Strategi Penyesuaian Dinamis Take Profit dan Stop Loss Williams %R

Gambaran Umum

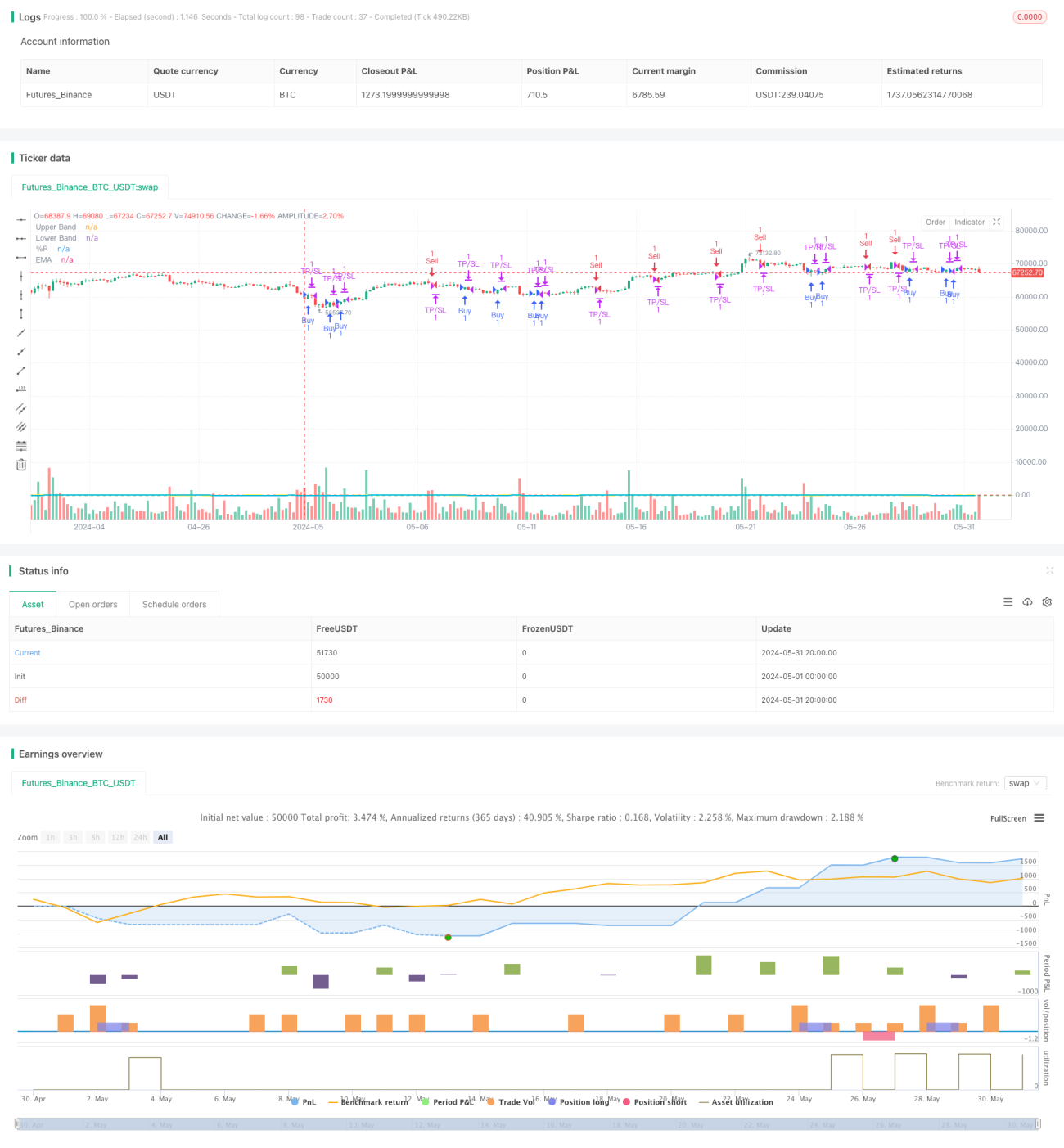

Strategi ini didasarkan pada indikator Williams %R, dengan menyesuaikan level take profit dan stop loss secara dinamis untuk mengoptimalkan kinerja perdagangan. Sinyal beli dihasilkan ketika Williams %R menembus zona oversold (-80), dan sinyal jual dihasilkan ketika menembus zona overbought (-20). Exponential Moving Average (EMA) digunakan untuk menghaluskan nilai Williams %R guna mengurangi noise. Strategi ini menyediakan pengaturan parameter yang fleksibel, termasuk periode indikator, level take profit/stop loss (TP/SL), waktu perdagangan, dan arah perdagangan, sehingga dapat beradaptasi dengan berbagai kondisi pasar dan preferensi trader.

Prinsip Strategi

- Hitung nilai Williams %R untuk periode yang ditentukan.

- Hitung Exponential Moving Average (EMA) dari Williams %R.

- Ketika Williams %R menembus level -80 dari bawah ke atas, sinyal beli dipicu; ketika menembus level -20 dari atas ke bawah, sinyal jual dipicu.

- Setelah posisi beli, atur level take profit dan stop loss, dan tutup posisi hanya jika mencapai level TP/SL atau Williams %R menghasilkan sinyal kebalikan.

- Setelah posisi jual, atur level take profit dan stop loss, dan tutup posisi hanya jika mencapai level TP/SL atau Williams %R menghasilkan sinyal kebalikan.

- Dapat memilih untuk melakukan transaksi dalam rentang waktu tertentu (misalnya 09:00-11:00) dan apakah akan melakukan transaksi di sekitar jam penuh (X menit sebelumnya hingga Y menit sesudahnya).

- Dapat memilih arah perdagangan: hanya long, hanya short, atau dua arah.

Analisis Keunggulan

- Take Profit dan Stop Loss Dinamis: Menyesuaikan level TP/SL secara dinamis berdasarkan pengaturan pengguna, dapat melindungi keuntungan dan mengontrol risiko dengan lebih baik.

- Parameter Fleksibel: Pengguna dapat mengatur berbagai parameter sesuai preferensi, seperti periode indikator, level TP/SL, waktu perdagangan, dll., untuk beradaptasi dengan kondisi pasar yang berbeda.

- Indikator yang Dihaluskan: Memasukkan EMA untuk menghaluskan nilai Williams %R dapat secara efektif mengurangi noise indikator dan meningkatkan keandalan sinyal.

- Pembatasan Waktu Perdagangan: Dapat memilih untuk bertransaksi dalam rentang waktu tertentu, menghindari periode volatilitas tinggi, sehingga mengurangi risiko.

- Arah Perdagangan Kustom: Dapat memilih hanya long, hanya short, atau kedua arah berdasarkan tren pasar dan penilaian pribadi.

Analisis Risiko

- Pengaturan Parameter Tidak Tepat: Jika level TP/SL terlalu longgar atau terlalu ketat, dapat menyebabkan kerugian laba atau seringnya stop loss.

- Kesalahan Identifikasi Tren: Indikator Williams %R berkinerja kurang baik di pasar sideway (ranging), dapat menghasilkan sinyal palsu.

- Efek Pembatasan Waktu Terbatas: Membatasi waktu perdagangan dapat menyebabkan strategi melewatkan beberapa peluang bagus.

- Over-optimasi: Over-optimasi parameter dapat menyebabkan kinerja strategi buruk dalam perdagangan nyata di masa depan.

Arah Optimasi

- Menggabungkan Indikator Lain: Seperti indikator tren, indikator volatilitas, dll., untuk meningkatkan akurasi konfirmasi sinyal.

- Optimasi Parameter Dinamis: Menyesuaikan parameter secara real-time sesuai kondisi pasar, seperti menggunakan pengaturan berbeda di pasar tren dan pasar sideway.

- Perbaikan Metode TP/SL: Menggunakan trailing stop, partial take profit, dll., untuk melindungi keuntungan dan mengontrol risiko dengan lebih baik.

- Menambahkan Manajemen Modal: Menyesuaikan ukuran posisi setiap transaksi secara dinamis berdasarkan saldo akun dan toleransi risiko.

Ringkasan

Strategi Williams %R dengan penyesuaian dinamis take profit dan stop loss menangkap kondisi overbought/oversold harga dengan cara yang sederhana namun efektif, sambil menyediakan pengaturan parameter yang fleksibel untuk beradaptasi dengan berbagai lingkungan pasar dan gaya trading. Strategi ini menyesuaikan level TP/SL secara dinamis, sehingga dapat mengontrol risiko dan melindungi keuntungan dengan lebih baik. Namun, dalam penerapan praktis, tetap perlu memperhatikan faktor-faktor seperti pengaturan parameter, konfirmasi sinyal, pemilihan waktu perdagangan, dll., untuk lebih meningkatkan ketahanan dan profitabilitas strategi.

- 1