Strategi Trading Dua Arah dengan Breakout Volatilitas Besar: Sistem Entry Long dan Short Berdasarkan Ambang Batas Level

Ringkasan

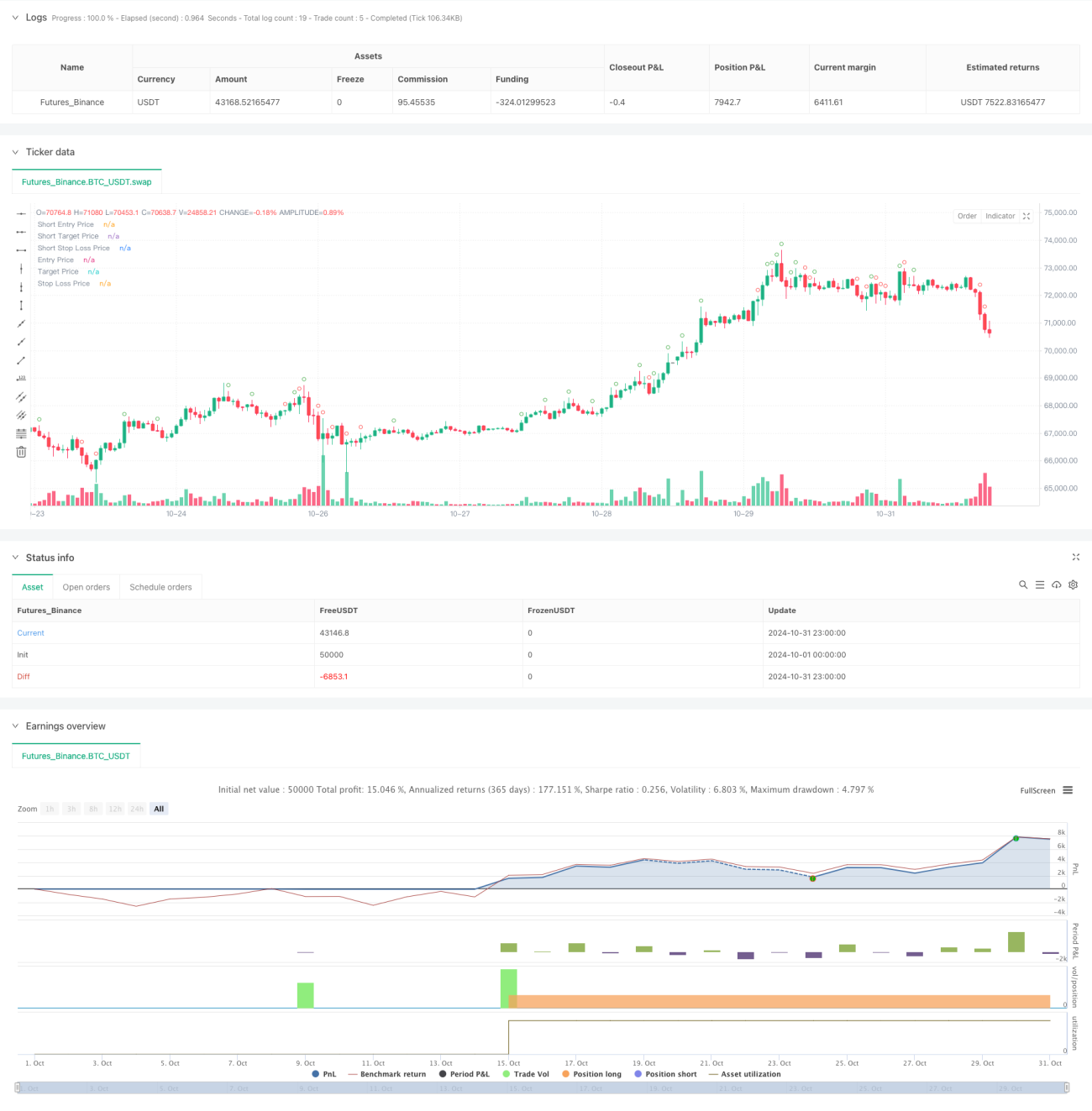

Strategi ini adalah sistem perdagangan dua arah berdasarkan grafik lilin 30 menit, yang mencari peluang perdagangan dengan memantau amplitudo pergerakan harga. Inti strategi adalah mengidentifikasi pergerakan besar dengan menetapkan ambang batas poin, dan melakukan perdagangan ke arah yang sesuai setelah konfirmasi breakout. Strategi ini mencakup manajemen waktu yang ketat, stop loss dan take profit, serta mekanisme manajemen perdagangan untuk mencapai perdagangan otomatis dengan risiko yang terkendali.

Prinsip Strategi

Strategi menggunakan beberapa mekanisme penyaringan untuk mengidentifikasi sinyal perdagangan yang valid. Pertama, strategi menghitung rentang pergerakan tubuh lilin pada setiap penutupan grafik lilin 30 menit. Ketika amplitudo pergerakan melebihi ambang batas yang telah ditentukan, itu akan ditandai sebagai peluang perdagangan potensial. Untuk memastikan efektivitas perdagangan, strategi menetapkan poin buffer tambahan, dan sinyal perdagangan aktual hanya akan dipicu ketika harga menembus zona buffer ini. Strategi ini juga menerapkan perdagangan dua arah (long dan short), yaitu membeli saat breakout naik dan menjual saat breakout turun, serta menetapkan stop loss dan take profit yang sesuai untuk setiap perdagangan.

Keunggulan Strategi

- Manajemen waktu yang baik: Membatasi jendela waktu perdagangan untuk menghindari sinyal palsu selama periode tidak aktif.

- Mekanisme perdagangan dua arah: Dapat menangkap peluang di kedua arah pasar, meningkatkan efisiensi penggunaan modal.

- Pengendalian risiko yang lengkap: Menggunakan stop loss dan take profit pada level tetap untuk memudahkan penilaian dan manajemen risiko.

- Tingkat otomatisasi tinggi: Mulai dari identifikasi sinyal hingga eksekusi perdagangan sepenuhnya otomatis, mengurangi intervensi manusia.

- Pengaturan parameter yang fleksibel: Parameter kunci dapat disesuaikan untuk beradaptasi dengan berbagai kondisi pasar.

Risiko Strategi

- Risiko breakout palsu: Pergerakan besar dapat diikuti oleh breakout palsu, menyebabkan stop loss tersentuh.

- Sensitivitas parameter: Pengaturan ambang batas yang tidak tepat dapat menyebabkan peluang terlewatkan atau perdagangan berlebihan.

- Ketergantungan pada kondisi pasar: Dalam pasar yang bergerak sideways (kisaran), stop loss mungkin sering tersentuh.

- Pengaruh slippage: Selama periode volatilitas tinggi, harga eksekusi aktual dapat menyimpang secara signifikan dari harga sinyal.

- Risiko manajemen modal: Tidak adanya mekanisme manajemen posisi dapat menyebabkan eksposur risiko yang terlalu besar.

Arah Optimasi Strategi

- Menambahkan filter tren: Menggabungkan indikator tren jangka panjang untuk meningkatkan kualitas sinyal.

- Optimasi parameter dinamis: Secara otomatis menyesuaikan ambang batas dan parameter stop loss berdasarkan volatilitas pasar.

- Memperkenalkan konfirmasi volume: Menambahkan filter volume untuk meningkatkan keandalan breakout.

- Mengoptimalkan take profit dan stop loss: Menerapkan stop loss dan take profit dinamis untuk beradaptasi dengan berbagai kondisi pasar.

- Menambahkan manajemen posisi: Menyesuaikan posisi secara dinamis berdasarkan kekuatan sinyal dan volatilitas pasar.

Kesimpulan

Ini adalah strategi perdagangan otomatis yang dirancang secara lengkap dan logis. Dengan penyaringan kondisi yang ketat dan pengendalian risiko, strategi ini memiliki kepraktisan yang baik. Namun, masih perlu diuji dan dioptimalkan secara menyeluruh dalam perdagangan langsung (live trading), terutama dalam hal pengaturan parameter dan pengendalian risiko yang perlu disesuaikan dengan kondisi pasar aktual. Keberhasilan strategi memerlukan lingkungan pasar yang stabil dan konfigurasi parameter yang tepat. Disarankan untuk melakukan backtesting yang memadai sebelum digunakan dalam perdagangan langsung.

- 1