Strategi Penolakan Rata-Rata Bergerak Berdasarkan Filter Indeks Arah Rata-Rata

Ikhtisar

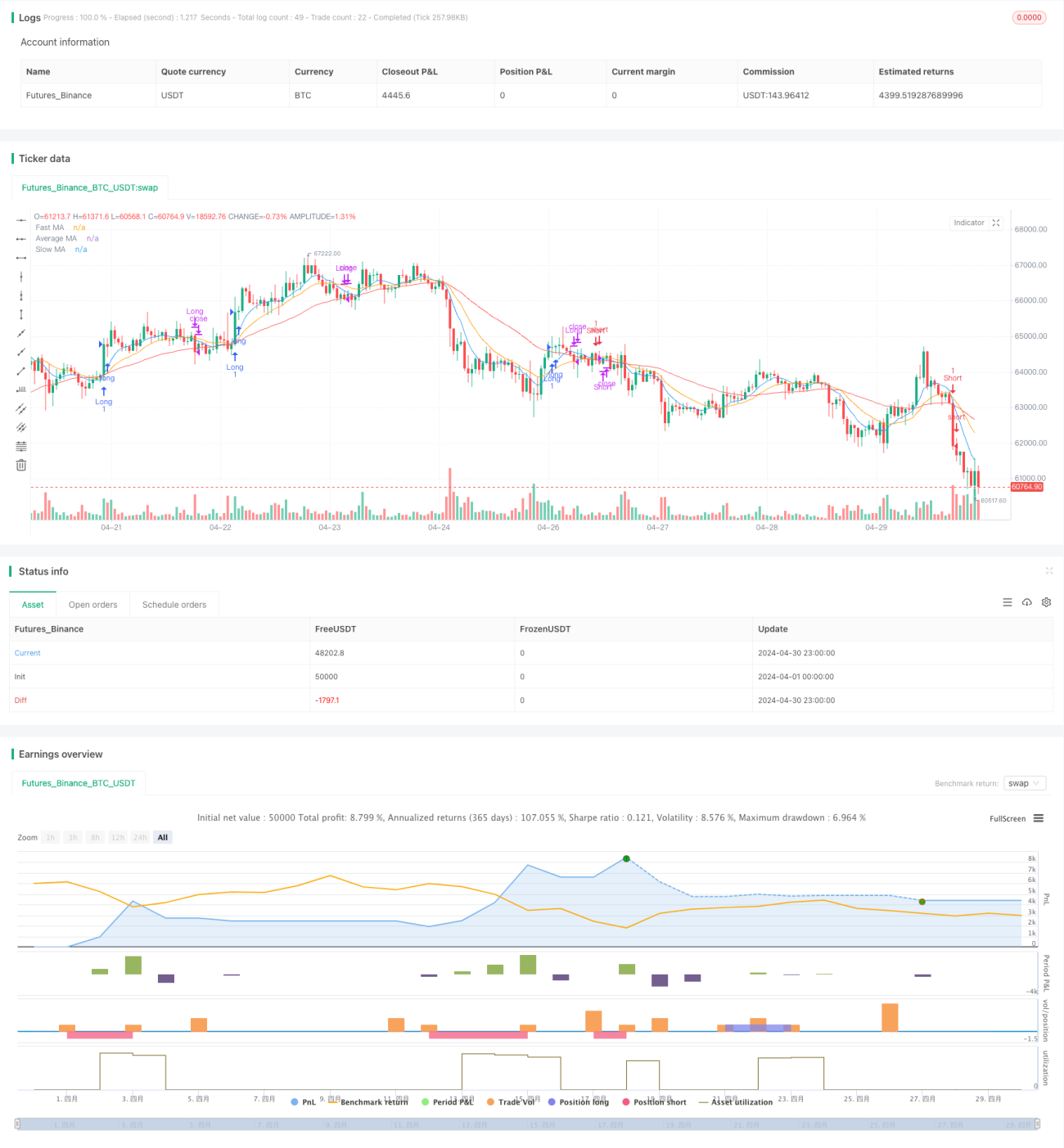

Strategi ini menggunakan beberapa moving average (MA) sebagai sinyal perdagangan utama, dan menggabungkan Average Directional Index (ADX) sebagai filter. Ide utama strategi adalah membandingkan hubungan antara MA cepat, MA lambat, dan MA rata-rata untuk mengidentifikasi potensi peluang long dan short. Pada saat yang sama, indikator ADX digunakan untuk menyaring kondisi pasar dengan kekuatan tren yang cukup, guna meningkatkan keandalan sinyal perdagangan.

Prinsip Strategi

- Hitung MA cepat, MA lambat, dan MA rata-rata.

- Bandingkan harga penutupan dengan MA lambat untuk mengidentifikasi level potensial long dan short.

- Bandingkan harga penutupan dengan MA cepat untuk mengonfirmasi level long dan short.

- Hitung indikator ADX secara manual untuk mengukur kekuatan tren.

- Ketika MA cepat memotong ke atas MA rata-rata, ADX lebih besar dari ambang batas yang ditetapkan, dan level long terkonfirmasi, maka muncul sinyal masuk long.

- Ketika MA cepat memotong ke bawah MA rata-rata, ADX lebih besar dari ambang batas yang ditetapkan, dan level short terkonfirmasi, maka muncul sinyal masuk short.

- Ketika harga penutupan memotong ke bawah MA lambat, maka muncul sinyal keluar long; ketika harga penutupan memotong ke atas MA lambat, maka muncul sinyal keluar short.

Keunggulan Strategi

- Menggunakan beberapa MA dapat menangkap perubahan tren dan momentum pasar secara lebih komprehensif.

- Dengan membandingkan hubungan antara MA cepat, MA lambat, dan MA rata-rata, dapat mengidentifikasi peluang perdagangan potensial.

- Menggunakan indikator ADX sebagai filter dapat menghindari terlalu banyak sinyal palsu di pasar yang bergerak sideways, sehingga meningkatkan keandalan sinyal perdagangan.

- Logika strategi jelas, mudah dipahami dan diimplementasikan.

Risiko Strategi

- Dalam kondisi tren yang tidak jelas atau pasar yang bergerak sideways, strategi ini dapat menghasilkan banyak sinyal palsu, menyebabkan frekuensi perdagangan tinggi dan kerugian.

- Strategi bergantung pada indikator lagging seperti MA dan ADX, yang mungkin melewatkan peluang pembentukan tren awal.

- Pengaturan parameter strategi (seperti panjang MA dan ambang batas ADX) memiliki dampak besar pada kinerja strategi, sehingga perlu dioptimalkan untuk pasar dan instrumen yang berbeda.

Arah Optimasi Strategi

- Pertimbangkan untuk memperkenalkan indikator teknis lain seperti RSI, MACD, dll., untuk meningkatkan keandalan dan keragaman sinyal perdagangan.

- Untuk kondisi pasar yang berbeda, dapat diatur kombinasi parameter yang berbeda untuk beradaptasi dengan perubahan pasar.

- Perkenalkan langkah-langkah manajemen risiko seperti stop loss dan pengelolaan posisi untuk mengendalikan potensi kerugian.

- Gabungkan analisis fundamental seperti data ekonomi, perubahan kebijakan, dll., untuk mendapatkan perspektif pasar yang lebih komprehensif.

Kesimpulan

Strategi Penolakan Rata-Rata Bergerak Berbasis Filter Indeks Arah Rata-Rata menggunakan beberapa MA dan indikator ADX untuk mengidentifikasi peluang perdagangan potensial dan menyaring sinyal perdagangan berkualitas rendah. Logika strategi ini jelas, mudah dipahami dan diimplementasikan, namun dalam aplikasi praktis perlu memperhatikan perubahan kondisi pasar, serta dioptimalkan dengan menggabungkan indikator teknis lain dan langkah-langkah manajemen risiko.

- 1