Strategi Deteksi Celah Nilai Wajar Tingkat Lanjut Berdasarkan Manajemen Risiko Dinamis dan Keuntungan Tetap

Ikhtisar

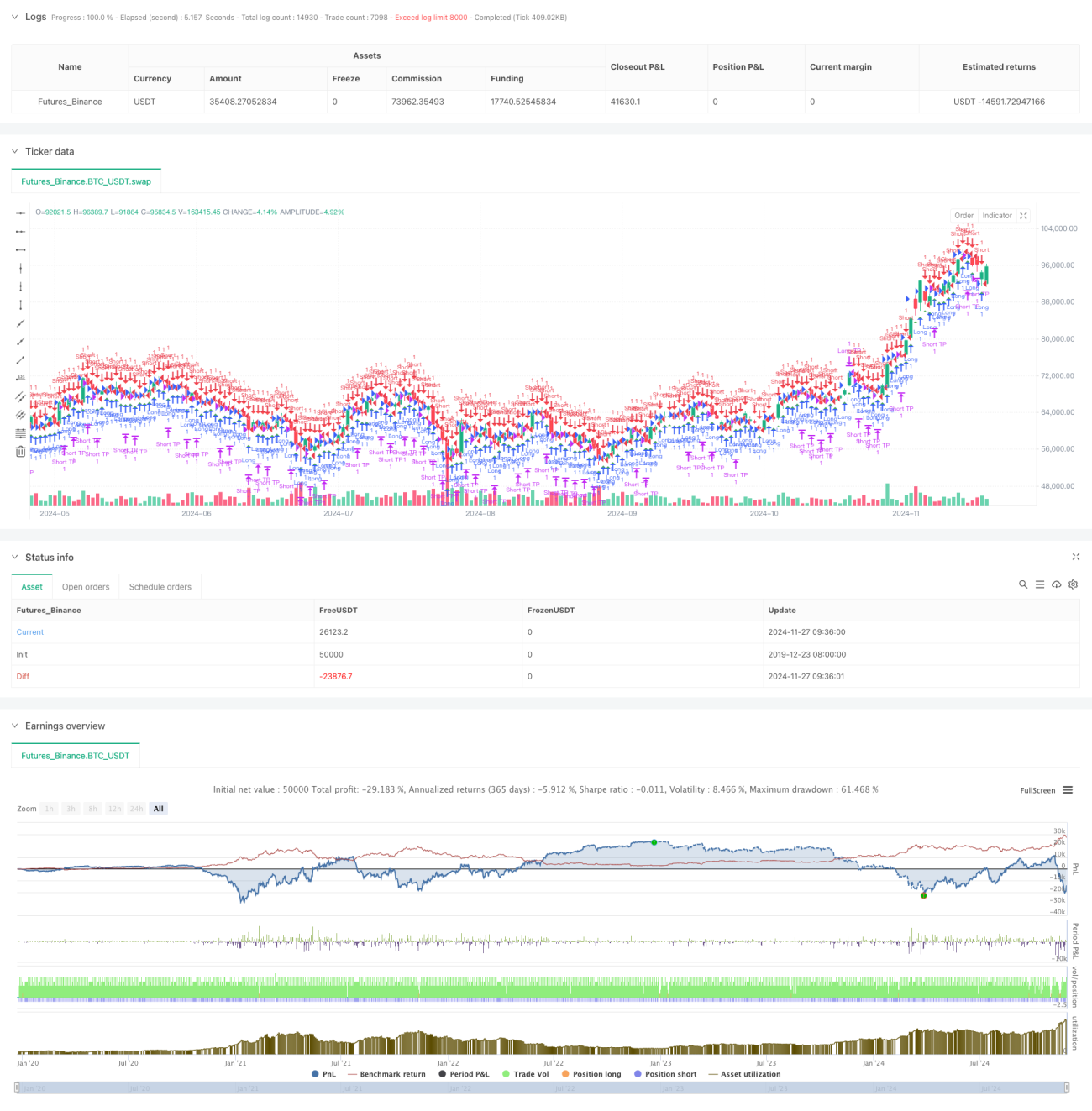

Strategi ini didasarkan pada konsep Kesenjangan Nilai Wajar (FVG) yang dikombinasikan dengan manajemen risiko dinamis dan target keuntungan tetap. Strategi berjalan pada timeframe 15 menit, mengidentifikasi celah harga di pasar untuk menangkap peluang trading potensial. Berdasarkan data backtest, dari November 2023 hingga Agustus 2024, strategi ini mencapai laba bersih sebesar 284,40% dengan total 153 transaksi, tingkat kemenangan 71,24%, dan faktor keuntungan 2,422.

Prinsip Strategi

Inti strategi adalah mengidentifikasi Fair Value Gap dengan memantau hubungan harga antara tiga candle berturut-turut. Secara spesifik:

- Kondisi pembentukan FVG bullish: ketika harga tertinggi candle sebelumnya lebih rendah dari harga terendah dua candle sebelumnya.

- Kondisi pembentukan FVG bearish: ketika harga terendah candle sebelumnya lebih tinggi dari harga tertinggi dua candle sebelumnya.

- Sinyal masuk dipicu oleh parameter ambang batas FVG, hanya aktif ketika ukuran celah melebihi persentase harga tertentu.

- Pengendalian risiko menggunakan persentase tetap (1%) dari ekuitas akun sebagai standar stop loss.

- Target keuntungan ditetapkan dengan jumlah poin tetap (50 poin).

Keunggulan Strategi

- Manajemen risiko ilmiah dan masuk akal: Menggunakan stop loss berdasarkan persentase ekuitas akun untuk kontrol risiko dinamis.

- Aturan trading jelas: Menggunakan target keuntungan tetap, menghindari penilaian subjektif.

- Kinerja unggul: Tingkat kemenangan dan faktor keuntungan yang tinggi menunjukkan stabilitas strategi yang baik.

- Implementasi sederhana: Logika kode jelas, mudah dipahami dan dipelihara.

- Adaptabilitas tinggi: Dapat disesuaikan dengan parameter untuk beradaptasi dengan kondisi pasar yang berbeda.

Risiko Strategi

- Risiko volatilitas pasar: Target keuntungan titik tetap mungkin kurang fleksibel di pasar dengan volatilitas tinggi.

- Risiko slippage: Frekuensi trading tinggi dapat menyebabkan biaya slippage yang tinggi.

- Ketergantungan parameter: Kinerja strategi sangat bergantung pada pengaturan ambang batas FVG.

- Risiko false breakout: Beberapa sinyal FVG mungkin merupakan false breakout, memerlukan indikator konfirmasi tambahan.

- Risiko manajemen modal: Stop loss proporsi tetap dapat menyebabkan penurunan modal cepat saat mengalami kerugian beruntun.

Arah Optimasi Strategi

- Memperkenalkan indikator volatilitas pasar untuk menyesuaikan target keuntungan secara dinamis.

- Menambahkan filter tren untuk menghindari trading di pasar sideways.

- Mengembangkan mekanisme konfirmasi multi-timeframe.

- Mengoptimalkan algoritma manajemen posisi, memperkenalkan sistem posisi variabel.

- Menambahkan filter waktu trading untuk menghindari periode volatilitas tinggi.

- Mengembangkan sistem penilaian kekuatan sinyal untuk menyaring peluang trading berkualitas tinggi.

Kesimpulan

Strategi ini menunjukkan hasil trading yang baik dengan menggabungkan teori Fair Value Gap dan metode manajemen risiko yang ilmiah. Tingkat kemenangan yang tinggi dan faktor keuntungan yang stabil menunjukkan nilai praktisnya. Melalui arah optimasi yang disarankan, strategi ini masih memiliki potensi peningkatan lebih lanjut. Disarankan agar trader melakukan optimasi parameter dan validasi backtest yang memadai sebelum menggunakan secara langsung di akun riil.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-28 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Fair Value Gap Strategy with % SL and Fixed TP", overlay=true, initial_capital=500, default_qty_type=strategy.fixed, default_qty_value=1)

// Parameters- 1