Strategi Volatilitas ATR Adaptif Dinamis Multi-Indikator untuk Penyesuaian Posisi

Ringkasan

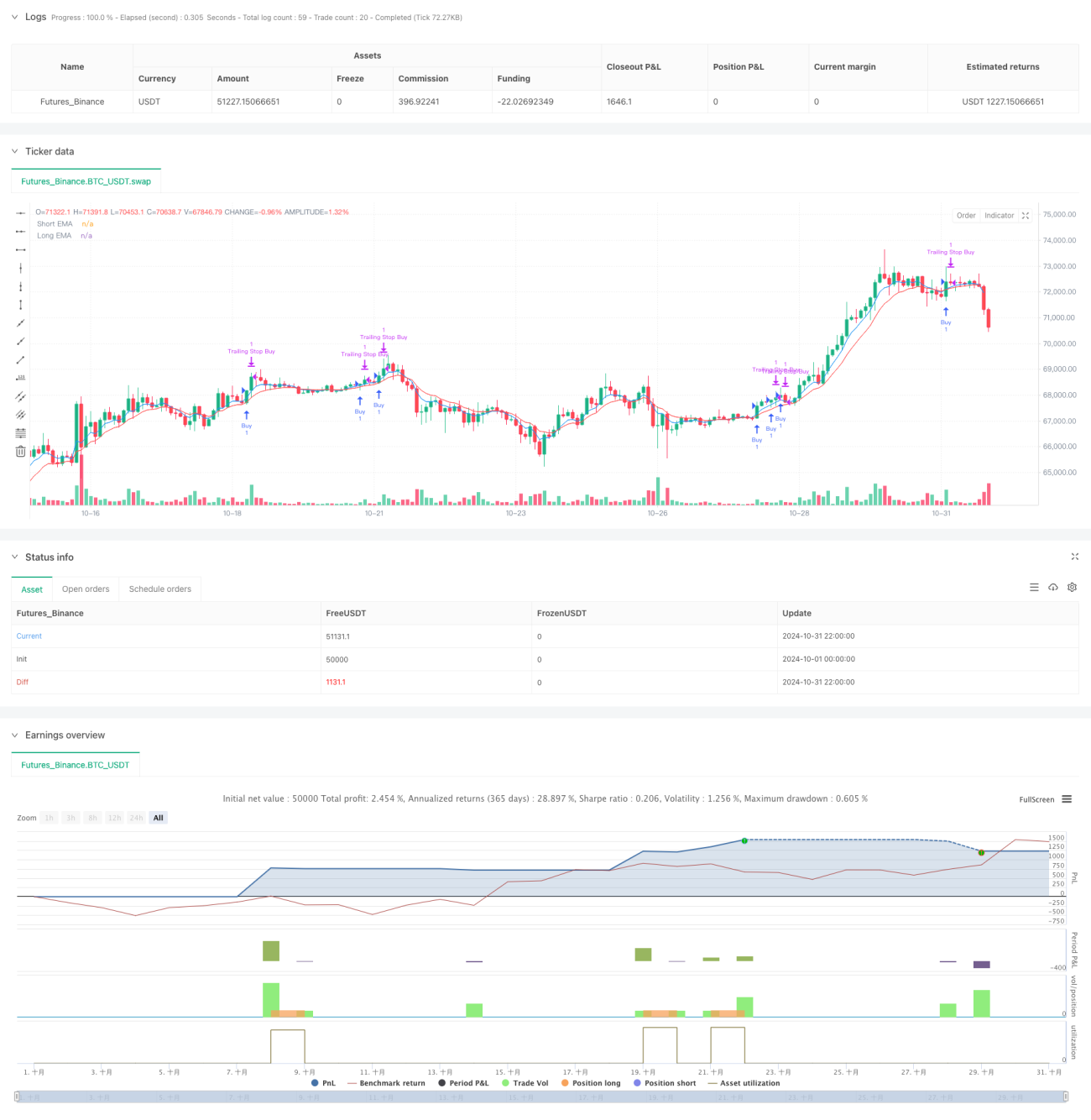

Strategi ini merupakan strategi perdagangan kuantitatif yang didasarkan pada berbagai indikator teknis dan manajemen risiko dinamis. Strategi ini menggabungkan beberapa dimensi seperti pelacakan tren EMA, volatilitas ATR, jenuh beli/jenuh jual RSI, serta pengenalan pola candlestick. Melalui penyesuaian posisi adaptif dan stop loss dinamis, strategi ini mencapai keseimbangan antara keuntungan dan risiko. Strategi ini menggunakan take profit bertahap dan stop loss trailing untuk melindungi laba.

Prinsip Strategi

Strategi ini terutama menjalankan perdagangan melalui aspek-aspek berikut:

- Menggunakan persilangan rata-rata bergerak EMA periode 5 dan 10 untuk menentukan arah tren.

- Melalui indikator RSI untuk mengidentifikasi area jenuh beli dan jenuh jual, menghindari membeli di puncak dan menjual di dasar.

- Menggunakan indikator ATR untuk menyesuaikan posisi stop loss dan ukuran posisi secara dinamis.

- Menggabungkan pola candlestick (engulfing, hammer, shooting star) sebagai sinyal masuk tambahan.

- Menerapkan mekanisme kompensasi slippage dinamis berbasis ATR.

- Menyaring sinyal palsu melalui konfirmasi volume perdagangan.

Keunggulan Strategi

- Verifikasi silang multi-sinyal untuk meningkatkan keandalan perdagangan.

- Manajemen risiko dinamis yang menyesuaikan secara adaptif dengan volatilitas pasar.

- Strategi take profit bertahap untuk mengunci sebagian laba secara wajar.

- Menggunakan stop loss trailing untuk melindungi laba yang sudah ada.

- Menetapkan batas stop loss harian untuk mengontrol eksposur risiko.

- Kompensasi slippage dinamis untuk meningkatkan tingkat eksekusi pesanan.

Risiko Strategi

- Banyaknya indikator dapat menyebabkan keterlambatan sinyal.

- Perdagangan yang sering dapat menimbulkan biaya yang lebih tinggi.

- Dalam pasar yang bergerak sideways, stop loss dapat sering terpicu.

- Pengenalan pola candlestick mengandung faktor subjektif.

- Optimasi parameter dapat menyebabkan overfitting.

Arah Optimasi Strategi

- Memperkenalkan penilaian siklus volatilitas pasar untuk menyesuaikan parameter secara dinamis.

- Menambahkan filter kekuatan tren untuk mengurangi sinyal palsu.

- Mengoptimalkan algoritma manajemen posisi untuk meningkatkan efisiensi penggunaan modal.

- Menambahkan lebih banyak indikator sentimen pasar.

- Mengembangkan sistem optimasi parameter adaptif.

Kesimpulan

Ini adalah sistem strategi yang matang dengan menggabungkan berbagai indikator teknis. Melalui manajemen risiko dinamis dan verifikasi sinyal ganda, strategi ini meningkatkan stabilitas perdagangan. Keunggulan inti strategi terletak pada sifat adaptifnya dan sistem pengendalian risiko yang komprehensif, namun masih perlu diuji secara menyeluruh dan dioptimalkan secara berkelanjutan dalam perdagangan riil.

- 1