Strategi Adaptif Campuran Rata-rata Bergerak Ganda dan Relatif Kekuatan

Ikhtisar

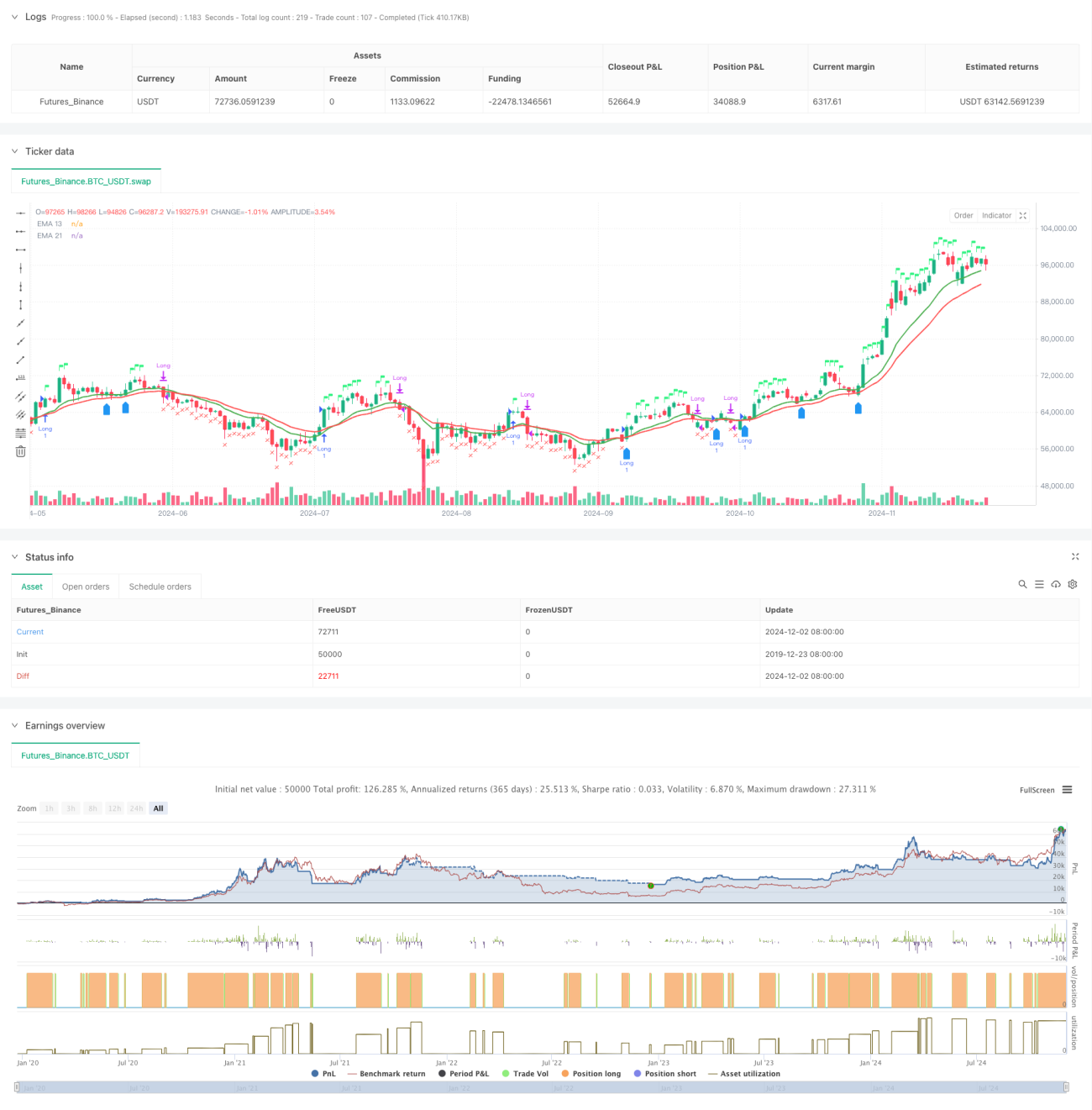

Strategi ini merupakan sistem perdagangan komprehensif yang menggabungkan sistem rata-rata bergerak ganda, Relative Strength Index (RSI), dan analisis Relative Strength (RS). Strategi mengonfirmasi tren melalui persilangan Exponential Moving Average (EMA) 13 hari dan 21 hari, sekaligus menggabungkan RSI dan nilai RS relatif terhadap indeks acuan untuk konfirmasi sinyal perdagangan, sehingga menciptakan mekanisme pengambilan keputusan multi-dimensi. Strategi ini juga mencakup mekanisme pengendalian risiko berdasarkan titik tertinggi 52 minggu dan penilaian kondisi masuk kembali.

Prinsip Strategi

Strategi menggunakan mekanisme konfirmasi sinyal ganda:

- Sinyal masuk harus memenuhi semua kondisi berikut:

- EMA13 melintasi di atas EMA21 atau harga berada di atas EMA13

- RSI lebih besar dari 60

- Relative Strength (RS) bernilai positif

- Kondisi keluar meliputi:

- Harga turun di bawah EMA21

- RSI di bawah 50

- RS berubah menjadi negatif

- Kondisi masuk kembali:

- Harga melintasi di atas EMA13 dan EMA13 lebih besar dari EMA21

- RS tetap positif

- Atau harga menembus titik tertinggi minggu lalu

Keunggulan Strategi

- Mekanisme konfirmasi sinyal ganda mengurangi risiko false breakout

- Menggabungkan analisis Relative Strength untuk menyaring instrumen yang kuat secara efektif

- Menggunakan mekanisme penyesuaian periode waktu adaptif

- Memiliki sistem pengendalian risiko yang lengkap

- Mencakup mekanisme masuk kembali yang cerdas

- Menyediakan visualisasi status perdagangan secara real-time

Risiko Strategi

- Pasar yang berfluktuasi dapat menghasilkan perdagangan yang sering

- Ketergantungan pada beberapa indikator dapat menyebabkan keterlambatan sinyal

- Ambang batas RSI yang tetap mungkin tidak cocok untuk semua kondisi pasar

- Perhitungan Relative Strength bergantung pada akurasi indeks acuan

- Level stop loss pada titik tertinggi 52 minggu mungkin terlalu longgar

Arah Optimasi Strategi

- Memperkenalkan ambang batas RSI adaptif

- Mengoptimalkan logika penilaian kondisi masuk kembali

- Menambahkan dimensi analisis volume perdagangan

- Menyempurnakan mekanisme take profit dan stop loss

- Menambahkan filter volatilitas

- Mengoptimalkan periode perhitungan Relative Strength

Kesimpulan

Strategi ini membangun sistem perdagangan yang komprehensif dengan menggabungkan analisis teknis dan analisis Relative Strength. Mekanisme konfirmasi sinyal ganda dan sistem pengendalian risikonya membuatnya sangat praktis. Melalui arah optimasi yang disarankan, strategi masih memiliki ruang untuk peningkatan lebih lanjut. Keberhasilan implementasi strategi membutuhkan pemahaman mendalam tentang pasar dari para pedagang, serta penyesuaian parameter yang tepat sesuai dengan karakteristik instrumen perdagangan spesifik.

- 1