Ikhtisar

Strategi ini adalah sistem trading kuantitatif yang menggabungkan Bollinger Bands, Relative Strength Index (RSI), dan Dollar Cost Averaging (DCA). Dengan menetapkan aturan manajemen modal, strategi ini secara otomatis melakukan pembukaan posisi secara bertahap di tengah volatilitas pasar, sekaligus menggunakan indikator teknis untuk menentukan sinyal beli dan jual, sehingga menghasilkan eksekusi trading dengan risiko yang terkendali. Sistem ini juga mencakup logika take profit dan fitur pelacakan akumulasi laba, yang memungkinkan pemantauan dan pengelolaan kinerja trading secara efektif.

Prinsip Strategi

Strategi ini beroperasi terutama berdasarkan komponen inti berikut:

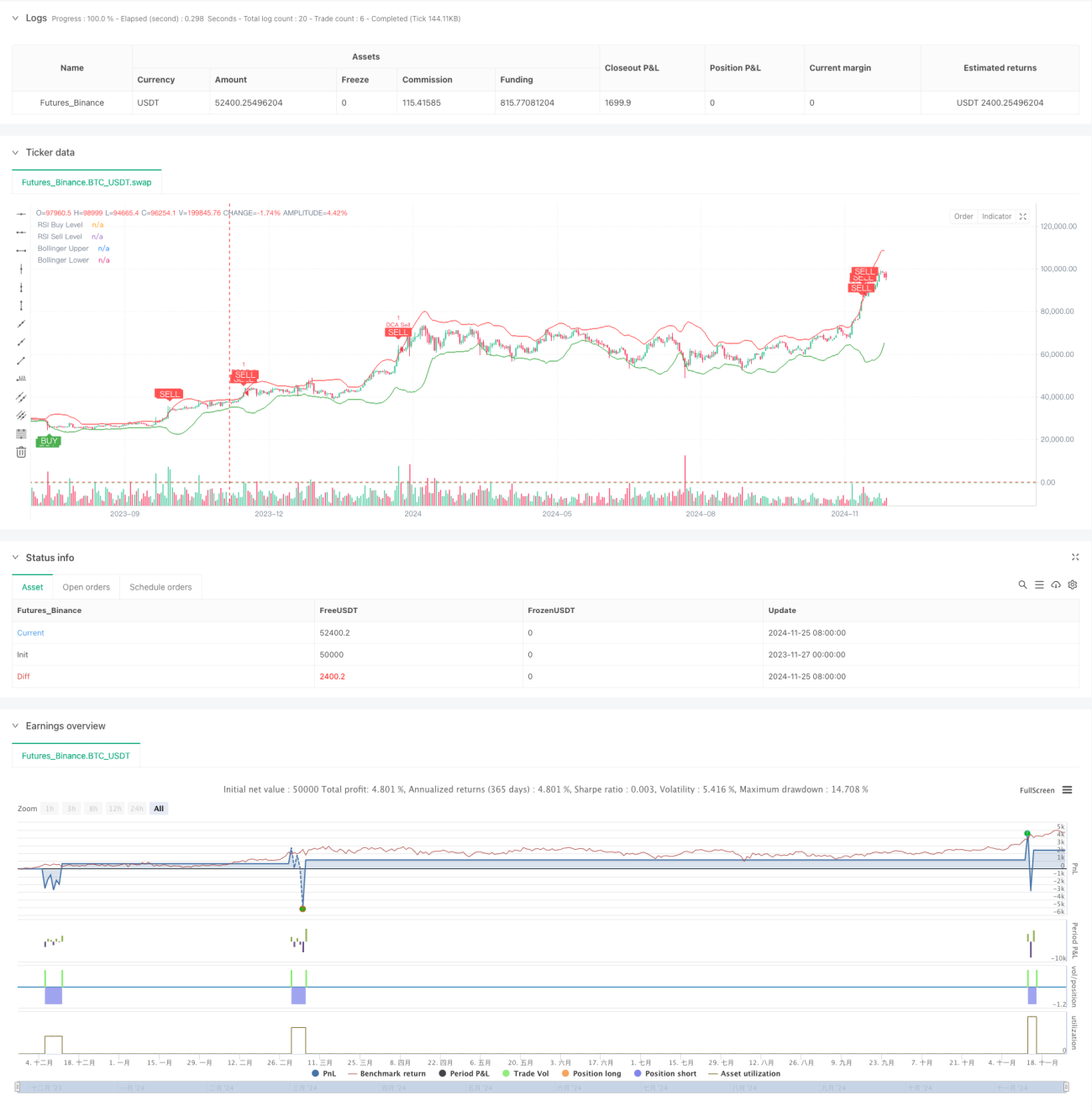

- Indikator Bollinger Bands digunakan untuk menentukan rentang fluktuasi harga; ketika harga menyentuh pita bawah, pertimbangkan untuk membeli; ketika menyentuh pita atas, pertimbangkan untuk menjual.

- Indikator RSI digunakan untuk mengonfirmasi kondisi overbought atau oversold pasar; RSI di bawah 25 mengonfirmasi oversold, di atas 75 mengonfirmasi overbought.

- Modul DCA secara dinamis menghitung jumlah dana untuk setiap pembukaan posisi berdasarkan ekuitas akun, sehingga mewujudkan manajemen modal yang adaptif.

- Modul take profit menetapkan target keuntungan 5%; ketika target tercapai, posisi otomatis ditutup untuk melindungi laba.

- Modul pemantauan kondisi pasar menghitung besarnya perubahan pasar selama 90 hari, membantu dalam menilai tren secara keseluruhan.

- Modul pelacakan akumulasi laba mencatat untung/rugi setiap transaksi, memudahkan evaluasi kinerja strategi.

Keunggulan Strategi

- Menggabungkan validasi silang dari berbagai indikator teknis, meningkatkan keandalan sinyal.

- Menggunakan manajemen posisi dinamis, menghindari risiko yang ditimbulkan oleh posisi tetap.

- Menetapkan kondisi take profit yang wajar, mengunci laba tepat waktu.

- Dilengkapi fungsi pemantauan tren pasar, memudahkan pemahaman situasi secara makro.

- Sistem pelacakan laba yang lengkap, memudahkan analisis kinerja strategi.

- Konfigurasi fitur peringatan yang baik, dapat mengingatkan peluang trading secara real-time.

Risiko Strategi

- Pasar yang bergejolak (sideways) dapat memicu sinyal secara sering sehingga meningkatkan biaya transaksi.

- Indikator RSI dapat menghasilkan keterlambatan di pasar yang sedang tren.

- Take profit dengan persentase tetap dapat menyebabkan keluar terlalu awal di pasar tren kuat.

- Strategi DCA dapat menyebabkan drawdown yang signifikan di pasar yang sedang menurun secara sepihak.

Disarankan untuk mengambil langkah-langkah berikut dalam mengelola risiko:

- Menetapkan batas maksimum kepemilikan posisi.

- Menyesuaikan parameter secara dinamis berdasarkan volatilitas pasar.

- Menambahkan filter tren.

- Menerapkan strategi take profit bertahap.

Arah Optimasi Strategi

- Optimasi parameter dinamis:

- Parameter Bollinger Bands dapat disesuaikan secara adaptif berdasarkan volatilitas.

- Ambang batas RSI dapat berubah sesuai siklus pasar.

- Proporsi dana DCA dapat disesuaikan mengikuti skala akun.

- Penguatan sistem sinyal:

- Menambahkan konfirmasi volume transaksi.

- Menambahkan analisis garis tren.

- Menggabungkan lebih banyak indikator teknis untuk validasi silang.

- Penyempurnaan kontrol risiko:

- Menerapkan stop loss dinamis.

- Menambahkan kontrol drawdown maksimum.

- Menetapkan batas kerugian harian.

Kesimpulan

Strategi ini membangun sistem trading yang cukup lengkap dengan mengintegrasikan analisis teknikal dan metode manajemen modal. Keunggulan strategi terletak pada konfirmasi sinyal ganda dan manajemen risiko yang matang, namun tetap perlu diuji dan dioptimalkan secara menyeluruh dalam perdagangan riil. Dengan terus menyempurnakan pengaturan parameter dan menambahkan indikator pendukung, strategi ini diharapkan dapat mencapai kinerja yang stabil dalam perdagangan aktual.

/*backtest

start: 2023-11-27 00:00:00

end: 2024-11-26 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Combined BB RSI with Cumulative Profit, Market Change, and Futures Strategy (DCA)", shorttitle="BB RSI Combined DCA Strategy", overlay=true)

// Input Parameters- 1