang kuat dan momentum yang mencukupi, sembari mengendalikan risiko secara ketat.

Prinsip Strategi

- Menggunakan VWMA 9 hari dan 14 hari untuk menentukan tren naik; sinyal beli muncul ketika rata-rata bergerak jangka pendek melintasi di atas rata-rata bergerak jangka panjang.

- Memperkenalkan rata-rata bergerak adaptif yang dibangun dari VWMA harga tertinggi dan terendah 89 hari sebagai filter tren; posisi hanya dipertimbangkan jika harga penutupan atau pembukaan berada di atas rata-rata bergerak tersebut.

- Menggunakan indikator ADX dan DMI untuk mengonfirmasi kekuatan tren; transaksi hanya dianggap cukup kuat jika ADX lebih besar dari 18 dan selisih antara +DI dan -DI lebih besar dari 15.

- Menggunakan fungsi persentil volume untuk memfilter bar dengan volume antara 60% hingga 95%, menghindari periode volume rendah.

- Menetapkan stop loss pada 0,96–0,99 kali harga tertinggi candle sebelumnya, yang menurun seiring bertambahnya kerangka waktu, guna mengendalikan risiko.

- Menutup posisi ketika waktu penahanan yang telah ditentukan tercapai atau harga turun di bawah rata-rata bergerak adaptif.

Analisis Keunggulan

- Menggabungkan beberapa indikator teknis untuk mengevaluasi kondisi pasar dari berbagai dimensi seperti tren, momentum, dan volume, sehingga sinyal lebih andal.

- Rata-rata bergerak adaptif dan mekanisme filter volume secara efektif menyaring sinyal palsu, mengurangi transaksi yang tidak efektif.

- Penetapan stop loss yang ketat dan batasan waktu penahanan secara signifikan mengurangi eksposur risiko strategi.

- Desain kode modular, mudah dibaca dan dipelihara, serta memudahkan optimasi dan pengembangan lebih lanjut.

Analisis Risiko

- Saat pasar bergerak sideways atau tren tidak jelas, strategi ini dapat menghasilkan banyak sinyal palsu.

- Stop loss relatif dekat, sehingga dapat terpicu terlalu dini saat volatilitas tinggi, menyebabkan kerugian yang lebih besar.

- Kurang mempertimbangkan kondisi ekonomi makro dan peristiwa besar; strategi mungkin gagal saat menghadapi peristiwa "black swan".

- Parameter relatif tetap, kurang adaptif, sehingga kinerja dapat tidak stabil di berbagai kondisi pasar.

Arah Optimasi

- Memperkenalkan lebih banyak indikator yang menggambarkan kondisi pasar, seperti Relative Strength Index (RSI), Bollinger Bands, untuk meningkatkan keandalan sinyal.

- Mengoptimalkan posisi stop loss secara dinamis, misalnya menggunakan ATR atau persentase stop loss, untuk beradaptasi dengan volatilitas pasar yang berbeda.

- Menggabungkan data ekonomi makro dan analisis sentimen untuk memperkuat modul pengendalian risiko strategi.

- Menggunakan algoritma pembelajaran mesin untuk mengoptimalkan parameter secara otomatis, meningkatkan adaptabilitas dan stabilitas strategi.

Kesimpulan

Strategi long Bitcoin VWMA-ADX, dengan mempertimbangkan berbagai indikator teknis seperti tren harga, momentum, dan volume, mampu menangkap peluang kenaikan di pasar Bitcoin secara efektif. Selain itu, langkah-langkah pengendalian risiko yang ketat dan kondisi penutupan posisi yang jelas membuat risiko strategi ini terkendali dengan baik. Namun, strategi ini juga memiliki beberapa keterbatasan, seperti kurangnya adaptasi terhadap perubahan kondisi pasar dan perlunya optimalisasi strategi stop loss. Ke depannya, strategi ini dapat ditingkatkan dari segi keandalan sinyal, pengendalian risiko, dan optimalisasi parameter untuk meningkatkan ketangguhan dan profitabilitas. Secara keseluruhan, strategi long Bitcoin VWMA-ADX memberikan pendekatan perdagangan sistematis berbasis momentum dan tren bagi investor, yang layak untuk dieksplorasi dan disempurnakan lebih lanjut.

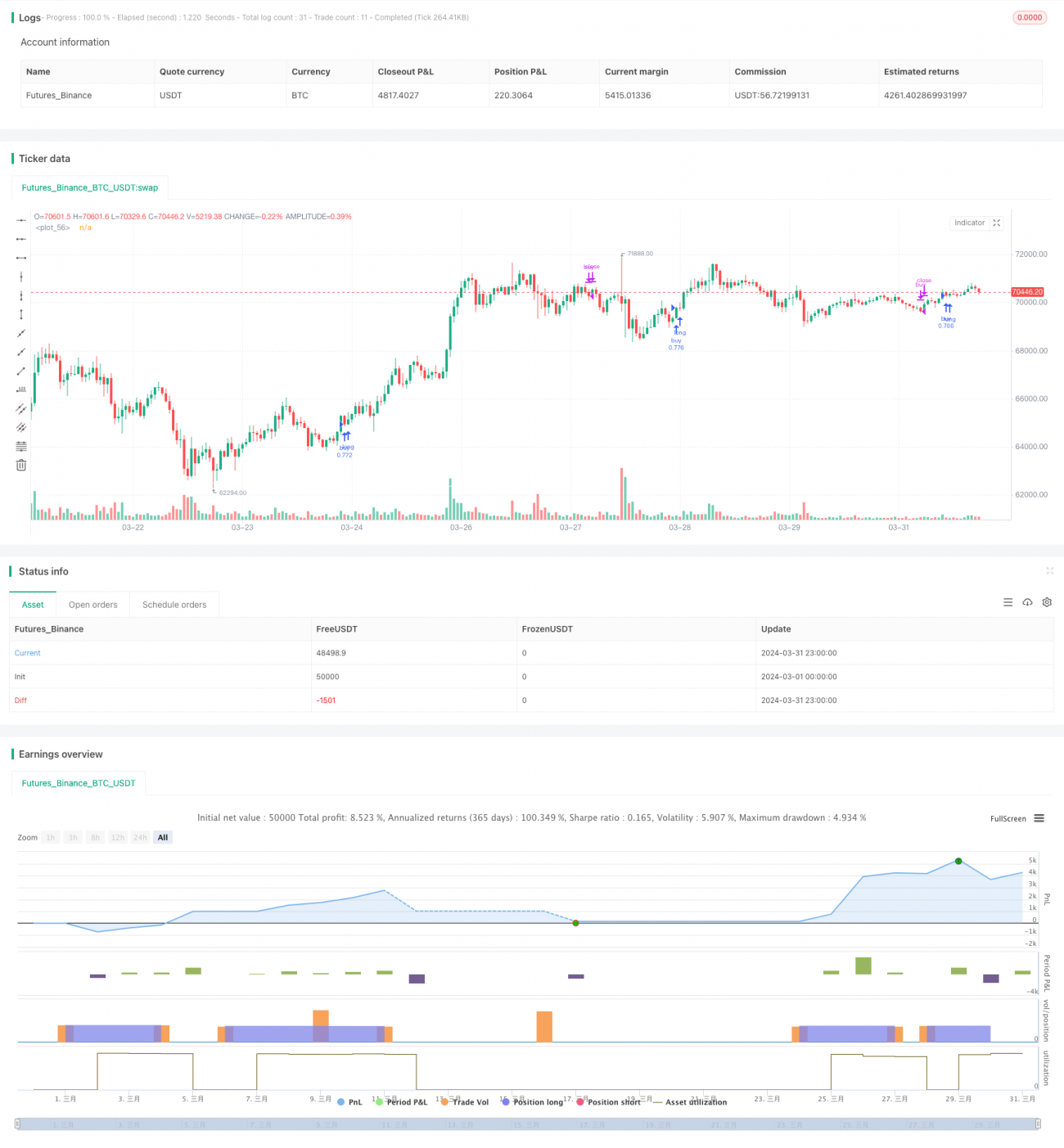

/*backtest

start: 2024-03-01 00:00:00

end: 2024-03-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Q_D_Nam_N_96

//@version=5

- 1