Rata-rata bergerak, rata-rata bergerak sederhana, kemiringan rata-rata bergerak, trailing stop, masuk kembali

Ikhtisar

Strategi ini membuat keputusan trading berdasarkan kemiringan moving average (MA) dan posisi relatif harga terhadap MA. Ketika kemiringan MA lebih besar dari ambang kemiringan minimum dan harga berada di atas MA, strategi melakukan pembelian. Pada saat yang sama, strategi menggunakan trailing stop loss untuk mengelola risiko, dan masuk kembali (re-entry) dalam kondisi tertentu. Strategi ini bertujuan untuk menangkap peluang dalam tren naik, sambil mengoptimalkan keuntungan dan risiko melalui stop loss dinamis dan mekanisme masuk kembali.

Prinsip Strategi

- Hitung simple moving average (SMA) periode tertentu sebagai indikator tren utama.

- Hitung kemiringan SMA dalam jendela periode tertentu untuk menilai kekuatan tren saat ini.

- Ketika kemiringan SMA lebih besar dari ambang kemiringan minimum dan harga berada di atas SMA, pasar dianggap berada dalam tren naik, dan strategi melakukan pembelian.

- Setelah masuk, strategi menggunakan mekanisme trailing stop loss untuk secara dinamis menyesuaikan level stop loss berdasarkan harga saat ini dan persentase yang ditentukan.

- Jika harga menyentuh level trailing stop loss, strategi menutup posisi dan menandai terjadinya stop loss.

- Setelah stop loss terjadi, jika harga mundur ke persentase tertentu di bawah SMA, strategi akan masuk kembali.

- Jika harga turun di bawah SMA, strategi langsung menutup posisi.

Analisis Keunggulan

- Pengikut Tren: Dengan menilai tren melalui kemiringan SMA dan posisi relatif harga terhadap SMA, strategi membantu meraih keuntungan dalam tren naik.

- Stop Loss Dinamis: Menggunakan mekanisme trailing stop loss yang menyesuaikan level stop loss secara dinamis berdasarkan perubahan harga, dapat melindungi laba dan membatasi kerugian dengan lebih baik.

- Masuk Kembali: Setelah stop loss terjadi, strategi akan masuk kembali ketika harga mundur ke persentase tertentu di bawah SMA, untuk menangkap potensi peluang pemulihan.

- Parameter Fleksibel: Strategi menyediakan beberapa parameter yang dapat disesuaikan, seperti periode SMA, ambang kemiringan minimum, persentase trailing stop loss, dll., yang dapat dioptimalkan sesuai dengan kondisi pasar yang berbeda.

Analisis Risiko

- Sensitivitas Parameter: Kinerja strategi mungkin cukup sensitif terhadap pengaturan parameter; pemilihan parameter yang tidak tepat dapat menyebabkan kinerja strategi yang buruk.

- Identifikasi Tren: Strategi terutama bergantung pada kemiringan SMA dan posisi relatif harga terhadap SMA untuk menilai tren, yang dapat menghasilkan sinyal yang salah dalam kondisi pasar tertentu.

- Frekuensi Stop Loss: Mekanisme trailing stop loss dapat menyebabkan stop loss yang sering, terutama dalam situasi volatilitas pasar yang tinggi, sehingga memengaruhi kinerja keseluruhan strategi.

- Risiko Masuk Kembali: Mekanisme masuk kembali dapat menyebabkan strategi masuk kembali lalu mengalami penurunan lebih lanjut dalam beberapa situasi, memperbesar kerugian.

Arah Optimasi

- Konfirmasi Tren: Saat menilai tren, dapat menggabungkan indikator teknis lain atau pola perilaku harga untuk meningkatkan akurasi identifikasi tren.

- Optimalisasi Stop Loss: Dapat mengeksplorasi metode stop loss lain, seperti stop loss berdasarkan volatilitas atau level support/resistance, untuk lebih beradaptasi dengan kondisi pasar yang berbeda.

- Kondisi Masuk Kembali: Dapat mengoptimalkan kondisi masuk kembali, misalnya dengan mempertimbangkan faktor seperti besarnya retracement harga, durasi waktu, dll., untuk menyaring sinyal masuk kembali yang merugikan.

- Manajemen Posisi: Memperkenalkan mekanisme manajemen posisi, menyesuaikan ukuran posisi setiap transaksi berdasarkan volatilitas pasar atau indikator risiko lainnya, untuk mengendalikan eksposur risiko keseluruhan.

Kesimpulan

Strategi ini menilai tren melalui kemiringan moving average dan posisi relatif harga terhadap moving average, dan menggunakan mekanisme trailing stop loss serta masuk kembali bersyarat untuk mengelola perdagangan. Keunggulan strategi terletak pada kemampuan mengikuti tren, perlindungan stop loss dinamis, dan penangkapan peluang masuk kembali. Namun, strategi juga memiliki potensi masalah seperti sensitivitas parameter, kesalahan identifikasi tren, frekuensi stop loss, dan risiko masuk kembali. Dapat diperbaiki dengan arah optimasi seperti mengoptimalkan identifikasi tren, metode stop loss, kondisi masuk kembali, dan manajemen posisi. Dalam penerapan praktis, harus dievaluasi dan disesuaikan dengan hati-hati sesuai dengan karakteristik pasar spesifik dan gaya trading.

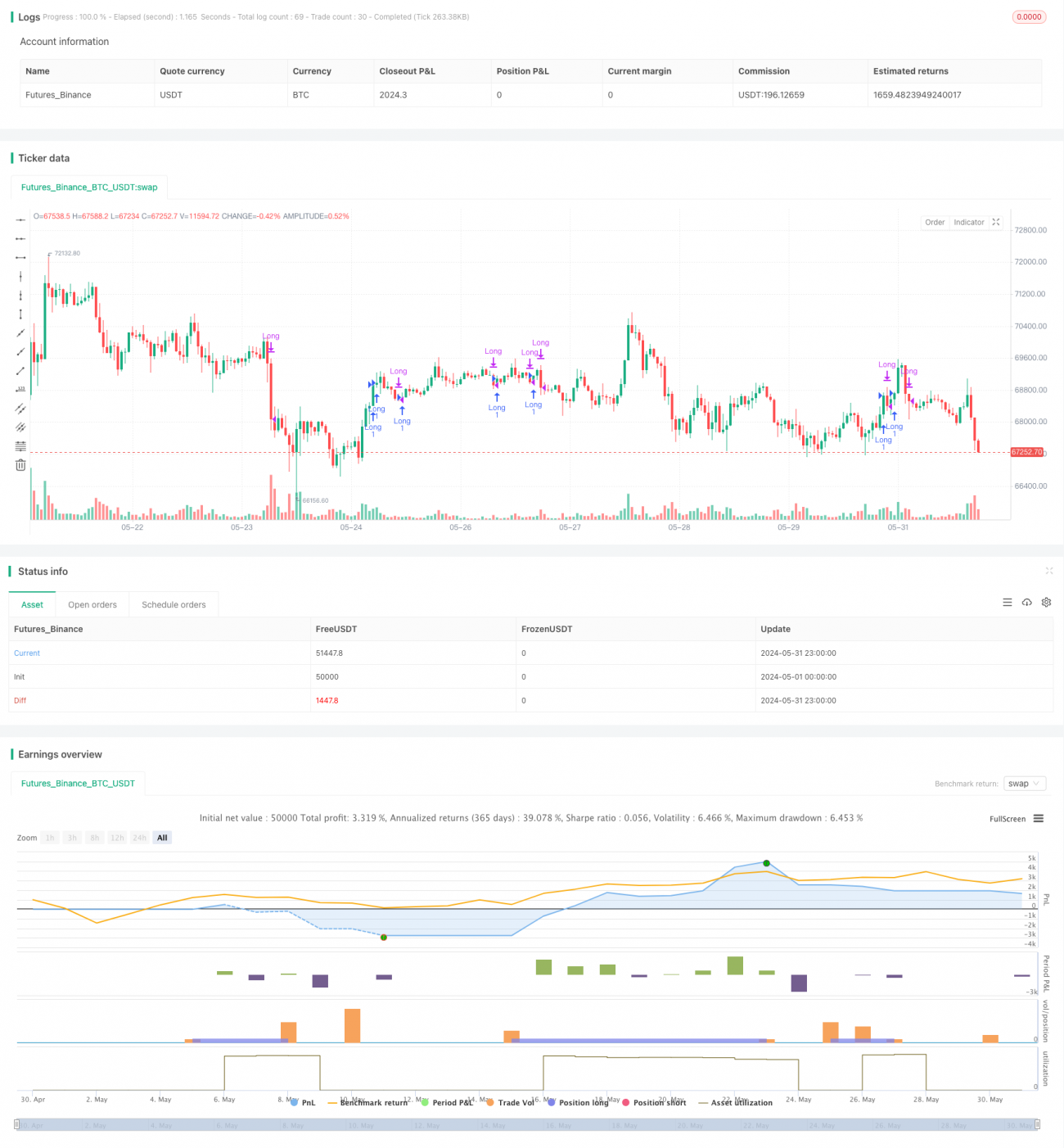

/*backtest

start: 2024-05-01 00:00:00

end: 2024-05-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("MA Incline Strategy with Trailing Stop-Loss and Conditional Re-Entry", overlay=true, calc_on_every_tick=true)

// Input parameters- 1